EM LATAM SOV: Market Wrap

* A stronger than expected monthly U.S. labor report triggered a Treasury bear market curve flatte...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

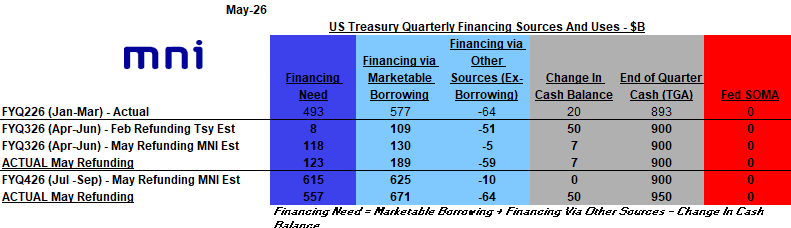

US TSYS/SUPPLY: 2nd Straight Rise In TGA Cash Target (3/3)

Monday's financing requirements probably contained the most surprises of the refunding round, and even here they were relatively modest.

- The April-June quarter's estimated financing needs were in line with MNI's expectation at $123B, though were well up from the $8B expected as of the February refunding. However the marketable borrowing requirement of $189B was higher than we had anticipated with the "other sources" financing remaining elevated at $-59B vs our (and consensus) expectation that it would be reduced. Per Treasury, the revision to the borrowing estimate was "primarily due to lower projected net cash flows, partially offset by the higher-than-assumed beginning-of-quarter cash balance".

- That was a theme: for the Jul-Sep quarter, financing via "other sources" was larger than most had penciled in (several analysts saw this column being a zero), at $-64B. The actual financing need ($557B) was a little smaller than we'd expected, though this was largely the result of the TGA cash balance change of $50B to $950B, which had been a risk but somewhat of a surprise (without this $50B, the financing need would have been $607B). Financing via marketable borrowing was higher at $671B (we'd penciled in $625B).

- That marks the 2nd consecutive quarter with a $50B increase in the TGA target.

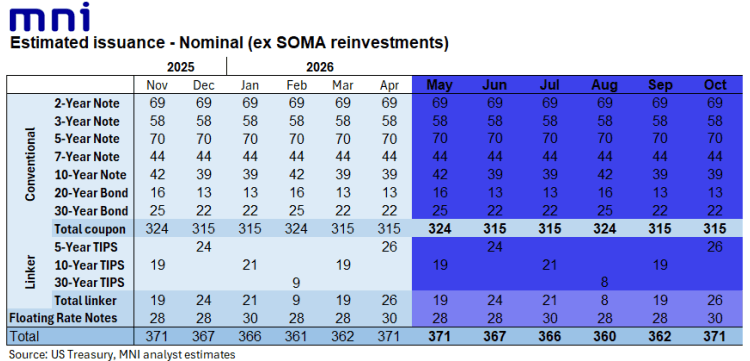

US TSYS/SUPPLY: Auction Announcements Bring No Drama, 20Y Settles Tweaked (2/3)

The actual coupon size announcements for the May refunding auctions and estimates for the quarter brought no drama: next week brings sales of 3Y note for $58B, 10Y Note for $42B, and 30Y Bond for $25B.

- TIPS auction sizes were kept unchanged again with May 10Y reopen at $19B, June 5Y reopen at $24B, and July new 10Y at $21B.

- One tweak is that the timing of 20Y Bond settlements will change. Starting in June, reopenings will now settle on the Friday of the auction week; new issues will continue to settle at month-end. As Treasury explains, "Shortening the when-issued period is expected to mitigate repo specialness that often occurs surrounding reopening auctions. This change is consistent with feedback provided by a variety of market participants, including the primary dealers." This change had been flagged in advance and is not a major surprise.

- See image below for expected auction sizes (unrevised from MNI's pre-refunding estimates).

- Meanwhile the path of bill issuance was largely as expected, given the usual tax/seasonal flows, with Treasury announcing its intention to increase the size of "shorter-dated benchmark bills over the coming weeks and, in late-May, anticipates issuing a short-dated CMB to meet the peak liquidity needs at the end of May due to maturing coupon securities". After this, Treasury will reduce sizes in June before "incrementally" increasing sizes "across the curve".

- The Buyback program schedule is here. Again, it contained few surprises: Treasury will buy a max $38B in liquidity support operations and up to $25B in short-term securities for cash management purchases (June 4 and June 11, in the run-up to the mid-June tax date).

US TSYS/SUPPLY: May Refunding: No Guidance Change, Later Coupon Upsizing (1/3)

The lack of revision to Treasury's guidance on future nominal coupon size increases ("Based on current projected borrowing needs, Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters") is likely to further push back expectations for the timing of the next size increase to well into 2027 if not beyond.

- This was probably the most closely-eyed portion of the refunding announcement, with some expectations that it would be revised to indicate a nearer-term upping of auction sizes, perhaps by removing the words "at least". Coming into the week, most analysts saw February 2027 as the base case for the next coupon upsizing with some having pushed back their expectations from November 2026 in recent months; with some seeing bigger coupon sizes as soon as November 2026 (Danske) with others only seeing changes much further out (Mizuho: FY 2029).

- The TBAC minutes for May's refunding also noted "Dealers generally anticipate that nominal coupon auction sizes might next increase in early CY2027, and expect Treasury to modify its forward guidance several quarters ahead of such a change".

- A revision in the guidance at this meeting is probably inconsistent with an upsizing in early 2027 (ie February), which is only 3 quarters away, so the base case probably shifts to May 2027.

- Since the announcement and its unchanged guidance, we've seen one analyst push back expectations (TD Securities now sees May 2027 having previously expected February 2027).

- MNI's central expectation had been either February or May 2027 and the latter is obviously looking more likely, particularly since we had (in a close call) expected a softening of guidance at this refunding.