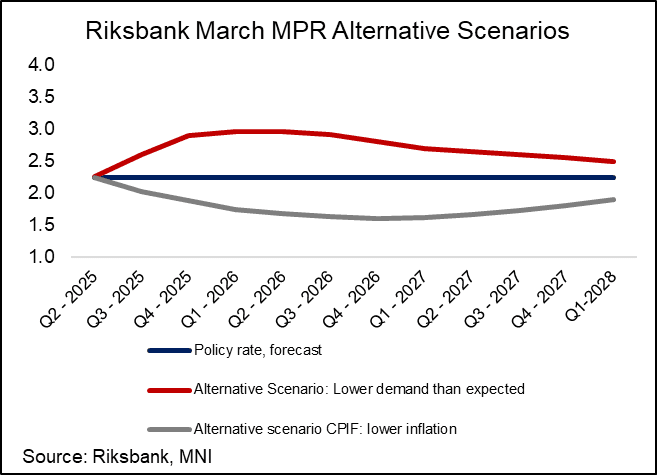

RIKSBANK: March MPR Alternative Scenarios Highlight Two-way Tariff Risks

The March MPR alternative scenarios highlight the two-way risks for the policy rate in response to increased (US) trade frictions. Developments in this complex, particularly in April when the "reciprocal tariff" regime is expected to start, will be key to the Riksbank's rate outlook. One scenario presented looks at the case where “new trade barriers lead to lower productivity and higher inflation”, while the other analysts a case where “uncertainty about international economic developments lead to weak demand and a lower policy rate”.

- In the first scenario, “It is assumed in the scenario with new trade barriers that during the spring the United States raises its import tariffs against the EU substantially, and that the EU responds with similar retaliatory measures”.

- With inflationary pressures clearly rising, the Riksbank raises the policy rate by 25bps in June to 2.50%. Afterwards, “inflation and the inflation outlook continue to deteriorate over the summer and the Riksbank therefore continues to raise the policy rate during the second half of the year”

- In the second scenario, “rising uncertainty will gradually lead to increasingly large falls in confidence among households and companies, both in Sweden and abroad”…. “After the summer, the Riksbank begins a new cycle of interest rate cuts”

- However, “it is assumed in this scenario that the economic policy uncertainty persists for a long period of time and thus the risk of new inflationary impulses from abroad remains”. Thus, “as inflation is somewhat higher than the target of 2 per cent to start, monetary policy cannot entirely disregard these risks. In this scenario, the Riksbank therefore chooses a strategy of gradual interest rate cuts and it is not until sometime into 2026 that resource utilisation begins to rise clearly again”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Gilts Underperform Bunds As Markets Assess Mixed Labour Market Data

Gilt futures underperform Bunds, as markets weigh stronger-than-expected signals from the quantity side of the labour market against broadly in line pay growth.

- Gilt futures are -36 ticks at 92.61. The Feb 12 low at 92.31 remains intact, with futures troughing at 92.43 at the open. Initial resistance is the Feb 10 high at 93.71.

- The curve has lightly bear steepened, with yields 2-3bps higher.

- The 10-year Gilt/Bund spread is 2bps wider at 205.5bps, unwinding a good deal of yesterday’s tightening. 10-year yields are 3bps higher today at 4.557%, just short of the Feb 12 high at 4.579%.

- BOE Governor Bailey speaks in a Fireside Chat on “Preserving and enhancing open financial markets” at 0930GMT, so is unlikely to focus on monetary policy topics.

GLOBAL POLITICAL RISK: US-Russia Talks Underway As UK PM Proposes US 'Backstop'

Talks are underway in the Saudi capital Riyadh between delegations from the US and Russia in what could prove the first step towards peace talks to end the war in Ukraine. The US has painted the discussions as preliminary talks to infer whether Russia is serious about holding eventual ceasefire negotiations. Russia, on the other hand, has said the talks will cover "the entire complex of Russian-American relations”, preparations for peace talks, and planning for a meeting between Presidents Putin and Trump.

- Much of the meeting set to be behind closed doors, so headlines could come out sporadically or may be restricted to official pressers or readouts.

- No Ukrainian delegation is taking part in these discussions, with the US claiming that as they are not peace negotiations Ukrainian representation is not needed at this stage. Speaking in the UAE on 17 Feb, Ukrainian President Volodymyr Zelenskyy said "We cannot recognise [peace] agreements...without us,".

- Some of Ukraine's European allies met in Paris on 17 Feb. UK PM Sir Keir Starmer's proposals for UK and US troops to serve in Ukraine as peacekeepers have exposed cracks within the alliance. Politico: "German Chancellor Olaf Scholz seemed quietly furious when he told reporters he was a “little irritated” by the talk, which he called “completely premature” and “highly inappropriate.” Polish PM Donald Tusk made clear he doesn’t want his army to contribute, while the FT reported that Italian leader and Trump pal Giorgia Meloni [...] told leaders that sending troops was “the most complex [option] and least likely to be effective."

STIR: Euribor Futures Inching Away From Session Lows; MNI ECB Event Today

Euribor futures are inching away from session lows alongside Schatz and Bunds, after STIRs followed core FI lower overnight amid cautious Fedspeak, prospects of increased European defence spending and weak JGB price action.

- Futures are flat to -2.5 ticks through the blues at typing.

- There are 56bps of easing priced through the June gathering (i.e. just over 2x25bp rate cuts).

- French January final HICP confirmed flash estimates, though Y/Y CPI saw a 3 tenth upward revision. The ZEW survey is expected to be strong (expectations component seen at 20.0 vs 10.3 prior), owing to the continued rally in European equities.

- Yesterday evening, ECB’s Holzmann provided characteristically hawkish comments in an interview. In particular, he argued that an inflation rate of below 2% was “a reason to cut less, because if you automatically cut further when you see such a trend, then the expectation of lower inflation might become self-fulfilling”. Holzmann speaks again at 0900GMT this morning.

- ECB Executive Board Member Cipollone speaks on the ECB’s balance sheet at an MNI Event at 1400GMT/1500CET (sign up here).

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Mar-25 | 2.424 | -24.1 |

| Apr-25 | 2.275 | -39.0 |

| Jun-25 | 2.105 | -56.1 |

| Jul-25 | 2.043 | -62.3 |

| Sep-25 | 1.965 | -70.0 |

| Oct-25 | 1.942 | -72.3 |

| Dec-25 | 1.907 | -75.8 |

| Feb-26 | 1.905 | -76.0 |

| Source: MNI/Bloomberg. | ||