EU CREDIT SUPPLY: Mapfre (MAPSM) :IPT

Market Sources Mapfre EUR 500mn (WNG) 11NC10 Tier 2 - IPTs MS+175/180bps area ------------------...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Bear Cycle Extension

- RES 4: 1.4015 High Dec 2 ‘25

- RES 3: 1.3985 76.4% retracement of the Nov 5 ‘25 - Jan 30 bear leg

- RES 2: 1.3878/3967 High Apr 13 / High Mar 31 and the bull trigger

- RES 1: 1.3733 50-day EMA

- PRICE: 1.3577 @ 16:57 BST May 1

- SUP 1: 1.3555 Low Mar 11

- SUP 2: 1.3525 1.0% 10-dma envelope

- SUP 3: 1.3482 Low Jan 30 and key support

- SUP 4: 1.3420 Low Sep 25

The short-term bear cycle in USDCAD remains in play and Thursday’s sell-off reinforces current bearish conditions. The move down signals scope for an extension towards 1.3526 next, the Mar 9 low and the next key support. Clearance of this level would open 1.3482, the Jan 30 low. Initial resistance is seen at 1.3739, the 50-day EMA. A clear break of this average is required to signal a possible short-term reversal.

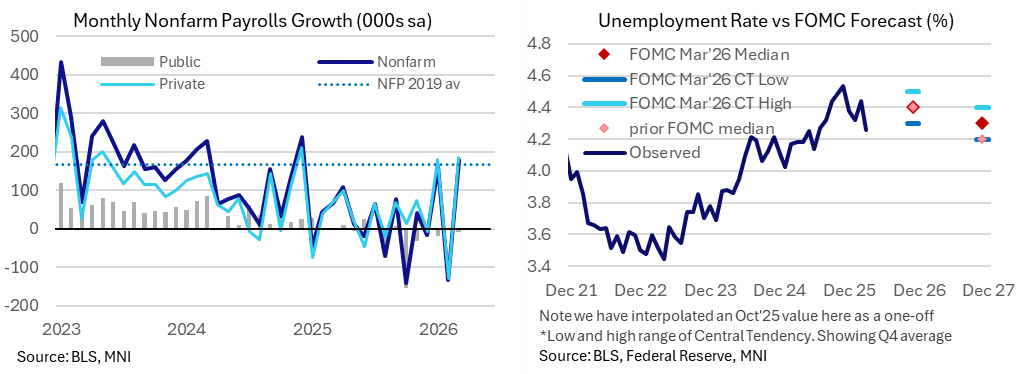

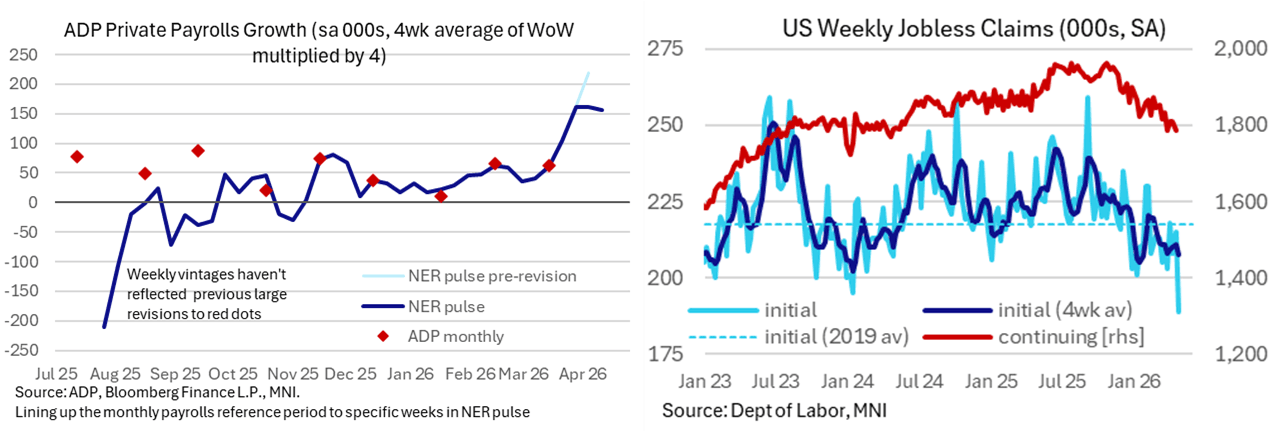

LOOK AHEAD: US Macro Week Ahead: Nonfarm Payrolls On Friday

- Consensus for Friday’s nonfarm payrolls report currently eyes a somewhat resilient 60k monthly increase in April, considering some estimate the breakeven pace could be closer to zero this year.

- 60k would be similar to the three-month average of 68k to March (an eleven-month high) although that hides what have been some particularly volatile readings with 178k in March, -133k in Feb and 160k in Jan. Recent net strength has been an improvement but not enough to suggest that employment gains are doing anything but treading water, with payrolls up only 0.2% Y/Y.

- Correlation with monthly payrolls growth may be weak but higher frequency labor indicators look robust: weekly ADP has been equivalent to ~160k monthly private payrolls growth in recent weeks, whilst initial claims have nudged up compared to recent reference period weeks but continuing claims continued to push together. More puzzlingly, but not directly representative of this payrolls reference period, initial claims have since dropped to their lowest single week level on a seasonally adjusted basis since 1969.

- Consumer perceptions of the labor market meanwhile remain at vulnerable levels although have stabilized since February’s Conference Board labor differential touched a low since early 2021.

- The unemployment rate will continue to be watched closely, currently seen at 4.3% a week out from the release after it surprisingly hit a nine-month low of 4.26% in March to prove that headline payroll gains were no fluke. The median FOMC participant forecast an u/e rate of 4.4% in 4Q26 before 4.3% in 4Q27 in the March SEP.

US TSYS: Late SOFR/Treasury Option Roundup

SOFR & Treasury options trade outlined below: sporadic volumes with some decent short-term/weekly options in 10s and large June 10Y call buyer in the second half. Underlying futures modestly higher as May gets underway, upper half of narrow overnight range. Projected rate pricing largely steady vs. late Thursday lvls (*): Jun'26 at -1.9bp (-1.1bp), Jul'26 at -2.9bp (-2.9bp), Sep'26 at -3.9bp (-3.4bp), Oct'26 at -3.4bp (-3.9bp), Dec'26 -1.3bp (-2.3bp). First half of 2027 holding around +1.6bp to +5.9bp.

- SOFR Options:

- 2,000 0QN6 95.00 puts, 1.5 ref 96.34

- +2,500 0QM6 95.75 puts, 3.5 vs. 96.285/0.12%

- +2,000 SFRM6 96.31/96.37 3x2 put spds, 5.5

- +6,000 SFRK6/SFRM6 96.43 call spds, 1.25

- +10,000 0QV6 95.93/96.18 put spds, 6.5 ref 96.445

- -10,000 0QM6 96.25/96.37 call spds, 6.5 ref 96.305

- -4,000 0QM6 97.50calls, 0.5

- -5,000 0QM6 96.62/96.87 call spds, 2.0 ref 96.27

- -4,000 SFRU6 96.37/96.62 call spds vs. 96.00 put, .25 net

- 18,000 SFRM6 96.43 calls, 1.5 ref 96.35

- 2,500 SFRN6 96.31/96.43/96.68/96.81 call condors, 4.0 ref 96.335

- -1,000 SFRU6 96.06/96.31 put spds 0.5 over 2QU6 95.81/96.06 put spds

- Treasury Options

- 3,000 TYM6 109.5/110.5 2x1 put spds ref 110-23

- +50,000 TYM6 111.75 calls, 9 reef 110-23/0.17%

- +27,700 Wed/wkly TY 110 puts, 5 ref 110-16.5 (exp 05/06)

- +50,000 Wed/wkly TY 110.25 puts, 7

- over +22,000 wk2 TY 109.5/110.25 put spds, 10

- 8,000 Wed/wkly TY 109.5/110.25 put spds, 5 ref 110-17.5

- -1,500 TYN6 111 calls, 41 ref 110-13

- 1,800 FVN6 110 calls ref 107-24.75

- -3,475 FVU6 110 calls, 12 ref 107-24.75

- -6,950 FVU6 105 puts, 12.5 ref 107-24.75

- +3,500 FVU6 108 calls, 50.5 ref 107-24.75

- over +10,500 USM6 109 puts, 9 ref 112-31

- 2,500 wk2 TY/wk3 TY 110.5 call spds