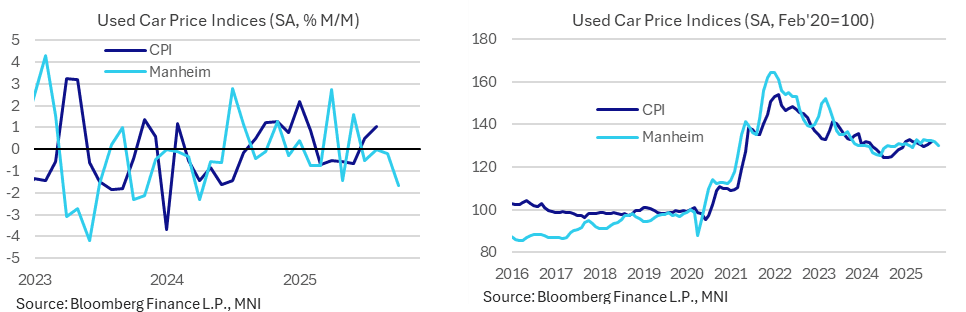

US DATA: Manheim Used Car Prices Slip In Mid-Month Estimate

Oct-17 16:13

- Manheim wholesale used vehicle prices fell -1.6% M/M from September in the first 15 days of October, as usual on a mix-, mileage- and seasonally adjusted basis.

- It leaves a gain of just 0.4% from the full month of Oct 2024.

- From the press release (link): “Wholesale values started to show weakness in late September, and that has carried over into the first half of October, as price depreciation trends start to get back to normal levels,” said Jeremy Robb, deputy chief economist for Cox Automotive. “Declining retail sales in late September typically signal that we could see softer wholesale demand, a pattern holding at Manheim. While October typically shows the year’s strongest depreciation, current weekly declines are running higher than normal for this month, giving back some of the unusual price strength we maintained through most of 2025.”

- It follows -0.2% M/M in the full month of September, 0.0% in Aug and -0.5% in July.

- This latest provisional weakness clearly won’t show up in next week’s September CPI report, but the lags from this wholesale data suggest downside risks for CPI used car prices for Sept compared to what was a 1.0% M/M increase in August, with a pipeline of softer prices ahead.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWEDEN: Government Nudges 2026-27 GDP Forecasts Higher Ahead Of Budget Bill

Sep-17 16:09

Bloomberg report small upward revisions to the government's GDP growth forecasts for 2026 and 2027:

- "*SWEDISH GOVT STILL SEES GDP GROWTH OF 0.9% IN 2025

- *SWEDISH GOVT SEES GDP GROWTH OF 3.1% IN 2026; SAW 3% IN AUG.

- *SWEDISH GOVT SEES GDP GROWTH OF 2.6% IN 2027; SAW 2.5% IN AUG.

- *SWEDISH GOVT UPDATES GROWTH FORECASTS IN WEBSITE STATEMENT" - bbg

It comes ahead of Monday's full presentation of the 2026 Budget Bill. See the MNI Preview published earlier today: https://media.marketnews.com/MNI_2026_Swedish_Budget_Preview_250917_d44c526621.pdf

US STOCKS: Midday Equities Roundup: DJIA Outperforms Ahead FOMC Policy Annc

Sep-17 16:05

- Stocks trade mixed ahead midday Wednesday, the DJIA outperforming weaker S&P emini and Nasdaq indexes, holding to generally narrow ranges in the leadup to the FOMC policy announcement at 1400ET.

- Currently, the DJIA trades up 319.32 points (0.7%) at 46078.41 (record high of 46137.20 on Sep 11), S&P E-Minis down 7.75 points (-0.12%) at 6659.75, Nasdaq down 118.5 points (-0.5%) at 22215.66.

- Information Technology and Communication Services sector shares underperformed in the first half: tech stocks under pressure after reports China authorities have banned the sale of Nvidia chips to top technology firms: Broadcom Inc -3.50%, Western Digital -2.95%, Palantir Technologies -2.94%, NVIDIA -2.72% and Oracle -2.66%.

- Interactive media and entertainment shares weighted on the Communication Services sector: Warner Bros Discovery -1.37%, Alphabet -1.33%, Meta Platforms -1.03% and Live Nation Entertainment -0.67%.

- On the positive side, Financial and Consumer Staples shares led gainers in the first half, banks and services stocks buoyed the former: American Express +2.57%, US Bancorp +2.31%, MSCI +2.19%, Citizens Financial +2.07%, W R Berkley +2.02% and Global Payments +1.91%.

- Meanwhile, retail sellers held modest gains Dollar Tree +3.04%, Walmart +1.95%, Kenvue +1.93%, J M Smucker +1.67% and Brown-Forman +1.50%.

SOFR OPTIONS: Midcurve SOFR BLOCK Update, Separate Oct'25 calls

Sep-17 15:34

Two-way call flow ahead midday as underlying futures inching lower. Projected rate cut pricing cools slightly vs. early morning levels (*): Sep'25 at -25.8bp (-27.1bp), Oct'25 at -45.1bp (-46.4bp), Dec'25 at -67.2bp (-69.1bp), Jan'26 at -80.6bp (-82.9bp).

- +20,000 SFRV5 96.50 calls, 2.25 vs. 96.345/0.20%

- Block/screen -75,000 0QZ5 97.00/97.25 call spds, 10.0