US OUTLOOK/OPINION: Macro Since Last FOMC: Growth - Slightly Softer Hard Data

- Whilst now particularly stale, we start with latest estimates of Q1 national accounts as the revisions in the second update made on May 29 only partly played out as Fed Chair Powell had suggested at the May press conference.

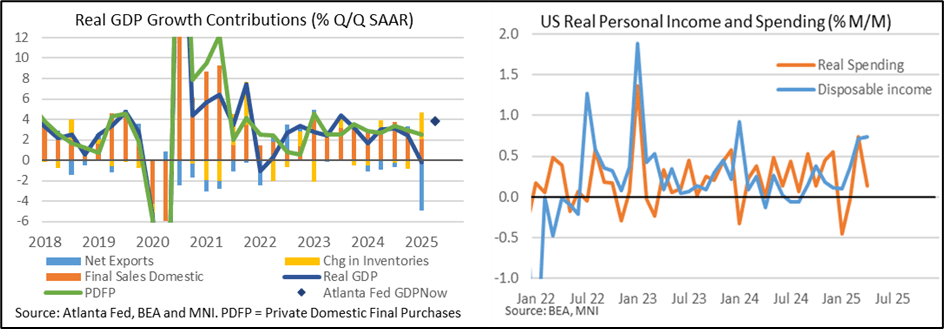

- Real GDP growth was near enough unrevised at -0.24% annualized (vs an initial -0.27%) in Q1 to confirm a sidelining in GDP after 2.4% in Q4 and 3.1% in Q3. There were large offseting revisions though; personal consumption was surprisingly cut from 1.8% to 1.2% annualized, dragging 0.4pp from GDP growth in the process, but fully offset by an even larger boost from inventories on tariff front-running. It left inventories adding 2.6pps to GDP growth compared to the huge -4.9pp drag from net exports.

- Powell had said that it’s “very likely you'll have restatements of the first quarter. It'll turn out that consumer spending was higher. It will turn out that inventories were higher. And so you'll see -you'll see those data revised up. It may actually go into the third quarter, too. And so I think it's going-this whole process is going to, a little bit, make it harder to make a clean assessment of U.S. demand." One takeaway that can we make though is that private domestic final purchases - a category Powell has previously focued on – is now estimated to have increased 2.5% annualized in Q1 vs the 3.0% referenced by Powell at the last meeting for what at the time had impressively looked like no moderation from the 3.0% averaged through 2024.

- New data also reveal that gross domestic income contracted -0.2% annualized in Q1, the weakest in nine quarters for a sharp reversal from Q4’s twelve-quarter best of 5.2%, in signs of broader economic weakness that can’t just be attributed to lower net exports.

- More timely hard data meanwhile have shown resilience in consumer spending and especially incomes, although softer business activity.

- Specifically, real consumer spending was a little better than expected and still managed to increase 0.1% M/M in April after a strong 0.7% M/M in March, whilst real personal disposable incomes surprisingly increased a second consecutive 0.7% M/M. While there were some worrying signs in terms of latest consumer momentum, particularly in services purchases, the employee income growth which has driven much of the economic expansion has not shown any signs of abating going into Q2. The May retail sales report lands on day one of the two-day FOMC meeting.

- On the capital goods side, core shipments saw a modest pullback with -0.1% M/M in April after two strong months that match tariff front-running more broadly. However, core orders point to more notable weakness ahead in production with -1.5% M/M for the single weakest month since early 2023. Add in a larger than expected correction lower in imports in April after Q1’s surge and the Atlanta Fed’s GDPNow currently projects real GDP growth rebounding with 3.8% annualized in Q2.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: Moody's Downgrades US's AAA Rating As Deficits Seen Ballooning

Moody's has downgraded the US's long-term credit rating to Aa1 trom Aaa. The move may not have been fully expected today. But it was the last holdout among they S&P and Fitch to demote the USA from the top rating, and they placed negative outlook on the US last year (now stable). Fiscal deterioration, both past and anticipated as Congress wrangles with the Republican fiscal bill, is cited as the key factor. From the release (link):

- “While we recognize the US’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics."

- "This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns...We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration."

- "If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade. As a result, we expect federal deficits to widen, reaching nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation."

- "We anticipate that the federal debt burden will rise to about 134% of GDP by 2035, compared to 98% in 2024."

- "Federal interest payments are likely to absorb around 30% of revenue by 2035, up from about 18% in 2024 and 9% in 2021. The US general government interest burden, which takes into account federal, state and local debt, absorbed 12% of revenue in 2024, compared to 1.6% for Aaa-rated sovereigns."

US FISCAL: "Extraordinary Measures" Continue To Dwindle Amid Debt Impasse

The "extraordinary measures" available to Treasury to stave off a debt default were down to $82B as of May 14, per a Treasury Department release today.

- That compares unfavorably with a high of $335B in January when the debt limit impasse began. Combined with $562B in Treasury cash on hand, though, after April's large tax intakes, that makes for around $644B in available resources before the "x-date" is reached.

- Resources are gradually being eroded since reaching nearly $800B in mid-April.

- Per Tsy Sec Bessent's letter to Congress last week, "after reviewing receipts from the recent April tax filing season, there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July, before its scheduled break, to protect the full faith and credit of the United States."

CANADA DATA: Sales Activity Points To Potential Marking Up Of GDP Ests

There was mixed news on the housing and wholesale/manufacturing sales fronts this week, which on net look to slightly upwardly bias Q1 GDP estimates, pending next week's retail sales reading.

Housing starts blew through expectations at 278.6k in April (226.2k expected, 214.2k prior). This came after building permits fell a worse-than-expected 4.1% M/M in March as reported Wednesday.

- Meanwhile, he Canadian Real Estate Association reported existing home says April sales unexpectedly contracted -0.1% M/M (+1.0% expected, -4.8% prior). Sales are now down 9.8% Y/Y, while prices fell 1.2% M/M (3.6% Y/Y on the price index). (Link)

- Overall, confidence appears subdued, which is likely to translate into subdued activity.

On the sales front, March data was soft but positive versus expectations and could add a slight upward drift to Q1 GDP expectations.

- Manufacturing sales were less negative than expected at -1.4% M/M (-1.9% expected/flash estimate, -0.2% prior rev up 0.4pp). The decline was led by primary metals -6.5%, an area hit by U.S. tariffs, and oil -4.2%. Overall Q1 factory sales grew +1.6% vs prior +1.1%.(Link)

- Wholesales ex-petroleum and grains rose 0.2% in March, vs the advance estimate / consensus -0.3%. Sales volumes fell 0.3%. Overall Q1 wholesales rose 2.5%, led by machinery/equipment and autos/parts.