ECB: Macro Since Last ECB: Growth - Domestic Demand Falls After Solid Run [1/2]

Sep-10 17:05

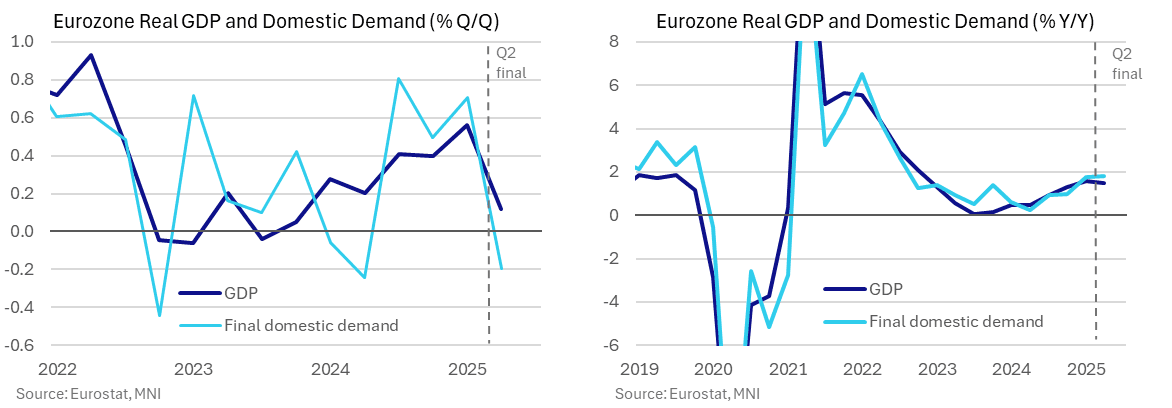

- Released shortly after the July ECB meeting, real GDP growth was a little better than analysts expected in the Q2 advance release at 0.1% Q/Q (cons 0.0) after a strong 0.6% Q/Q in Q1. Subsequent revisions haven’t materially altered this trend, if anything marginally on the stronger side with the Y/Y rounding up to 1.5% Y/Y.

- The recent final release put real GDP growth at 0.12% Q/Q in Q2, helped by a large +0.5pp coming from change in inventories whilst final domestic demand dragged -0.2pps for its joint largest decline since late 2022.

- The latter points to a marked cooling in underlying demand although it does follow a strong 0.7pp in Q1 and 0.6pp averaged in 2H24. As such, final domestic demand growth at 1.8% Y/Y remained a little above that of real GDP growth.

- The final report also showed that nominal GDP grew 0.8% Q/Q (vs 0.7% prior) and 4.0% Y/Y (vs 3.9% prior) in Q2. On a sequential basis, Q2 nominal growth was mostly inflationary – real growth was 0.1% Q/Q while GDP deflator growth was 0.7% Q/Q. However, on an annual comparison there is a growing contribution from real growth to nominal GDP, reflecting a gradual recovery in activity as ECB past rate cuts feed through the system (real growth was 1.5% Y/Y in Q2, versus deflator growth of 2.5% Y/Y).

- We calculate that profits contributed 0.6pp to annual nominal GDP growth after just 0.1pp in Q1 and negative contributions in the three quarters prior, with the impact of US tariffs on Eurozone exporters' profits key to watch in the quarters ahead.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Steady Near-Term Rate Path Ahead Of Tomorrow’s US CPI

Aug-11 17:03

- Fed Funds implied rates for near-term meetings have seen little movement so far today, with focus firmly on tomorrow’s CPI report.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Aug2025_2fe4cdf4a1.pdf

- Cumulative cuts from 4.33% effective: 22bp Sep, 37.5bp Oct, 58bp Dec, 69bp Jan and 81.5bp Mar.

- The SOFR implied terminal yield of 3.10% (SFRH7) is 1bp lower after Friday’s 3.11% marked the highest since the July NFP report. It has in recent days ticked to just under five cuts priced from current levels.

- We see more sensitivity to a downside surprise in July CPI, particularly in core goods components seen sensitive to tariffs. That would set up a replay of the 2024 episode in which after holding in July, the FOMC cut 50bp in Sept (a decision which was, going into the meeting, a “close call” vs 25bp) after a July jobs report saw the u/e rate rise by 0.2pp to 4.25%, even as core PCE appeared to stabilize at 2.6/2.7% Y/Y.

- Next scheduled Fedspeak comes after US CPI, with Barkin (non-voter) at 1000ET and Schmid (’25 voter, hawk) at 1030ET.

BONDS: EGBs-GILTS CASH CLOSE: Gilts Outperform Ahead Of Labour Data

Aug-11 17:01

Gilts outperformed Bunds Monday ahead of key UK labour market data.

- The session low for yields was set in early trade, with some focus on the potential disinflationary implications of a resolution to the Russia-Ukraine conflict ahead of a Trump-Putin meeting scheduled for end-week.

- That said, the pullback in yields looked corrective in nature, coming after Friday's rise and amid limited macro / data / headline news flow. Yields crept up for most of the remainder of the session.

- That left the German curve relatively unchanged on the day, though Gilts benefited in part from a KPMG-REC report on jobs suggesting weak labour market dynamics / restrained wage growth.

- Periphery/semi-core EGB spreads closed mixed, with Spain outperforming and Greece underperforming. MNI published an exclusive on Greek issuance ("Greek 2026 New Issuance Lower End Of EUR8-10 Bln-Source").

- Tuesday's scheduled highlight is the UK labour market report. MNI's preview is here (PDF): primary focus is on private regular average earnings which are expected at 4.8%Y/Y in the 3-months to June.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 1.964%, 5-Yr is up 0.6bps at 2.289%, 10-Yr is up 0.6bps at 2.696%, and 30-Yr is up 2bps at 3.226%.

- UK: The 2-Yr yield is down 3.6bps at 3.863%, 5-Yr is down 3.6bps at 4.001%, 10-Yr is down 3.6bps at 4.565%, and 30-Yr is down 3.6bps at 5.392%.

- Spanish bond spread down 0.3bps at 56.4bps / Greek up 1.1bps at 65.3bps

EURUSD TECHS: Making Further Progress

Aug-11 17:00

- RES 4: 1.1851 High Sep 10 2021

- RES 3: 1.1829 High Jul 01 and the bull trigger

- RES 2: 1.1789 High Jul 24

- RES 1: 1.1699 High Aug 7

- PRICE: 1.1608 @ 15:16 BST Aug 11

- SUP 1: 1.1401 Low Jul 30 and a bear trigger

- SUP 2: 1.1373 Low Jun 10

- SUP 3: 1.1313 Low May 30

- SUP 4: 1.1184 38.2% retracement of the Feb 3 - Jul 1 bull cycle

EUR/USD edged higher to a new recovery high Thursday, before fading into the close. Price has cleared the post-NFP high to keep the recovery off the late July pullback low intact. This works against the bearish backdrop that’s dominated the pullback from 1.1829. The break of firm resistance into 1.1619, the 20-day EMA, is signaling greater odds of a further reversal higher. Major support below rests at 1.1373 next, the Jun 10 low.

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank

Schatz

Bobl