GILT TECHS: (M6) Corrective Phase Intact For Now

* RES 4: 91.52 High Mar 10 * RES 3: 91.00 Round number resistance * RES 2: 90.74 50.0% retracement o...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

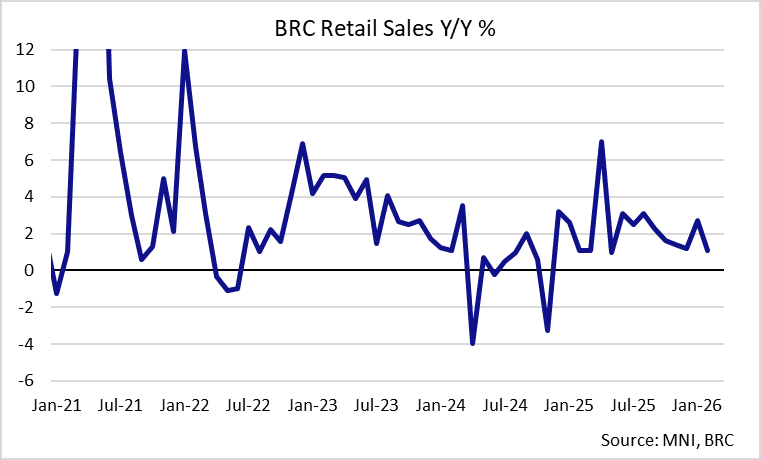

UK DATA: BRC Retail Sales Softer in February Due to Wet February Weather

BRC retail sales growth dropped to 1.1% Y/Y in February (2.7% Jan, 1.2% Dec), unwinding some of the strong January rise (which was the highest rate since last August). This comes after last week's poor BRC footfall data (the weakest since early 2025), with wet weather highlighted as a driver of the weakness in both releases. Both food and non-food sales growth fell, now sitting below the rates seen in December.

- Although inflation has helped boost headline growth in recent releases, the large reversals here (and negative growth in non-food) point to some meaningful underlying weakness.

- Food sales slowed to 2.9% Y/Y (3.8% Jan, 3.1% Dec), propped up by high food inflation (as has been the case in recent releases), with the BRC noting that "Food sales were flat in real terms".

- Non-food sales fell back to negative at -0.4% Y/Y (1.7% Jan, -0.3% Dec), with the largest negative contributions coming from clothing, footwear, and "other non-food" retailers. BRC footfall data released last weak pointed to poor clothing/footwear sales, driven by one of the wettest Februarys on record.

- Comments from the press release: "February’s grey, wet weather hit retail sales hard. Spending was weak across most categories, online and instore, as households pulled back after Christmas and January’s rebound. Food sales were flat in real terms as shoppers tightened their belts."

- The press release also highlights some offset from Valentine's Day providing some support to jewellery, watches and perfume sales, and that "Health and wellbeing related purchases helped to drive modest monthly retail sales growth".

- On consumer sentiment, the release adds: "shopper sentiment still saw a modest lift thanks to easing inflation and news of a forthcoming 7% cut in energy prices, offering a rare sense of financial reprieve. Seasonal spikes around Valentine’s Day and Pancake Day boosted at home dining but failed to translate into volume growth. As March begins, the outlook is deteriorating ... whilst the conflict in the Middle East is strengthening concerns over fuel costs, which could impact food price inflation, if the situation continues."

- While it could have been expected for online sales to be given a boost by the wet weather, this doesn't look to have come through in today's data: "Online Non-Food sales decreased by 1.3% Y/Y in February, against a growth of 1.9% in February 2025. This was below the 12-month average growth of 1.2% ... The online penetration rate (the proportion of Non-Food items bought online) decreased to 36.1% in February from 36.3% in February 2025. This was below the 12-month average of 37.3%."

- The reporting period covers the four weeks 1 - 28 Feb 2026, the same as the upcoming ONS retail sales data (due Fri 27th March), which saw a strong upside surprise in Jan (1.8% M/M vs 0.2% cons, 0.4% Dec), after positive signals from BRC data. Weak footfall and now retail sales data from the BRC add some downside risk to the official ONS print, combined with an already likely expected monthly reversal lower.

EUROZONE ISSUANCE: EGB Supply Daily

The EU is likely to hold a syndication today while Austria and Germany will hold auctions. Germany will return to the market tomorrow alongside Portugal while Ireland and Italy will look to follow on Thursday. We look for gross issuance of E28.6bln for the week, down from E40.6bln (ex-retail) last week.

- The EU has released a mandate for a new 10-year Dec-36 EU-bond. The transaction will be launched “in the near future, subject to market conditions”. This is a usual line for most issuers when mandates are released, but the EU normally commits to “tomorrow” in its mandates (which would have meant a transaction today). We still do expect a transaction today but there is a chance it is pushed to later in the week. We expect a transaction size of E7-9bln.

- The mandate was in line with our expectations. Note that we wrote in our EGB Issuance, Redemption and Cash Flow Matrix last week that “we pencil in the launch of a new 10-year. This may be as a single line syndication or potentially alongside a tap or a new 20-year issue.”

- Austria will kick auction issuance off for the week this morning for a combined E1.725bln. On offer will be second auction reopening of the 2.80% Sep-32 RAGB (ISIN: AT0000A3NY15) after it was launched via syndication in August and the on-the-run 10-year 3.20% Feb-36 RAGB (ISIN: AT0000A3RVH9).

- Germany will also come to the market today with E5bln of the 2.10% Mar-28 Schatz (ISIN: DE000BU22122) on offer.

WTI TECHS: (J6) Key Support Zone Intact For Now

- RES 4: $125.00 - Round number resistance

- RES 3: $123.68 - High Jun 14 ‘22 (cont) and a key resistance

- RES 2: $120.00 - Psychological round number

- RES 1: $100.34/119-48 - 50.0 of the Mar 9 daily range / High Mar 9

- PRICE: $89.53 @ 06:35 GMT Mar 10

- SUP 1: $89.43 - Intraday low

- SUP 2: $72.61 - 20-day EMA

- SUP 3: $66.39 - 50-day EMA

- SUP 4: $63.60 - Low Feb 26

A volatile impulsive bull wave in WTI futures remains intact. From a technical analysis standpoint alone, the sharp pullback from Monday’s high is not a surprise, given that the uptrend was in an extreme overbought position. The move down is allowing this overbought condition to unwind. A key support zone to monitor is $72.61 - $66.39, the area between the 20- and 50-day EMAs. A clear break through this area would signal a possible trend reversal.