RIKSBANK: Lowers Deposit Requirement To SEK35bln

"The Riksbank has decided that banks, other Swedish credit institutions and Swedish branches of fore...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT TECHS: (M6) Corrective Phase Intact For Now

- RES 4: 91.52 High Mar 10

- RES 3: 91.00 Round number resistance

- RES 2: 90.74 50.0% retracement of the Feb 27 - Mar 23 bear leg

- RES 1: 90.18 Intraday high

- PRICE: 89.99 @ 08:22 BST Apr 8

- SUP 1: 88.71 20-day EMA

- SUP 2: 87.59 Low Apr 7 and a key near-term support

- SUP 3: 87.13 Low Mar 30

- SUP 4: 85.91 Low MAr 23 and a key support

Recent gains in Gilt futures are considered corrective. However, note that the gap higher today signals potential for a stronger short-term recovery. A continuation higher would open 90.74 next, a Fibonacci retracement, ahead of the 91.00 handle. The initial key short-term support to watch lies at 87.59, the Apr 7 low. Clearance of this level would be a bearish development and signal the end of the corrective cycle.

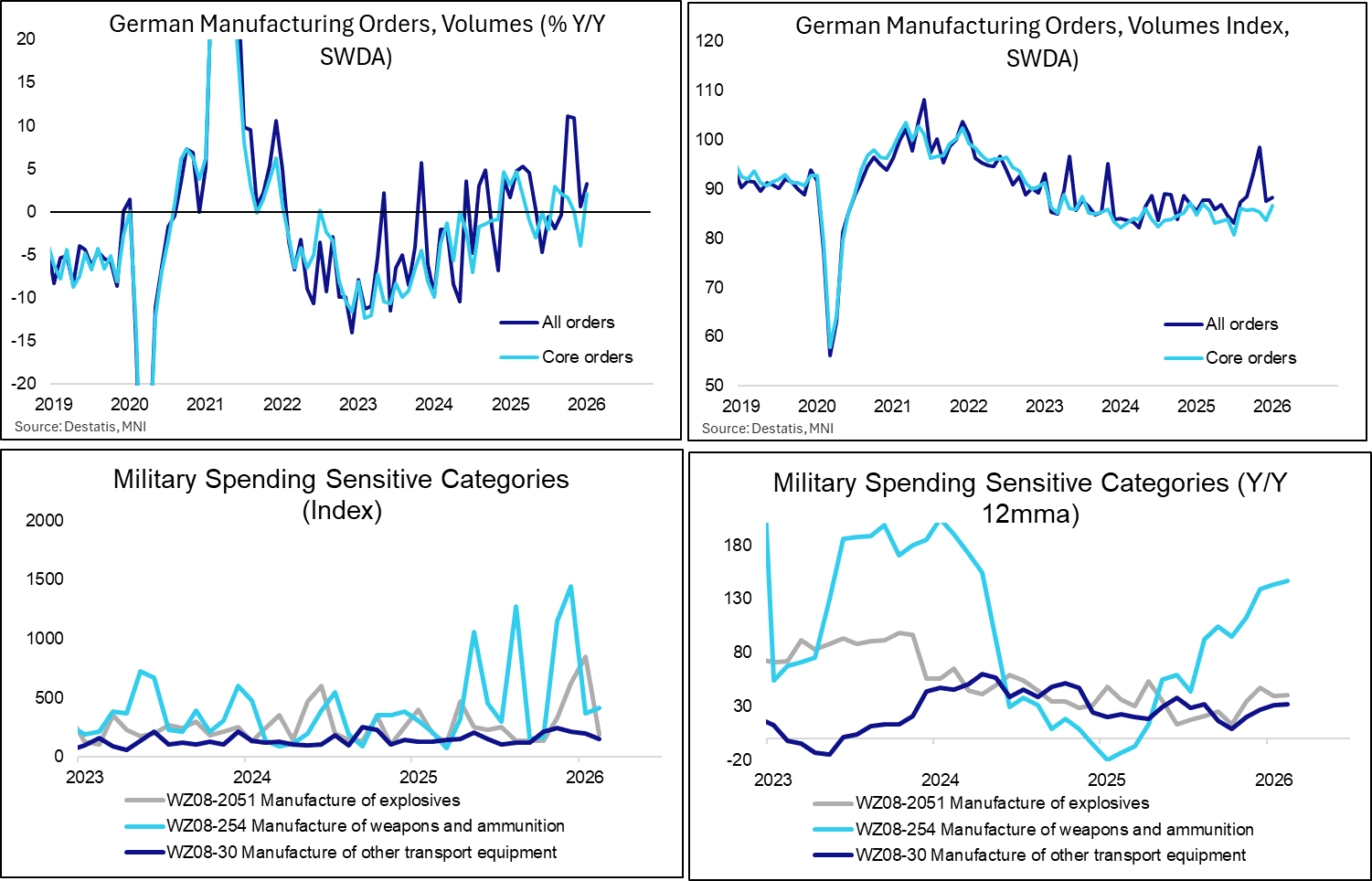

GERMAN DATA: Core Factory Orders More Resilient Than Headline In February

German factory orders were weaker than expected in February, rising 0.9% M/M (vs 3.0% cons, -11.1% prior). The core series, which excludes large-scale orders, was more resilient, posting a 3.5% M/M increase (vs -1.9% in Jan, -0.7% in Dec). The data provides a snapshot of the German industrial outlook before the Iran war started – it will be interesting to see how March’s orders are affected by both higher energy prices and increased geopolitical uncertainty.

- On a calendar and seasonally adjusted basis, headline orders rose 3.3% Y/Y (vs a downwardly revised 0.6% prior), while core orders increased 2.1% (vs -3.0% prior). Core orders have shown some signs of life in recent months, but more broadly speaking have flatlined since 2023.

- Destatis notes that “The positive development of new orders in manufacturing in February 2026 was primarily attributable to the substantial increase seen in the automotive industry (+3.8% on the previous month, seasonally and calendar adjusted). The increases in new orders for the manufacture of textiles (+45.2%) and the manufacture of basic metals (+3.7%) also had a positive impact on the overall result. By contrast, the decline registered in the manufacture of other transport equipment (aircraft, ships, trains, military vehicles; -25.9%) had a negative impact.”

- While there is certainly evidence of increased defence-related orders since Chancellor Merz’s March 2025 announcement, momentum has waned a little in recent months. Indices of orders in weapons and ammunition and explosives remain highly volatile. It will take some time for increased orders to be reflected in actual production figures (and therefore GDP).

- Real turnover in manufacturing fell 0.5% M/M in February (vs 0.7% in Jan, downwardly revised from 1.5%). This points to downside risks to tomorrow’s February industrial production report (0.7% cons).

EURIBOR OPTIONS: Call Spread buyer

ERU6 97.75/97.87cs bought for 2.5 in 7.5k.