RBA: Lowe: Persistent Services Inflation “Here”, Tightening Not Done

RBA Governor Lowe has spoken to the Morgan Stanley Summit regarding the “Narrow Path” that the RBA is on to get inflation back to target while keeping as many of the labour market gains as possible. But it remains “resolute” in its goal of returning inflation to target. He cited the global economy, household spending, unit labour costs and inflation expectations as the key areas that will determine future rate decisions.

- The tightening this cycle is “working” and “inflation is coming down” and while there are falling inflation pressures stemming from global markets, services prices, rents, electricity prices and unit labour costs (ULC) remain a concern.

- The decision to hike rates in June was to give “greater confidence” that inflation will return to target “within a reasonable timeframe”. It was also in response to an upside risk to inflation from persistent services inflation, which he stated is now “here” and not just an overseas phenomenon. Recent information pointed to inflation, wages and house prices being higher than assumed in the RBA’s May forecasts.

- The Board will be looking at global developments including core services and the recovery in China.

- There is a lot of uncertainty around the consumption outlook with higher rates and cost of living on one hand and high population growth, savings buffers and strong employment on the other. The RBA will look at retail sales, house prices, employment and mortgage arrears.

- ULC have a close relationship with inflation and is concerning the RBA and Lowe said that “ongoing strong growth in unit labour costs would underpin ongoing high inflation outcomes”.

- Medium-term inflation expectations from financial markets and a RBA survey of unions will be watched closely for signs that inflation is becoming entrenched.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cheaper Start

Cash tsys have opened dealing ~1bp cheaper across the major benchmarks. Local participants are perhaps focusing on the headline number of Friday's NFP which saw the unemployment rate tick unexpectedly lower. TYM3 deals at 115-22, -0-01, with 0-05+ range observed thus far.

- A thin data calendar in Asia today leaves participants on headline watch.

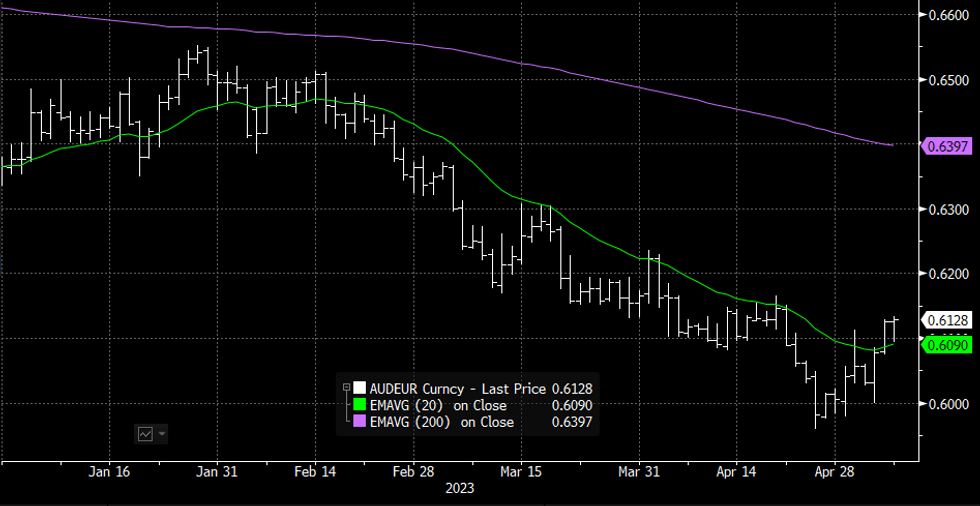

AUD: AUD/EUR: Holding Above 20-Day EMA

Improving risk sentiment on Friday saw AUD/EUR continue to recover from cycle lows, bulls have held above the 20-Day EMA as the pair printed its highest level since April 21.

- We now sit ~3% above cycle lows seen late in April at €0.5959, the 20-Day EMA had been a key resistance for bulls to clear since breaking below the measure in February.

- Bulls now target a break of €0.62, which opens up the 200-Day EMA (€0.6371).

- Bears look to test year to date lows (€0.5959). From here €0.5867 the 50% retracement of the 2020-2022 Bull leg is the next downside support level.

Fig 1: AUD/EUR Daily Spot, EMAs

Source: MNI/Bloomberg

JPY: Yen Weaker Early Doors

Yen is trading lower early doors in the Monday Asia Pac session. We have lost close to 0.30% since the open, putting USD/JPY back into the 135.20/25 region, which is above highs from Friday's session post the US payroll print. Note Japan markets return today after a 3-day break. The yen is underperforming both AUD and NZD, with NZD/JPY back to 85.15/20.

- Headline flow has been light, with some focus likely to be on EU plans to sanction China companies aiding the Russian war with Ukraine (per the FT). Some of the companies are already reportedly sanctioned by the US, so the fallout from a broader risk sentiment perspective may not be large.

- US equity futures opened higher, but are away from best levels. Eminis last just near 4153 (+0.06%).