US TSYS: Little Changed In Asia, Light Data Calendar Bit Fedspeak Due

Jan-16 04:08

TYH6 is dealing at 112-056, -0-01 from closing levels in today's Asia-Pac session.

- US tsys are slightly cheaper in today’s Asia-Pac session after finishing Thursday near session cheaps, with the curves flatter with the 30Y Bond outperforming.

- The market had retreated following lower than expected weekly & continuing claims and higher than estimated Philly Fed Business Outlook & Empire Mfg.

- The Bureau of Economic Analysis has announced updated release dates for delayed data: The Q4 GDP / 2025 second estimate will be published March 13 (was originally scheduled for Feb 26); with the third estimate out April 9 (originally scheduled for March 27). These will follow the advance estimate for the quarter on February 20.

- Friday’s data is limited to Industrial Production & Capacity Utilization at 0915ET. Otherwise multiple Fed speakers are scheduled: Boston Fed Collins welcoming remarks (1050ET), Fed VC Bowman on economy & monetary policy (1100E) and Fed VC Jefferson at 1130ET.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

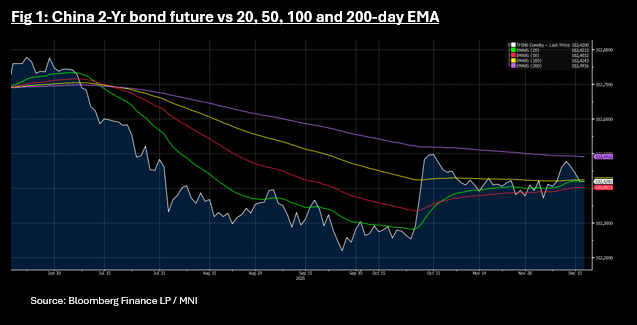

CHINA: Bond Futures Steady as Equities Rebound

Dec-17 03:24

- As equities rebound after two days of losses, bond futures are steady this morning moving only marginally higher.

- The China 10-Yr future is up +0.06 at 107.96 as it nears the 20-day EMA of 107.99.

- The 2-Yr future is up +0.01 at 102.42, atop the 20-day EMA of 102.42. Were it to break below, downside resistance is via the 50-day EMA of 102.40.

- Cash is steady with the 10-Yr at 1.84%, down -0.5bps this morning and the 2-Yr at 1.39%

JGBS: Futures Holding Weaker At Lunchtime Break, JGB Yields Steady

Dec-17 02:41

At the lunchtime break, JGB futures are holding negative, 133.29, -.14 versus settlement levels. Recent lows at 133.18 remain intact, while upticks continue to be faded, with a negative technical bias in play. US bond futures have failed to kick on from the overnight lead in and are down modestly during the morning session in Asia, which may be spilling over to JGBs at the margin.

- JGB yields are little changed in the first part of Thursday dealings. The 10yr was last near 1.97%, up a touch but short of recent cycle highs (close to 1.98%). The 2yr is around 1.07%, as Friday's BoJ meeting outcome comes into focus.

- The market is fully priced for a hike. Beyond December, attention will focus on guidance around the neutral rate, which Ueda has described as "1-2.5%," signalling that policy normalisation is likely to continue gradually rather than end at 1%. See our preview here:

- Earlier data was firmer on the export side and core machine orders, but isn't likely to shift BoJ thinking around the economic backdrop.

CHINA: More of the Same for Policy in 2026

Dec-17 02:35

- An article in the China Securities Journal assess policy in 2025 describing it as 'supportive' suggesting that since the beginning of the year various policy tools have worked together to guide financial institutions to increase their support for the real economy, whilst 'anchoring the goal of stable financial markets.

- Looking at the potential for policy in 2026, the article points to more of the same with the continuation of the current 'moderately loose' monetary policy, adhere to precise policy implementation whilst using flexible tools like RRR cuts and interest rate cuts to promote overall social financing costs.

- On social financing costs, the article points to overall social financing costs being at historical lows with lower loan interest rates thanks to cuts in the 7-day reverse repo rate, whilst lower housing provident fund loan rates are lower also. The weighted average interest rates for new corporate loans was 30bps lower than a year ago.

- The recent Central Economic Work Conference clearly stated that various policy tools, such as reserve requirement ratio (RRR) cuts and interest rate cuts, will be used flexibly and efficiently in what appears to leave room for further RRR and interest rate cuts in 2026.

- The focus on financing costs and banks willingness to lend will support the government's goal of improving domestic demand and target innovative industries viewed as important to the future development of the economy.

- It appears from this article that there is no imminent change to come, rather more of the same as the economy remains on track to achieve the 5% GDP growth target.

- Instead, it appears now that the already 'supportive' policy provides a backstop and could be altered if needed.

- Going forward we continue to monitor social financing costs and lending data as a key insight for future direction of policy.