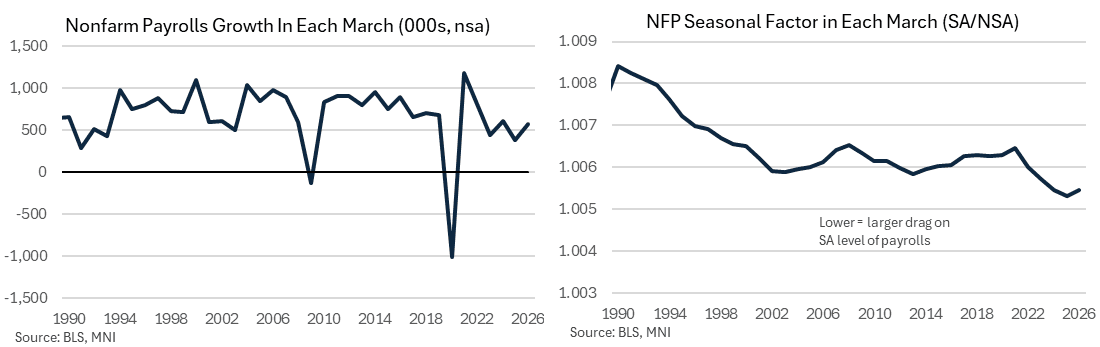

US DATA: Limited Distortions From Birth-Death, Seasonal Adjustments

Even though March's headline payrolls number handily beat expectations, seasonal adjustments and the establishment Birth-Death adjustment were not particularly favorable to the reading.

- The non-seasonally adjusted change in nonfarm payrolls was +571k, coming after +476k. In keeping with March typically being a strong month on an NSA basis, the seasonal adjustment factor was negative for the gains, but at 0.995 was little different than in March 2025 (the chart below shows the reciprocal).

- The BLS's Birth-Death model subtracted 47k (NSA) from payrolls after adding 90k in February, for a 3rd subtraction in 4 months. That compares to -33k in March 2025 and was larger than the -22k average for the last 5 March's.

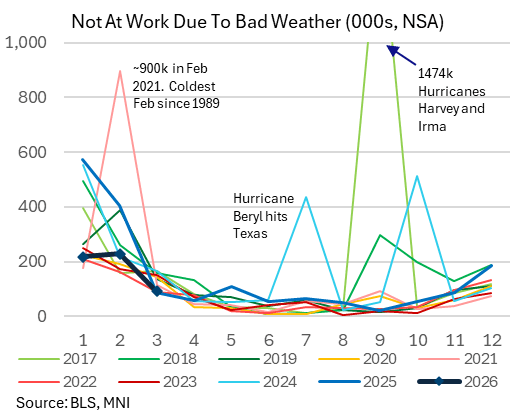

- As far as the Household Survey is concerned, weather wasn't really a factor: 91k (NSA) were not at work due to bad weather, almost identical to the prior year (87k) though slightly lower than the 122k average of the last 5 March's (this year's weather was particularly good for March). The rebound in construction and leisure/hospitality payrolls in March were also suggestive of a more solid-than-usual weather effect after February's depressed figures.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

IRAN: Markets Look for Clues on Conflict Duration as Messaging Stays Firm

Markets saw only a brief reaction to today's NYT piece that quoted sources in saying Iran had used back channels to offer to discuss terms for an end to the conflict - and public-facing messaging from all sides have strongly played down the odds of any near-term resolution. Even with this combative messaging, markets will be looking for any softer tones or further source reports to gauge the duration of the conflict (and thereby the persistence of high energy prices), rather than headlines

Official comments on conflict duration:

- US Sec. of War Hegseth (Weds): More, larger waves are coming, the US is just getting started. Will take all the time [we] need. It could take 4 weeks, it could take 8 or 3.

- US President Trump (Mon): We haven't even started hitting them hard, the big waves haven't even happened. The big one is coming soon.

- Senior Israeli IDF sources (Weds): Two more weeks of bombings across Iran ahead of us, with the plan being to attack thousands of targets

- Iran IRGC spokesman (Weds): Attacks will intensify in the coming days, will strike US and Israeli assets with "greater intensity" in the coming days

- US General Caine (Weds): Operation is complex, dangerous and "far from over"

Unofficial comments on conflict duration:

- NYT sources: US officials either Trump or Iran ready for offramp - at least in short-term. Offer raises questions about whether any Iranian officials could put in place a ceasefire with Tehran gov so unstable

- BBG sources: UAE, Qatar privately lobbying allies for help persuading Trump to reach an offramp, keeping military operations short

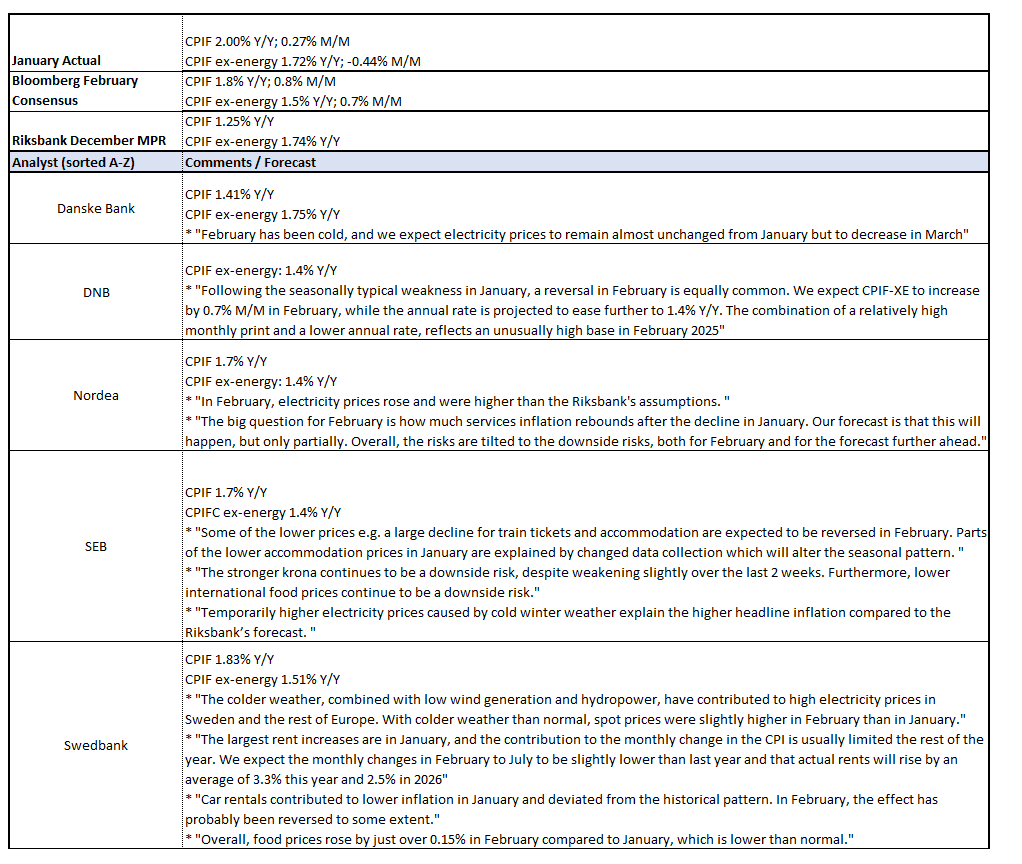

SWEDEN: February Flash Inflation Due Tomorrow Morning, Services Key

Swedish February flash inflation is due tomorrow at 0700GMT/0800CET. Analyst consensus pencils in another deceleration in CPIF ex-energy to 1.5% Y/Y, down from 1.72% in January. If realised this would see the Riksbank’s December MPR forecast error narrow to 0.2pp (vs 0.3pp at present). Underlying inflation pressures continue to appear soft, but we still think several Riksbank board members will need to see a stalling of activity momentum before supporting another rate cut. We noted last week that the details of the Q4 GDP report (which was revised up vs the flash) were solid.

- We think the Riksbank reaction function to recent energy price increases will be similar to the ECB. For now, it’s too early to determine whether the Middle East conflict will generate a material supply shock that requires a monetary policy response.

- The flash inflation release will include preliminary details on COICOP categories and key subcomponent groups (i.e. goods, services, food etc.). This should allow for a more refined market reaction compared to previous flash releases, where only the headline CPIF and CPIF ex-energy readings were provided.

- In January, services inflation was the main downside surprise, with decelerations seen across categories (though this included a change to dental care subsidies)

- The exchange rate was flagged as a downside inflation risk in the Riksbank’s January meeting minutes. Strength seen through 2025 may still be applying pressure to goods/food inflation, though recent weakening has seen the KIX effective exchange rate fully retrace January’s move lower.

- See below for a selection of analyst comments:

SOFR OPTIONS: Short Mar'26 SOFR Calls

- +10,000 0QH6 96.87/97.00 call spds, 3.25-3.5 ref 96.85

- +2,500 0QH6 96.62/97.00 call over risk reversals, 1.0 vs. 96.825/0.30%