STIR: Light Regional Calendar Leaves EUR STIRs Exposed To X-Market Forces

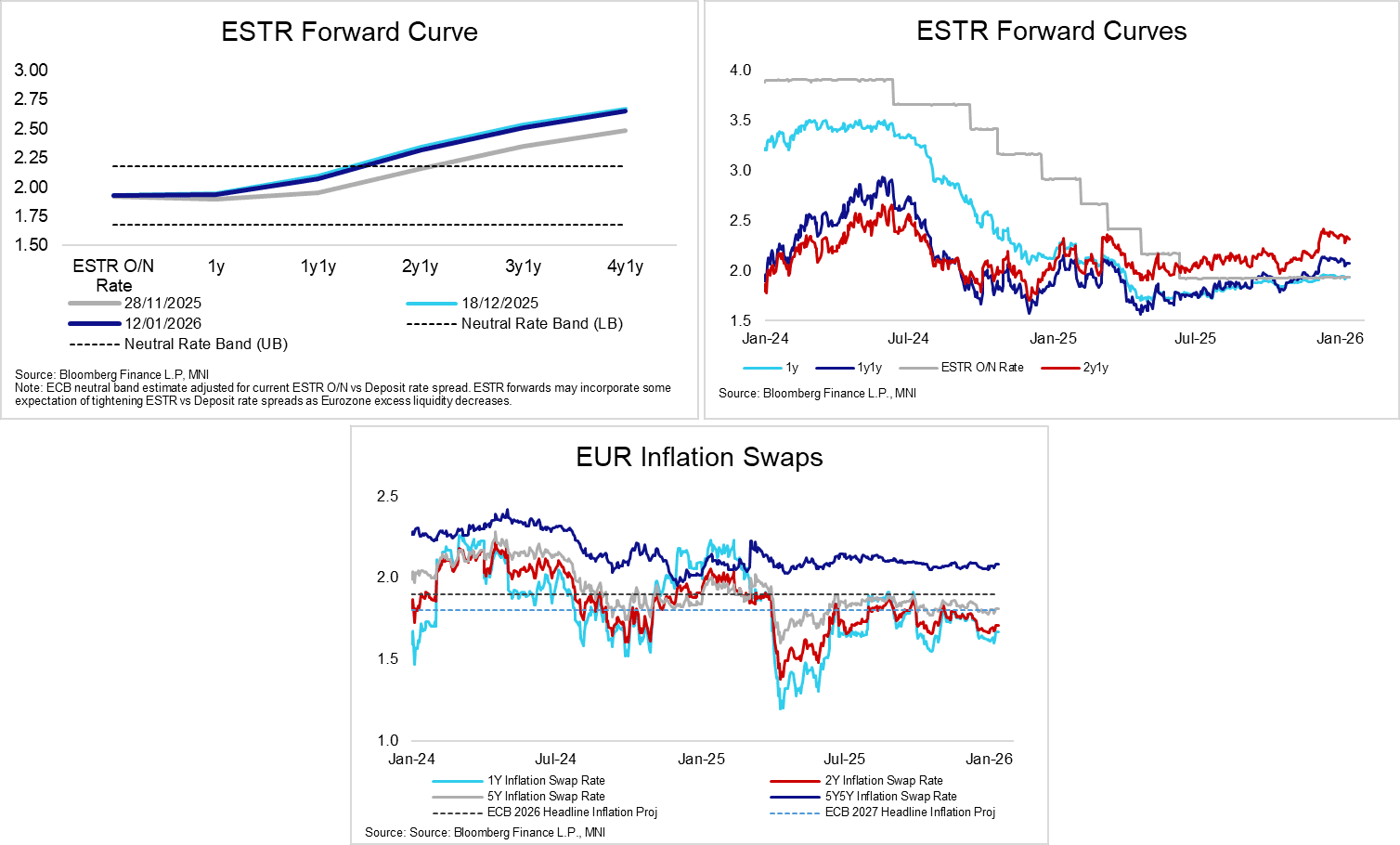

This week’s Eurozone calendar is light, leaving cross-market forces as the likely drivers of EUR STIR price action. Market pricing suggests the bar to a ECB rate change over the next year is unlikely. Although core HICP marginally surprised to the downside last week, more material deviations from ECB projections are required to motivate another cut.

- EUR traded inflation metrics drifted back higher alongside crude futures at the end of last week. Zooming out, the 5y5y inflation swap has been very steady – and close to the 2% target - since October, underscoring the ECB’s view that the policy stance is in a “good place”.

- ECB’s de Guindos speaks in a Fireside chat today. A reminder that de Guindos’ term as Vice President ends in May. The Eurogroup will discuss the six candidates for the VP job at its meeting next Monday, before submitting a recommendation to the European Council. The ECB and the European Parliament will be consulted before a final decision is taken by the European Council.

- ECB-dated OIS price 3bps of easing through September 2026. Meanwhile, Euribor futures are flat to -1.5 ticks through the blues.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (H6) Just Off Cycle Lows

- RES 3: 140.08 - High Jun 13

- RES 2: 139.05 - High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 133.44 @ 15:44 GMT Dec 12

- SUP 1: 133.25 - Low Dec 10

- SUP 2: 132.78 - 2.0% Lower Bollinger Band

- SUP 3: 132.17 - 1.0% 10-dma envelope

Prices traded to new pullback and cycle lows earlier this week, weighed by building expectations of a December BoJ rate hike and a breach of support in futures prices. This affirms the firm downtrend that’s dominated prices since mid-September, and prices will need to challenge resistance before signaling any broader reversal.

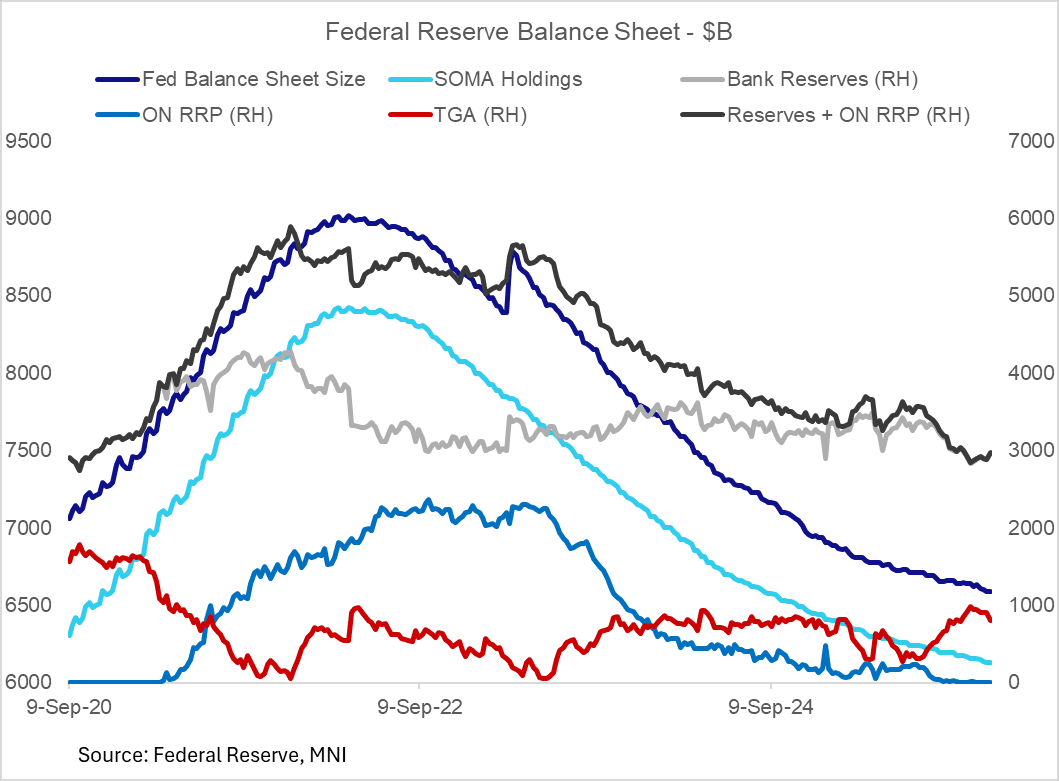

FED: Reserves Fell To "Ample" At Just Under $3T (2/2)

The FOMC's decision this week to immediately initiate reserve management purchases (RMPs) suggests some concern by policymakers over recent funding market issues and potential further volatility at year-end, while also having an eye on building reserve capacity ahead of the major tax date in April.

- The December FOMC statement noted "reserve balances have declined to ample levels" vs abundant previously, and RMPs will be conducted "to maintain an ample supply of reserves on an ongoing basis."

- As of the meeting, reserves stood at just under $3T ($2.97T), perhaps on the high side of most estimates of where the "ample" range had been. Gov Waller estimated in July that "ample" could be closer to $2.7T.

- The $40B / month pace of RMPs is front-loaded and will taper off, with the reserve rebuild set to average about $20-25B/month. (Powell said Wednesday: "We have to keep reserves, call it, constant as a -- as it relates to the banking system or to the whole economy. And that alone calls for us to increase about $20-25 billion per month...It's also happening in the context of a temporary few month front loading to get reserves high enough to get through the -- you know, the tax period in mid-April."

- The NY Fed's guidance: "The Desk anticipates that the pace of RMPs will remain elevated for a few months to offset expected large increases in non-reserve liabilities in April. After that, the pace of total purchases will likely be significantly reduced in line with expected seasonal patterns in Federal Reserve liabilities. Purchase amounts will be adjusted as appropriate based on the outlook for reserve supply and market conditions."

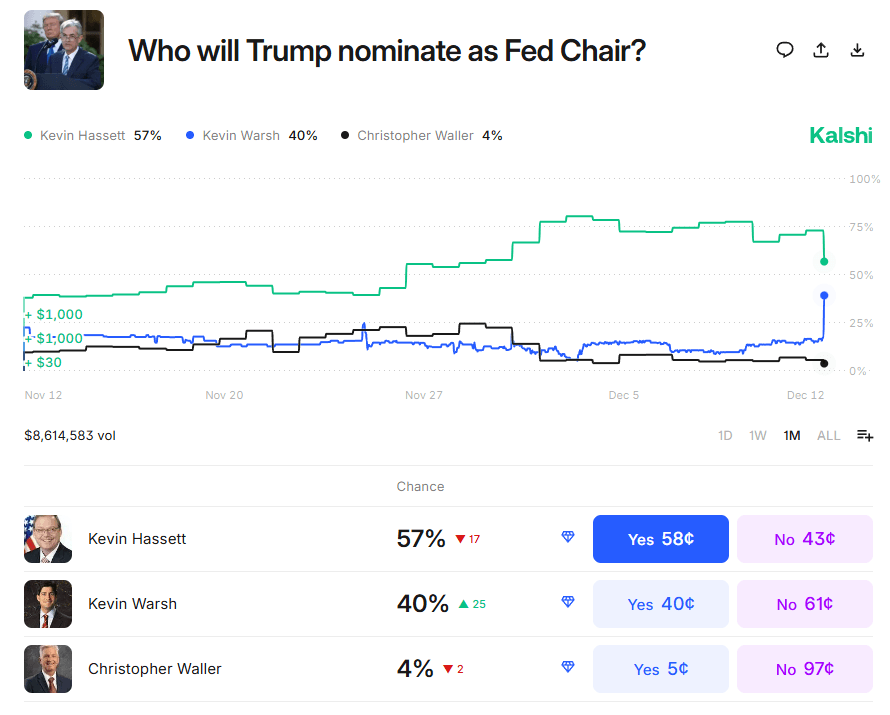

FED: Trump Tells WSJ: Leaning To Warsh Or Hassett As Fed Chair

President Trump has told the Wall Street Journal in an interview Friday that he was leaning toward either Kevin Warsh or Kevin Hassett as his pick for the next Fed Chair.

- Warsh's probability of becoming Fed chair is spiking (40%, up 25pp on Kalshi in the last few minutes) on prediction markets with the interview suggesting the ex-Fed governor is neck-and-neck with previously presumptive favorite Hassett (57%).

- "In an interview with The Wall Street Journal in the Oval Office on Friday, the president said Warsh was at the top of his list. "Yes, I think he is. I think you have Kevin and Kevin. They're both -- I think the two Kevins are great," he said. "I think there are a couple of other people that are great.""

- Additionally Trump tells the WSJ that the next Fed Chair should consult with him on where to set interest rates, and that he pressed Warsh this week on "whether he could trust him to support interest-rate cuts if he were chosen to lead the central bank, according to people familiar with the meeting. Trump, in the Journal interview, confirmed that reporting. "He thinks you have to lower interest rates," Trump said of Warsh. "And so does everybody else that I've talked to." "

- "Asked where he wants interest rates to be a year from now, Trump said, "1% and maybe lower than that." "

- This is not entirely new rhetoric from Trump on rates and the associated litmus test of a low rate preference for the next Fed Chair - as such there's not much market reaction to the news, but the reporting suggests that current Fed officials Waller and Bowman may be out of the running.