OIL: LEAVITT: TRUMP 'VERY INTERESTED' IN ADDITIONAL CARTEL MEASURES

LEAVITT: TRUMP 'VERY INTERESTED' IN ADDITIONAL CARTEL MEASURES - Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Hammer Candle Reversal Signal

- RES 4: 154.39 76.4% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 153.82 1.618 proj of the Sep 17 - 26 - Oct 1 price swing

- RES 2: 152.61/153.27 High Oct 14 / 10 and the bull trigger

- RES 1: 152.17 High Oct 21

- PRICE: 151.76 @ 15:41 BST Oct 21

- SUP 1: 149.38 Low Oct 17

- SUP 2: 148.94 50-day EMA

- SUP 3: 147.82 High Oct 3

- SUP 4: 147.14 Trendline support drawn from the Apr 22 low

The recovery from last Friday’s low in USDJPY is beginning to highlight a stronger bullish signal. The pair has found support below the 20-day EMA and note that Friday’s price pattern is a hammer candle formation. If correct, the pattern signals the end of a corrective pullback that started Oct 10, and highlights the fact that support at the 50-day EMA, at 148.94, remains intact. The bull trigger is at 153.27, the Oct 10 high. The 50-day EMA is key support.

BOC: Canada Analysts Nearly Unanimous That October Cut Still On Track (2/2)

Continuing through Canadian analyst reviews of CPI (the below all expect a 25bp cut on Oct 29) below. MNI's BOC meeting preview will be published on Monday October 27.

- Desjardins: "While the higher‑than‑expected pace of inflation in September may complicate the Bank of Canada’s messaging, a good part of the acceleration in the month can be explained by events a year ago as opposed to what is happening today. As such, we think that headline inflation could comfortably return to around 2% in the fourth quarter, supported by the recent reduction in retaliatory tariffs on goods imports from the US. When combined with the Bank’s downbeat business and consumer surveys, a still elevated unemployment rate and an economy that looks like it might barely manage to escape a recession in Q3, we remain of the view that the BoC will cut the policy rate by another 25 basis points at its upcoming meeting."

- National: "Deputy Governor Mendez's recent speech clearly indicated that the Bank of Canada had made another U-turn in regard to their core measures by stating that CPI-Trim and CPI-Median should no longer be prioritized. For this reason, we will now track these two measures, as well as inflation excluding food and energy (CPIXFET) and the CPIX (the Bank of Canada's former core inflation measure).Taking the average of these four measures, the price increase in September was only 0.24%, which is uncomfortable for the Bank of Canada but much less worrying than the increase in the total index. Over three months, the annualized rate of increase is 2.3%, only a few tenths of a percentage point above the target... As for inflationary pressures, there was no indication in the BOS that businesses felt they had pricing power. In conclusion, we continue to favor a rate cut at the next decision, and the need for further accommodation will depend on the federal budget and a potential de-escalation of trade tensions with the United States."

- RBC: "Inflation continues to run above the BoC's 2% target, but that was also true when the central bank cut the overnight rate in September. The breadth of inflationary pressure did narrow slightly by our count in September. A higher unemployment rate, lower business inflation expectations in the BoC's own Business Outlook Survey, and the removal of most Canadian counter-tariffs, should reinforce the BoC's view that upside inflation risks have eased - and our base-case assumes one more reduction in the overnight rate next week in October...We expect cutting beyond that, into outright stimulative levels of interest rates, will be more difficult with inflation still sticky at an above-target rate and fiscal policy potentially ramping up as a support after the federal budget in early November."

- Scotiabank: "Canadian core inflation measures remain good enough for the BoC to cut next week when properly evaluated in terms of month-over-month trends and breadth...Key is that each of the main core measures of inflation were well within the flexible 1–3% headline inflation target range and were likely overstated by mechanistic seasonal adjustments that may not be appropriate...I think the BoC will work the flexible inflation target range that Macklem keeps emphasizing and deliver easing next Wednesday but with a hawkish sounding and noncommittal feel."

- TD: "Overall, we do not think the September CPI report will be enough to shift the Bank of Canada's assessment on the risks around inflation, and we continue to look for them to deliver another 25bp cut in October. 3m rates of core inflation were more stable between August and September, and inflation pressure were less broad based in the September CPI report. The Q3 BOS also noted that firms are having a more difficult time passing down higher input costs, which should make it easier to look through the stronger performance for CPI-trim/median."

BOC: September CPI Not Major Obstacle To October Cut (1/2)

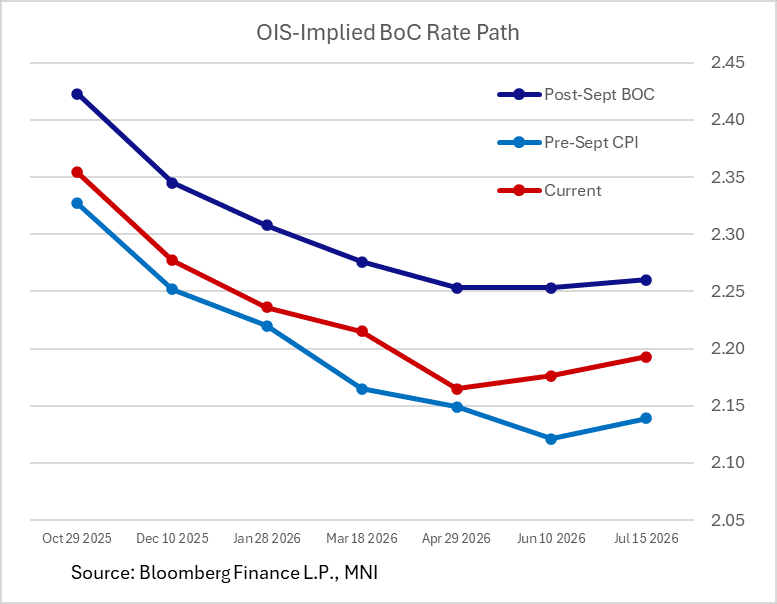

Stronger-than-expected readings across September headline and core CPI metrics has seen expectations of future BOC cuts diminish slightly, with current meeting dated OIS-implied pricing pointing to about 5bp less easing through the next 4 decisions to March 2026.

- That includes just under a 70% probability of a cut at the upcoming October meeting, which fell as far as 62% post-CPI, vs closer to 80% prior to the release. Current BOC meeting-dated OIS implied cumulative rates: Oct -17bp, Dec -25bp, Jan -29bp, Mar -31bp. That's still a more dovish path than seen immediately after the September BOC decision, which saw 21bp of cuts priced through year-end, with the next cut only fully priced by around March.

- The CPI report keeps the upcoming decision in the category of not-a-foregone-conclusion but still likely in favor of a cut. As MNI has pointed out, the headline reading was only slightly above-expected (and even then due largely to volatile energy and food prices), with core goods price pressures looking tame, and inflation breadth (particularly in services) continuing to diminish, suggesting no real obstacle to a cut on October 29 vs what was known before.

- Similar reasoning appears to be held by most of the 7 major Canadian institutions tracked by MNI, of which all but one (BMO) continues to see the BOC cutting rates by 25bp next week even after having considered the September CPI report. Several cited the fact that the BOC has been downplaying the importance of its CPI trim/median measures whose unexpected uptick in September appeared to drive a portion of the hawkish reaction; others note the relatively dovish findings from the Bank's quarterly surveys out Monday..

- That having been said, there are potentially rising risks from this data of a more hawkish communication from the BOC at the meeting along with a rate cut.

- Retail sales on Thursday is the final major piece of data before the decision, with August GDP only out on Oct 31.

- In alphabetical order of institution, each of which as noted expects an October cut with BMO being the exception:

- BMO (hold in October): "Suffice it to say this will make the Bank of Canada's decision a bit more interesting next week than previously expected—markets had been all but baking in a rate cut after Governor Macklem's dovish remarks and yesterday's soft Business Outlook Survey. Absolutely full disclosure: We have been on the dovish side of the ledger, calling for the Bank to eventually cut the overnight rate to 2.0% (and possibly lower if trade gets uglier), but were not convinced that October would see another cut. Given today's setback for core, we'll stay there for now. The biggest counterpoint, as noted above, is that some key measures of core are still fully consistent with the Bank's view that underlying inflation is around 2.5%."

- CIBC: "We think that core measures of inflation were just about subdued enough, and the economy is certainly weak enough, to still justify a further 25bp cut from the Bank of Canada next week. However, after that the Bank is likely to move back onto the sidelines, in part due to evidence of some lingering inflationary pressures, but also on the assumptions that economic growth starts to recover and progress is made towards a trade deal that reduces some of the sector specific tariffs currently impacting Canadian trade."