EQUITIES: Latest Estoxx Options

Dec-06 09:44

- SX5E (21st Juned) 4400^ traded 371.4 in 10k.

- SX5E (20/12/24) 4400/3700ps 1x2, bought for 69 in 10k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: SFRU4 Blocked

Nov-06 09:35

Latest block trade lodged at 09:09:58 London/04:09:58 NY:

- SFRU4 8,000 lots blocked at 95.330, looks like a buyer.

US TSYS: Curve Flatter, Outrights Operating Just Off Early Yield Highs

Nov-06 09:23

The raft of peripheral/final core Eurozone services and composite PMIS do little for Tsys, as the space stabilises over the last hour or so.

- That leaves TYZ3 -0-08 at 108-03+, 0-01 off the base of a narrow 0-05 range.

- Cash Tsy yields are little changed to 3.5bp higher across the curve, with bear flattening seen.

- Macro headline flow has been light outside of the aforementioned PMI run out of Europe.

- FOMC-dated OIS prices a modest ~4bp of additional tightening through the January ‘24 meeting, as the move away from Friday’s post-data dovish extremes extends a little. Further out, ~32bp of cuts are seen through June ’24 (vs. current effective levels) i.e. a 25bp cut is more than fully priced over that window.

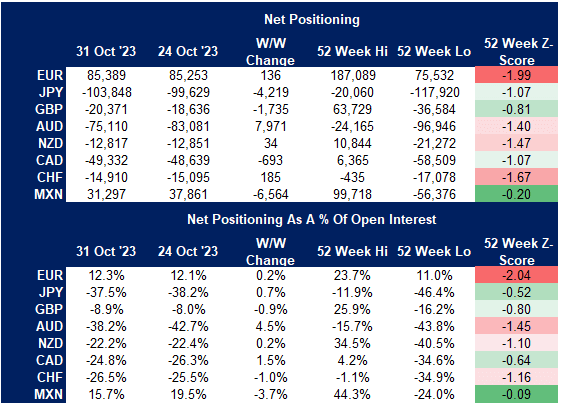

CFTC: CoT Data Shows AUD Position Improved Alongside Higher Q3 CPI

Nov-06 09:12

- Friday's CFTC CoT update showed markets most notably trimming the AUD net short, while moderating net long MXN.

- The AUD net position recovered off levels not far off the lowest in a year, as markets added a net 8.0k contracts, or 4.5% of open interest. With the data is correct as of the Tuesday Oct31 close, the more favourable positioning may reflect the recovery in spot after the higher-than-expected CPI print for Q3. The RBA are this week expected to hike rates a further 25bps to 4.35%.

- USD Index positioning held close to multi-month highs, fading very slightly off last week's net long of 19.6k contracts - the largest net long since December last year. This leaves markets with the most sizeable net long in USD and EUR, while speculators maintain the largest net shorts in JPY and AUD. Full details here: