US TSYS: Late SOFR/Treasury Option Roundup: Pre-Data/Event Risk Positioning

Mostly downside put flow from SOFR & Treasury options - with a notable exception: huge buyer short Sep'26 SOFR calls outlined below. Focus is on tomorrow's headline employment data for December and the SCOTUS opinion session (est 1000ET) on the Trump admin's global tariff actions. Underlying futures reverse early overnight gains - remain near recent session lows, curves mixed (2s10s +1.683 at 69.274; 5s30s -.753 at 111.928). Projected rate cut pricing has consolidated vs. late Wednesday levels (*): Jan'26 at -2.9bp (-4bp), Mar'26 at -11.2bp (-12.9bp), Apr'26 at -16.4bp (-18bp), Jun'26 at -30.3bp (-33bp).

- SOFR Options:

- over +125,000 0QU6 97.50 calls, 7.5 vs. 96.80/0.17%

- +20,000 SFRU6 96.12/96.37 put spds, 1.75

- +7,500 SFRZ6 96.87/97.37/98.50 2x3x1 call flys, 17.5-18.0 ref 96.88

- +10,000 0QZ 97.50 calls, 8.5 ref 96.73/0.16%

- -30,000 SFRM6 97.62 calls, 2.0 vs. 96.635/0.10%

- +7,500 SFRG6 96.43/96.50/96.62 2x3x1 broken call flys, 1.5 ref 96.44

- +10,000 SFRH6 96.43 put vs. 0QH6 x2 96.50 put, 3.75 net

- +27,000 (pit/screen) 0QF6 96.62/96.75 put spds, 1.5 ref 96.86

- -2,000 3QG6 96.50 straddles, 19.5 ref 96.45

- +38,000 SFRH6 96.31/96.37/96.43 put trees, 3.75

- Block, -5,000 SFRG6 96.31/96.87 strangles, 1.0, more in pit

- 1,500 SFRU6 96.87/97.25/97.37 broken call trees ref 96.82

- 2,000 SFRZ6 96.62/96.87 put spds ref 96.88

- over 11,000 0QG6 96.62 puts outright pushes volume up to 36.5k

- 25,000 0QG6 96.62/96.75 put spds ref 96.90 to -.905

- 1,500 SFRZ6 96.50/96.75 put spds vs 0QZ6 96.25/96.37/96.75 broken put flys

- 3,000 0QG6 96.87 puts ref 96.885

- 2,000 2QH6 96.12/96.37 put spds ref 96.715

- 1,750 SFRZ6 96.37/97.00/97.37 broken put flys ref 96.90

- Treasury Options:

- 4,000 TYG6 111/TYK6 110.5 put spread

- 2,500 TYK6 114 calls

- 4,000 FVG6 108 puts ref 109-05

- 8,000 TYG6 111.75/112.25 put spds, 12 ref 112-13

- 2,000 FVG6 109.25/109.5 call spds ref 109-08.25

- 1,115 USH6 112/114/115 1x3x2 put flys ref 115-22

- 1,800 wk2 TY 112 puts, 2 ref 112-15

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

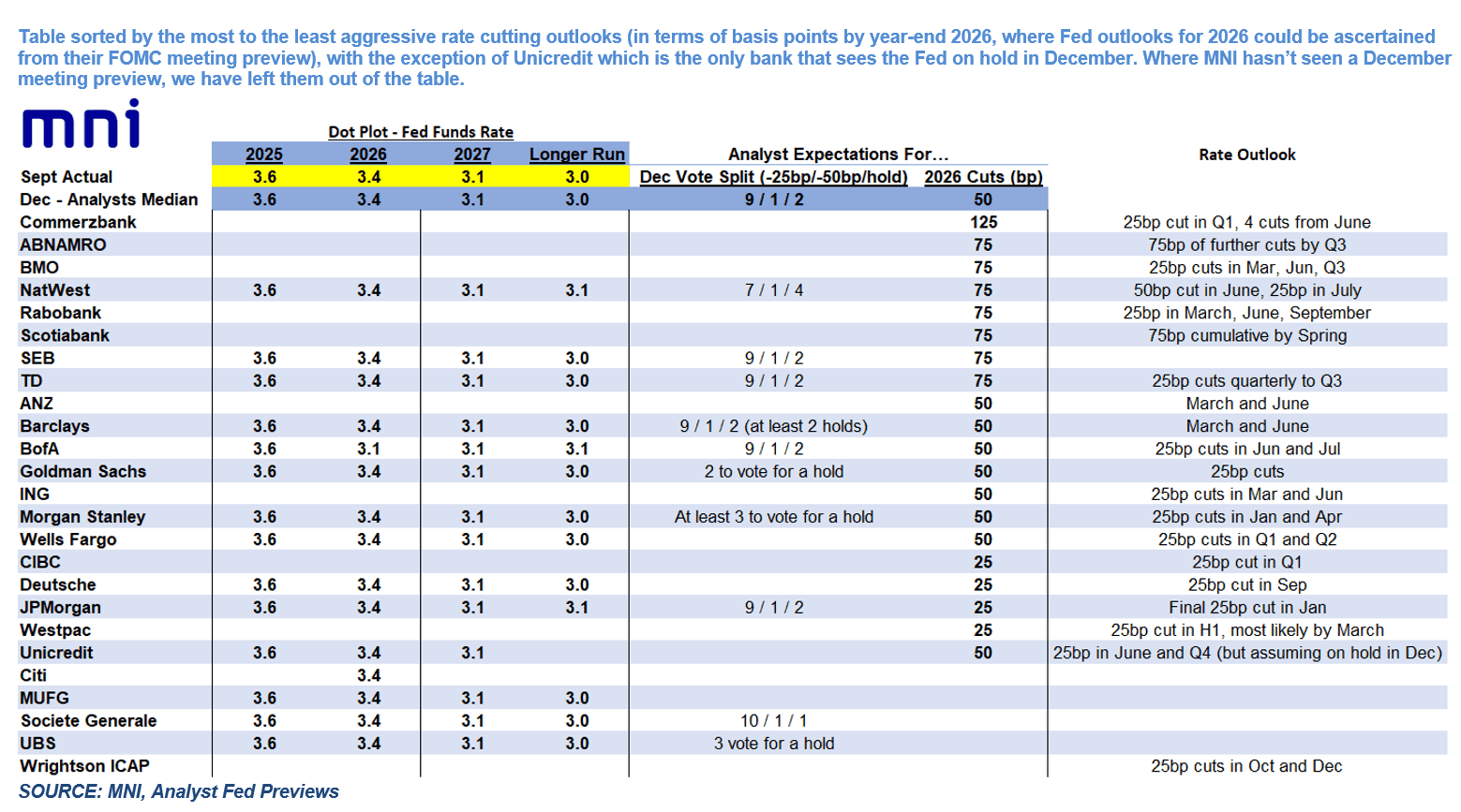

FED: Analyst Outlook: 2026 Cuts Seen Between 25bp And 125bp (2/2)

From our Fed preview's summary of analyst expectations:

- SEP/Dot Plot: The vast majority of analysts expect unchanged Fed funds rate dot medians in the updated SEP vs the prior edition in September, implying 1 cut in 2026 and another in 2027. Some see the longer-run dot rising to 3.1% from 3.0%.

- Statement: Almost all analysts expect a shift in the forward rate guidance, to reflect less propensity to cut in 2026.

- Opinions vary on the vote split, ranging from 10 in favor of a 25bp cut with 2 dissenters, to 7 in favor of a 25bp cut with 5 dissenters. None expects a unanimous vote.

- Future action: Analysts’ views of total cuts in 2026 range from 25bp to 125bp, with a median of 50bp. Notably, several analysts expect rate cuts to resume only in the 2nd half after Chair Powell’s successor is in place.

FED: Analyst Outlook: Near Unanimity On Rate Cut (1/2)

All but one of the 33 analysts’ previews of the December meeting anticipates a 25bp rate cut (Unicredit is the exception), with the vast majority seeing a “hawkish cut” in terms of the communications. We go through analysts' key comments in our Fed preview - see table below for consensus on the Dot Plot and the vote split, as well as the rate outlook.

US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Stabilization Elsewhere

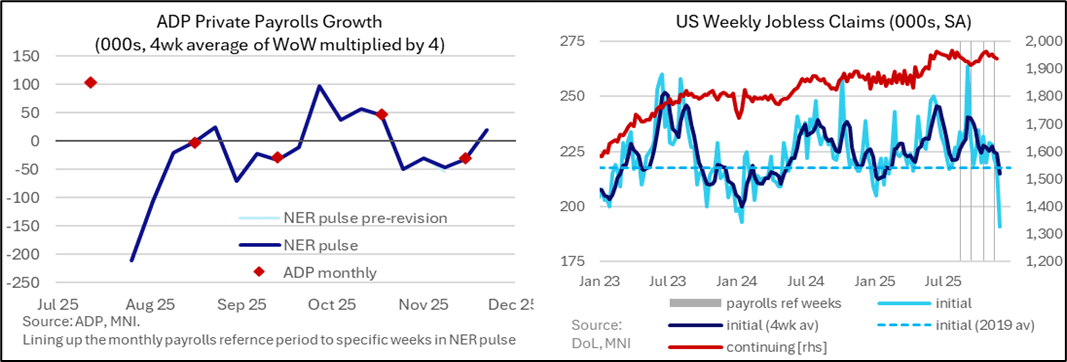

- Since the delayed September payrolls report, ADP employment has sent mixed signals – it surprisingly firmed in October after declining in September, returned to declining with a -32k drop in the main November report for a third monthly decline in the space of four months before some stabilization in latest weekly data.

- However, some unemployment rate trackers such as the Chicago Fed’s nowcast point to no further deterioration in the labor market ahead, with this nowcast tracking at the same 4.44% in November after 4.46% in October.

- Granted, the surprise increase in the BLS unemployment rate in September has clearly appeared sufficient to sway Williams and seemingly other core FOMC members to the need for another cut in what might be viewed as a further insurance cut.

- Certainly, hawks will point to weekly jobless claims data not showing any additional deterioration in the labor market, with initial claims at very low levels even when looking through the latest slide to its lowest in three years in what looks like a Thanksgiving adjustment distortion. Granted, re-hiring conditions are softer as evidenced by continuing claims but they roughly remain at levels seen in payrolls reference periods from earlier in the year.

- In an addition to what we wrote in the Fed preview, the double JOLTS report for September and October on day one of the two-day FOMC meeting saw much higher than expected job openings but with quit and hire rates casting a more dovish light. Higher frequency Indeed job openings data had suggested stabilization before a recent increase into November.