US TSYS: Late Roundup: Tsys Hold Midrange, Focus on July Employ Next Friday

Jul-28 19:25

- Treasury futures remain in positive territory, off early session highs following a knee-jerk bid on lower than est Employment Cost Index gains 1.0% vs. 1.1% est, Core PCE 4.1% vs. 4.1% est.

- Rates quickly reversed the gap move as markets deemed it an overreaction to near in-line data. Services saw a mild acceleration from 0.25% to 0.275% M/M but importantly the Fed’s preferred indicator of core non-housing services eased a tenth to 0.22% M/M. Softer ECI data an afterthought while benign price pressure evinced from UofM survey helped buoy rates back to middle of the range.

- Tsy curves off early highs, currently mixed w/ 3M10Y -2.594 at -146.816, 2s10s +.600 at -92.849 (vs. -86.190 high) as short end rates lagged the rally in intermediates. As such, rate hike projections through year end remained subdued (18-36% chance of 25bp hike before year end). Markets much more eager to price in rate CUTS in 2024 (first 25bp cut in May '24, second in July'24.

- Focus turns to next week's ISMs on Tue (Mfg 46.98 est, prices paid 44.0 est), ADP on Wednesday (+188k est vs. 497k prior), and July employment data next Friday, current estimate of +200k job gains vs. +209k in June.

- Equity earnings resume Monday, premarket: Immunogen; after the close: Diamondback Energy, Tenet Health, Monolithic Power, Welltower, Rambus, and Western Digital.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Bonds Near Late Session Highs, Tsy 7Y Note Sale Well Received

Jun-28 19:00

- Treasury futures are drifting near late session highs, climbing steadily since marking lows at midmorning, discounting earlier comment from Chairman Powell at ECB CB forum that consecutive rate hikes are not off the table spurred fast sell interest in short to intermediates.

- Modest two-way trade this morning after higher than expected Retail inventories data: MoM (0.8%, 0.2% est; 0.3% prior/rev), Wholesale Inventories in-line MoM (-0.1%, -0.1% est; -0.3% prior/rev), Advance Goods Trade Balance (-$91.1B, -$93.8B est; -$97.1B prior).

- Curves climbed off deeper inversion briefly after a decent $35B 7Y note auction (91282CHJ3) traded through: 3.839% high yield vs. 3.847% WI; 2.65x bid-to-cover vs. 2.61x last month. Indirect take-up 75.31% vs. 72.30% prior; Direct take-up: 16.55% vs. 17.29% prior; Primary dealer take-up to 8.14% vs. 10.42% prior auction.

- Despite the bounce, bears still hold sway at current levels. Recent pullback in 10s held inside the recent range and the contract remains in consolidation mode. The trend outlook is bearish.

- Meanwhile, market confidence of a hike at the July 26 FOMC has climbed to 79% with implied rate of +19.8bp to 5.267%. September cumulative of +24.4bp at 5.315% while November is pricing in just over a 25bp hike with cumulative at 29.3bp at 5.364%. Fed terminal at 5.385% in Nov'23 this morning.

EURJPY TECHS: Bull Trend Extends

Jun-28 19:00

- RES 4: 159.92 2.236 proj of the May 11 - 29 - 31 price swing

- RES 3: 158.72 2.00 proj of the May 11 - 29 - 31 price swing

- RES 2: 158.49 2.0% 10-dma envelope

- RES 1: 158.00 High Jun 28

- PRICE: 157.53 @ 16:05 BST Jun 28

- SUP 1: 155.06/154.05 Low Jun 23 / 20 and key short-term support

- SUP 2: 153.54 20-day EMA

- SUP 3: 151.61 Low Jun 15

- SUP 4: 150.65 50-day EMA

EURJPY bulls remain in the driver’s seat. The uptrend extended marginally on Wednesday to put the cross at a fresh multi-month high. Tuesday’s price action reinforces the current bullish theme after the latest impulsive rally. Moving average studies are in a bull mode position too, highlighting positive market sentiment. The focus is on 158.72, a Fibonacci projection. Initial key support is at 155.06, the Jun 23 low.

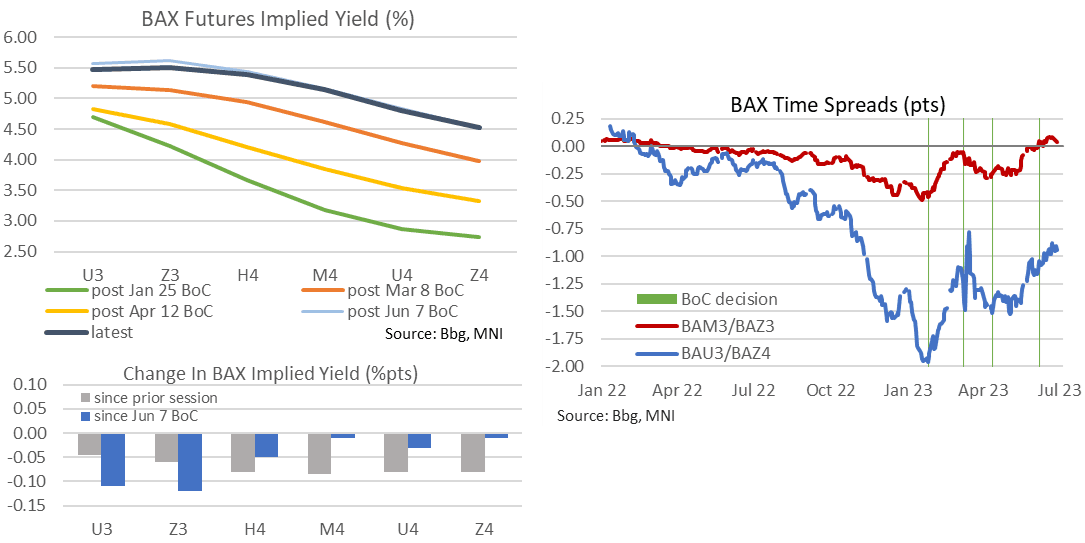

CANADA: Backloaded Rally In CAD Rates

Jun-28 18:56

- 10s may be leading the GoC rally on the day but the front end has still seen a decent -6bp decline.

- The latter’s dynamics are supported in rates markets, with BAX futures rallying 4 ticks for the front Sep’23, 6 ticks for the Dec’24 and building to 8.5 ticks through mid-2024.

- The upshot is that implied yields for 2H23 are now ~10bps lower than after the BoC Jun 7 hike (i.e. unwinding half of the then sell-off) and marginally lower for all 2024 contracts as well. The BAU3/Z4 spread widens back to -95bps although remains tight relative to recent months.

- In the near-term, OIS rates imply a 15-16bp hike for the Jul 12 decision, down from 17bp pre CPI, but still with the BoC surveys and monthly GDP this Fri before the employment report the following Fri.