LATAM FX: Price Signal Summary - USDMXN Bounce Extends

Aug-22 12:54

- A bullish theme in USDMXN remains intact following the rally between Jul 12 and Aug 5. The pair is trading higher this week and this also represents a positive development. Initial short-term objectives are 19.5999 and 19.8362, the 61.8% and 76.4% retracement points of the sell-off between Aug 5 - Aug 16. Further out, a clear break of the 20.00 handle would pave the way for an extension towards 20.7642, the 76.4% retracement of the bear leg between Nov ‘21 and Apr this year. Support to watch lies at the 50-day EMA, at 18.4169. A clear break of the 50-day average would undermine the bullish theme. Initial support is at the 20-day EMA, at 18.8028.

- Bullish conditions in USDBRL remain intact and the latest pullback is considered corrective. However, support around the 50-day EMA, has been breached. A clear break of this average would undermine a bull theme and signal potential for a deeper retracement towards 5.3709, the Jul 11 low and the next important support. A reversal higher would signal the end of the correction and refocus attention on key resistance and the bull trigger at 5.8551, the Aug 5 high. Initial firm resistance is 5.5261, the 20-day EMA, ahead of 4.6545, the Aug 8 high.

- USDCLP has pulled back from its Aug 5 high of 966.61. The move - for now - appears to be a correction. However, price has traded through a key support at 929.78, the Aug 1 low. The breach highlights potential for a deeper retracement towards 902.00, the Jul 11 low. For bulls, a reversal higher would refocus attention on key resistance and the bull trigger at 966.61, the Aug 5 high. Initial firm resistance is 940.53, the Aug 16 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: United Health 8Pt Jumbo Guidance Update

Jul-23 12:53

- Date $MM Issuer (Priced *, Launch #)

- 7/23 $Benchmark United Health 8Pt jumbo: 2Y +60a, 2Y FRN, 5Y +85a, 7Y +100a, 10Y +110a, 20Y +120a, 30Y +135a, 40Y +150a

PIPELINE: United Health Group 8Pt Jumbo on Tap

Jul-23 12:46

- Date $MM Issuer (Priced *, Launch #)

- 7/23 $Benchmark United Health 8Pt jumbo: awaiting details.

- Past historical issuance from UNH usually around $6B over 4-6 tranches while Oct'22 saw $9B over 7 tranches:

- Mar'24: $6B *United Health $500M 3Y +37, $400M 5Y +52, $1B 7Y +70, $1.25B 10Y +80, $1.75B 30Y +95, $1.1B 40Y +107

- Mar'23: $6.5B *United Health $1.25B +5Y +88, $1.5B 10Y +118, $2B 30Y +143, $1.75B 40Y +158

- Oct'22: $9B *United Health $500M 2Y +55, $750M 3Y +70, $1B +5Y +100, $1.25B +7Y +115, $2B +10Y +130, $2B +30Y +165, $1.5B +40Y +185

- May'22: $6B *United Health $600M 5Y +75, $900M 7Y +105, $1.5B 10Y +125, $2B 30Y +160, $1B 40Y +180

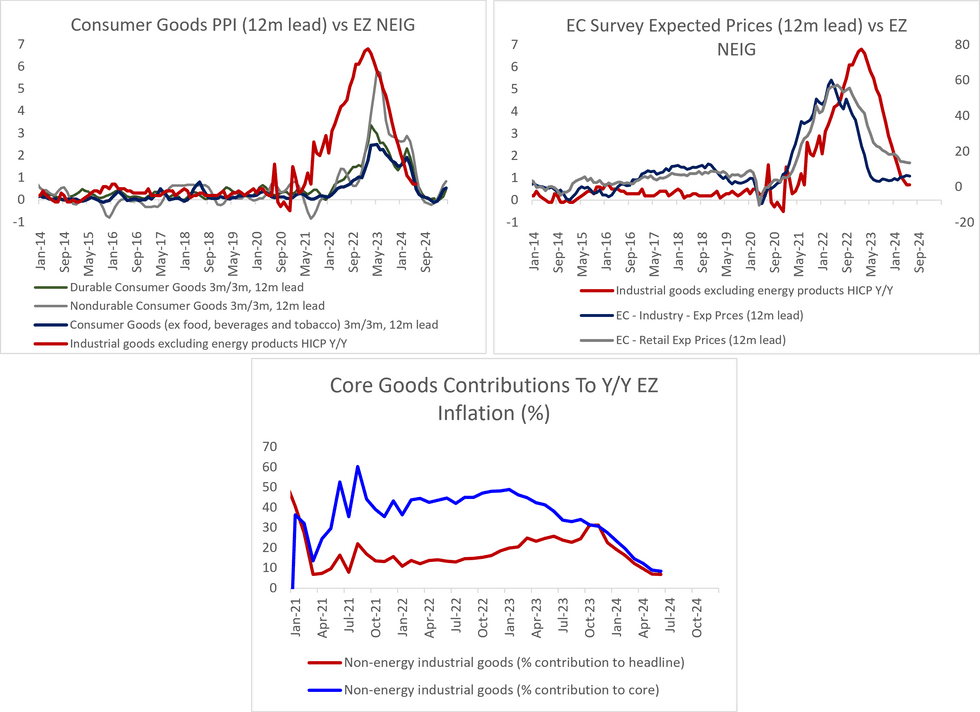

EUROZONE DATA: ECB Not Currently Concerned About Core Goods Re-acceleration (2/2)

Jul-23 12:43

The July ECB meeting once again highlighted domestic price pressures (largely services) as the key source of upside risks to the inflation outlook.

- The (small) upward revisions to 2024/2025 Eurozone headline and core inflation forecasts in the June projection round included “only negligible impacts from geopolitical tensions in the Middle East (including disruption to Red Sea shipping) on goods inflation, consistent with shipping costs being a small share of total goods costs”.

- However, should core goods disinflation eventually stall and potentially start re-accelerating, the magnitude of disinflation required in other components (i.e. services) to achieve the 2% target increases.

- If services inflation remains sticky around 4% Y/Y and core goods inflation begins to re-accelerate in the coming months, this may pressure the ECB to make further upward inflation revisions in future projection rounds.

- This may also put upward pressure on EUR inflation swaps, which currently trade below the 2% target at 1- and 2-year ahead horizons.