EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.74% +2bp

10yr UST 4.14% +3bp

5s-10s UST 40.3 +0bp

WTI Crude 61.4 -1.1

Gold 3979 -63.4

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1132bp -174bp

BRAZIL 6 1/8 03/15/34 235bp +7bp

BRAZIL 7 1/8 05/13/54 318bp +9bp

COLOM 8 11/14/35 320bp +5bp

COLOM 8 3/8 11/07/54 381bp +3bp

ELSALV 7.65 06/15/35 376bp -1bp

MEX 6 7/8 05/13/37 217bp +3bp

MEX 7 3/8 05/13/55 265bp +3bp

CHILE 5.65 01/13/37 131bp +2bp

PANAMA 6.4 02/14/35 231bp +2bp

CSNABZ 5 7/8 04/08/32 613bp +64bp

MRFGBZ 3.95 01/29/31 260bp +13bp

PEMEX 7.69 01/23/50 472bp +5bp

CDEL 6.33 01/13/35 180bp +0bp

SUZANO 3 1/8 01/15/32 163bp +2bp

FX Level Δ DoD

USDBRL 5.38 +0.03

USDCLP 950.76 -0.24

USDMXN 18.4 +0.05

USDCOP 3886.27 -7.18

USDPEN 3.43 -0.02

CDS Level Δ DoD

Mexico 89 2

Brazil 143 6

Colombia 194 3

Chile 53 1

CDX EM 97.82 (0.05)

CDX EM IG 101.48 (0.03)

CDX EM HY 93.49 (0.05)

Main stories recap:

· Major US equity indexes eased back off of record highs to close lower while Treasuries inched up another couple of bp as the U.S. auctioned off USD22bn of long bonds.

· EM primary issuance remained active with two new CEEMEA deals and three new issues in LATAM.

· Secondary market benchmark bond spreads were mixed in CEEMEA while in LATAM they were mostly wider.

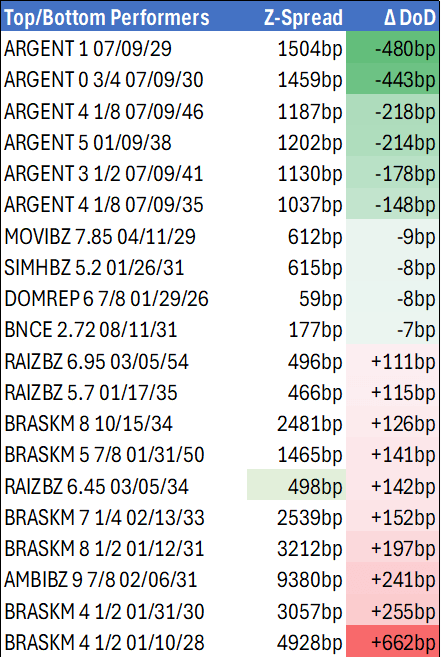

· Fallout from Braskem and Ambipar credit events continued with several Brazil high yield corporate names widening. Earnings performance challenged and over levered Raizen was severely impacted with some bonds down as much as 10 points.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US INFLATION: MNI US CPI Preview: Data To Shape Fed's Tone On Rate Cuts

We've just published our inflation preview for this week's CPI and PPI data - Download Full Report Here

- August inflation data lands this week, with PPI out first on Wednesday September 10 at 0830ET, followed 24 hours later by the CPI report. Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July, with the MNI unrounded median looking for 0.32% with a slight lean in the risks toward a rounding-up to 0.4%.

- For PPI, current Bloomberg consensus is for a cooling after July’s hot print, with M/M final demand PPI at 0.3% (0.9% prior) and “core” (ex-food/energy/trade) also at 0.3% (0.6% prior).

USDCAD TECHS: Trading Above Support

- RES 4: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 3: 1.3925 High Aug 22 and the bull trigger

- RES 2: 1.3868 High Aug 26

- RES 1: 1.3854 High Sep 05

- PRICE: 1.3838 @ 17:43 BST Sep 9

- SUP 1: 1.3727 Low Aug 27 and a bear trigger

- SUP 2: 1.3709 61.8% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 3: 1.3658 76.4% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact. Near term, the recovery from the Aug 29 low highlights a potential early reversal signal and if correct, the end of the corrective pullback between Aug 22 - 29. An extension higher would open the bull trigger at 1.3925, the Aug 22 high. Support lies at 1.3727, the Aug 29 low. Clearance of this level would instead reinstate a short-term bear theme and expose 1.3709 initially, a Fibonacci retracement.

US TSYS: Eyes on PPI, Cash 2s10s Remains Dis-Inverted, 3Y Stops Through

- Treasuries look to finish weaker, off late morning lows with rates paring losses after a decent $58B 3Y Note auction broke a four consecutive auction run of tails w/ 3.485% high yield vs. 3.492% WI; 2.73x bid-to-cover vs. 2.53x prior.

- After some sharp two-way action - Tsys retreated after BLS Prelim Benchmark Revision to Establishment Survey Data comes out much lower than anticipated: -911k vs. -682k est from -818k prior.

- Meanwhile, Johnson Redbook Retail Sales Index rose 6.6% Y/Y in the first week of September (ending Sep 6), running a little above retailers' targeted 6.3% gain for the month.

- Currently, the Dec'25 10Y trades -6.5 at 113-11 (yld 4.0722 +.0324) vs. 113-07 low -- Initial firm support to watch is 112-11+, the 20-day EMA. Yield curves flatter: 2s10s -2.311 at 52.831, 5s30s -1.536 at 114.416. Cash 2s10s adjusted for carry/rolldown remains dis-inverted 58.9.

- US$ off lows, BBG index BBDXY currently +2.6 at 1201.15 vs. 1196.68 post data low.

- Focus turns to US price data, as PPI and CPI releases are expected across Wednesday and Thursday respectively. China CPI and PPI figures will be released during APAC hours tomorrow.