EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.71% +4bp

10yr UST 4.12% +4bp

5s-10s UST 40.4 -1bp

WTI Crude 60.8 +0.4

Gold 3888 +31.4

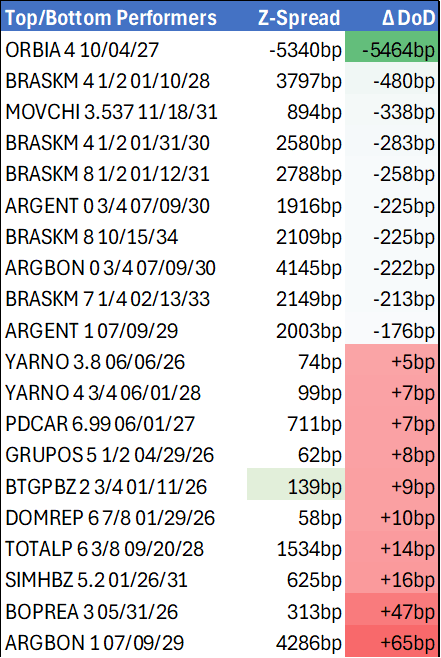

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1346bp -80bp

BRAZIL 6 1/8 03/15/34 226bp +1bp

BRAZIL 7 1/8 05/13/54 309bp -2bp

COLOM 8 11/14/35 321bp -7bp

COLOM 8 3/8 11/07/54 387bp -4bp

ELSALV 7.65 06/15/35 381bp -6bp

MEX 6 7/8 05/13/37 213bp -5bp

MEX 7 3/8 05/13/55 262bp -4bp

CHILE 5.65 01/13/37 129bp -3bp

PANAMA 6.4 02/14/35 229bp -1bp

CSNABZ 5 7/8 04/08/32 532bp -5bp

MRFGBZ 3.95 01/29/31 240bp -3bp

PEMEX 7.69 01/23/50 464bp -8bp

CDEL 6.33 01/13/35 179bp -4bp

SUZANO 3 1/8 01/15/32 159bp -3bp

FX Level Δ DoD

USDBRL 5.33 -0.01

USDCLP 965.32 +3.45

USDMXN 18.4 -0.03

USDCOP 3869.35 -16.54

USDPEN 3.46 -0.01

CDS Level Δ DoD

Mexico 88 (1)

Brazil 135 (1)

Colombia 193 (2)

Chile 51 (1)

CDX EM 97.90 0.07

CDX EM IG 101.53 0.05

CDX EM HY 93.63 0.16

Main stories recap:

· Treasury yields moved about 4bp higher today, retreating from gains made in previous days, but still lower for the week as the market debated the impact of the U.S. govt. shutdown.

· The EM primary market was relatively quiet, though there were a couple of mandates pending in CEEMEA and two pending for LATAM. That bodes well for the new issue market next week.

· Argentina sovereign bonds rebounded about two points amid further talk about U.S. govt. support.

· Braskem bonds rebounded about three points on further reports that banks may seize Braskem stock that it is holding as collateral for defaulted loans.

· Telefonica Moviles Chile bonds gapped 11 points higher at the open after late yesterday news of a joint America Movil, Entel bid for the beleaguered Chile telecom provider.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

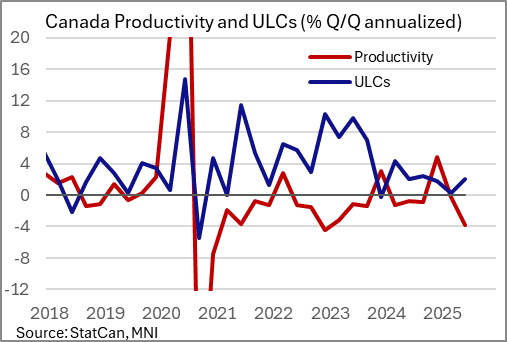

CANADA DATA: Productivity Remains A Problem

Productivity fell sharply in Q2 per StatCan's estimates, declining 1.0% Q/Q SA (more than the expected 0.2% drop). That was the 5th decline in the last 6 quarters, and the biggest drop since Q4 2022.

- This came as hours worked slowed to 0.3% growth after 0.6% in Q1. Hourly compensation fell for the first time since Q1 2021 (-0.5%), but combined with the productivity drop, this meant a 0.5% increase in unit labor costs.

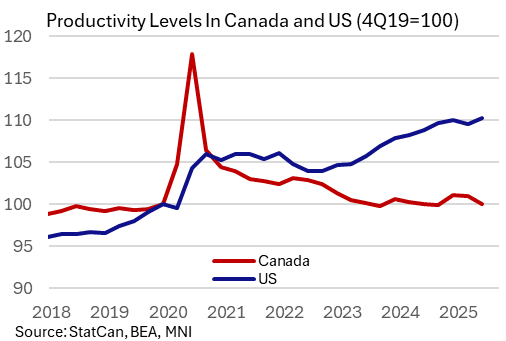

- While the level of productivity is is not at a recent low (that was September when the index was at its lowest since September 2019), it means that overall productivity has only increased by around 1% in the 22 quarters since 2019. At the same time, wage growth has meant Unit Labor Costs are up over 26% in the same period, a new high.

- The inevitable comparison is with the US, where productivity is up 10% since 2019, with ULCs up a more modest 19%.

- The latest StatCan report notes "Overall, manufacturing and wholesale trade were the main contributors to the decrease in business sector productivity in the second quarter. These two sectors—which are heavily dependent on merchandise trade—were particularly affected by the uncertainty surrounding Canada's trade activities with the United States during the quarter."

- While ULC growth has moderated vs 2022-23, and it must be said that the quarterly figures are subject to large revisions, a continued pickup alongside weaker productivity would be inflationary.

- The July BOC deliberations noted "wage increases and unit labour costs had continued to ease" in its discussion of inflation, also noting that easing ULCs and excess supply could counterbalance upward pressures from tariffs on consumer prices).

- The Bank of Canada's growth outlook under its "current tariff" scenario in the July MPR cites weaker potential output through 2026 "because tariffs and uncertainty lead to lower trend labour productivity" though potential output is seen picking up again thereafter due to "more robust trend labour productivity growth".

USDCAD TECHS: Recovers From Its Recent Lows

- RES 4: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 3: 1.3925 High Aug 22 and the bull trigger

- RES 2: 1.3868 High Aug 26

- RES 1: 1.3815 High Sep 02

- PRICE: 1.3797 @ 16:47 BST Sep 3

- SUP 1: 1.3722 Low Aug 7 and a pivot support

- SUP 2: 1.3709 61.8% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 3: 1.3658 76.4% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 4: 1.3637 Low Jul 25

The bull cycle in USDCAD that started mid-June remains in play. However, the latest corrective pullback has resulted in a breach through support at the 50-day EMA, at 1.3775. A clear break of this handle signals scope for a deeper retracement and exposes 1.3722, the Aug 7 low. Near term, the recovery from the Aug 29 low also highlights a potential early reversal signal. A continuation higher would open the bull trigger at 1.3925, the Aug 22 high.

US OUTLOOK/OPINION: U/E Rate In Increasing Focus, FOMC Eyeing Trend Rise [2/2]

Cleveland Fed’s Hammack (’26 voter) is of a similar view to us, although actually puts even more weight on the unemployment rate. Speaking last month:

- "With the changes that have happened in immigration policy, it's not clear that that headline [payrolls] growth number is going to be as informative as things like the unemployment rate, the vacancies to unemployed ratio, other things that we're looking at on the employment side of the mandate, and that's because we've seen a massive shift.

- So yes labor demand may be coming down but labor supply has come down pretty dramatically as well. And so our goal of maintaining employment around maximum needs to look at both sides of that, and it could be that even though we're seeing much slower headline job growth numbers, it could be that the labor market is still in balance and so we'll need to look at the closely."

That’s a similar message to Fed Chair Powell from his Jackson Hole address on Aug 22, although he cast it in a more dovish light considering rising downside risks to employment and the potential for a quick deterioration:

- “The July employment report released earlier this month showed that payroll job growth slowed to an average pace of only 35,000 per month over the past three months, down from 168,000 per month during 2024 (figure 2). This slowdown is much larger than assessed just a month ago, as the earlier figures for May and June were revised down substantially. But it does not appear that the slowdown in job growth has opened up a large margin of slack in the labor market—an outcome we want to avoid.

- The unemployment rate, while edging up in July, stands at a historically low level of 4.2 percent and has been broadly stable over the past year. Other indicators of labor market conditions are also little changed or have softened only modestly, including quits, layoffs, the ratio of vacancies to unemployment, and nominal wage growth.

- Labor supply has softened in line with demand, sharply lowering the "breakeven" rate of job creation needed to hold the unemployment rate constant. Indeed, labor force growth has slowed considerably this year with the sharp falloff in immigration, and the labor force participation rate has edged down in recent months.

- Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”