EM ASIA CREDIT: MNI EM Credit Market Update - Asia

A relatively quiet end to the week in Asia, with China and Korea out for national holidays, and not back until next Thursday (Oct 9th) and Friday (Oct 10th) respectively. Asia EM USD sovereign and agency spreads are more or less unchanged this morning. In terms of newsflow, LG Energy announced it was sending employees back to the US, now that visa issues are resolved, and Malaysian sovereign wealth fund, Khazanah Capital, denied reports it was in talks with China on a rare earth project. No new issuance reported today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Back End Yields Notably Higher, 2/10s Curve At +148bps

NZGB yields are flat to 6bps higher, led by the back end of the curve. The steepening theme evident globally has been seen strongly today in NZGB markets. The 2yr yield is barely changed and anchored sub 3.0% at this stage. The 10yr yield is up close to 6bps, last at 4.46% and closing the gap with pre RBNZ highs from August close to 4.50%. These moves leave the NZGB 2/10s curve at +148bps, closing in on April highs near +154bps.

- US Tsy futures initially moved higher in Wednesday Asia Pac trade, but this move has been faded. Cash Tsy yields sit 1-2bps higher in yield terms, with the back end leading. The US 2/10s curve sits at +63bps.

- Outside of US moves, NZ markets have also likely been impacted by ACGB yield gains. These were supported post the better than expected Q2 GDP print (although ACGB front end yields are notably higher, up 9bps for the 2-3yr tenors, compared to NZ's flat 2yr trend today).

- NZ's 2yr swap rate has edged a little higher, last near 2.775%.

- On the news front: " S&P Global Ratings is “comfortable” with New Zealand’s sovereign rating outlook, though it’s closely watching the nation’s current account and budget deficits." (via BBG).

- Data wise, the ANZ August commodity price index rose 0.7%m/m, after a -1.8% fall in July. Overnight we did have a softer whole milk powder auction result though.

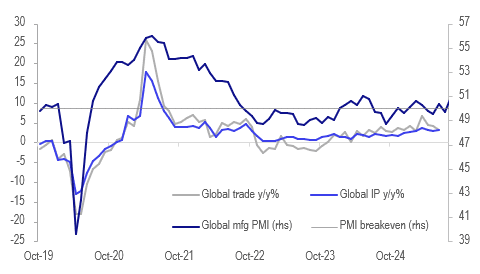

GLOBAL MACRO: Indicators Suggest Global IP Growth Continued In Q3

The August JP Morgan global manufacturing PMI printed at 50.9 up from 49.7 signalling growth in activity in the sector again and at its fastest since May 2024. The pickup was driven particularly by higher output but also domestic orders and a return to hiring but confidence remained below average. The PMI, LME metal prices and the Baltic Freight Index (BFI) are all consistent with global IP and trade growth remaining at current rates or possibly improving.

Global growth

Source: MNI - Market News/LSEG/Bloomberg Finance L.P.

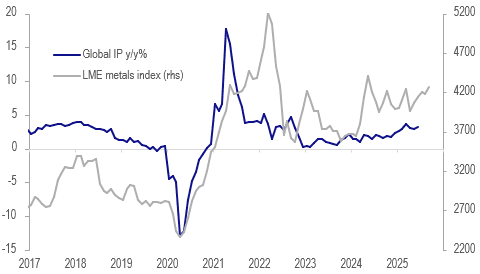

- CPB global IP growth rose 0.4% m/m in June driving a 0.4pp improvement in annual growth to 3.2% y/y, the strongest since March which was boosted by the frontloading of deliveries to the US ahead of tariff deadlines. June global trade rose 3% y/y down from 4.1% y/y.

Global IP y/y% vs LME metals

- August output in the JP Morgan PMI rose to 51.7 from 49.7 helped by orders up 1.1 points to 50.9. All sectors saw growth. However the increase was driven by domestic demand and export orders continued to contract but at a slower rate but tariff worries remained a problem, according to JP Morgan.

- The increase in demand likely drove an improvement in employment with it marginally returning to growth territory at 50.2.

- The resumption of output growth in manufacturing was also across most countries with only 5 continuing to see contraction. India, Thailand, Spain and the US saw strong growth.

- Cost inflation rose to its highest rate since February driving a marginal pickup in selling price inflation with the US reporting the fastest rate.

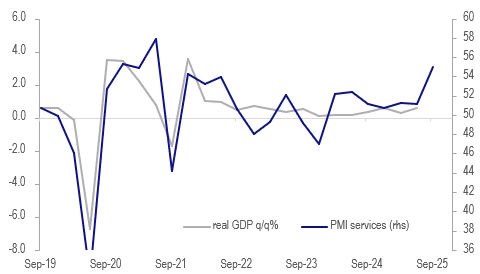

AUSTRALIA DATA: Q2 Boosted By Special Factors, H1 Averaged 0.4% q/q

Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook.

- The S&P Global PMI improvement over Q3 suggests growth may have improved further at the start of H2. The August composite rose to its highest since February 2022.

Australia GDP q/q% vs S&P Global PMI services

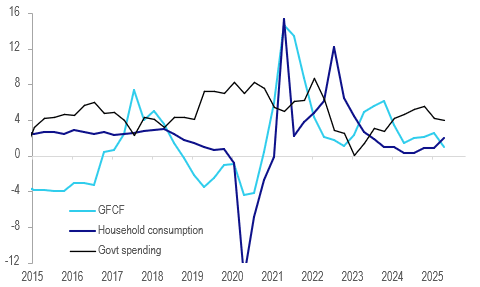

- Household consumption contributed 0.45pp to GDP as it rose 0.9% q/q to be up 2% y/y, the highest in 2 years, which was supported by a 1pp fall in the savings rate to 4.2%. Nominal disposable income rose 0.6% q/q.

- The ABS notes that the close proximity of Anzac Day to Easter boosted holiday-related spending. Also end of financial year discounting encouraged discretionary spending which rose 1.4% q/q.

- Government spending contributed 0.2pp to growth as it increased 1.0% q/q to be up 4% y/y driven by a strong increase in benefits paid and health expenditure as well as election and defence spending.

- Investment was lacklustre across the board with it detracting 0.2pp driven by the public sector with private capex neutral.

- Net exports made its strongest contribution to GDP in two years. Exports rose 1.7% q/q to be up 1.5% y/y, while imports increased 1.4% q/q & 1.9% y/y, a sign of improving domestic demand.

- GDP/person rose 0.2% q/q to be up 0.2% y/y, the first annual rise since Q1 2023.

Australia domestic demand y/y%

Source: MNI - Market News/ABS