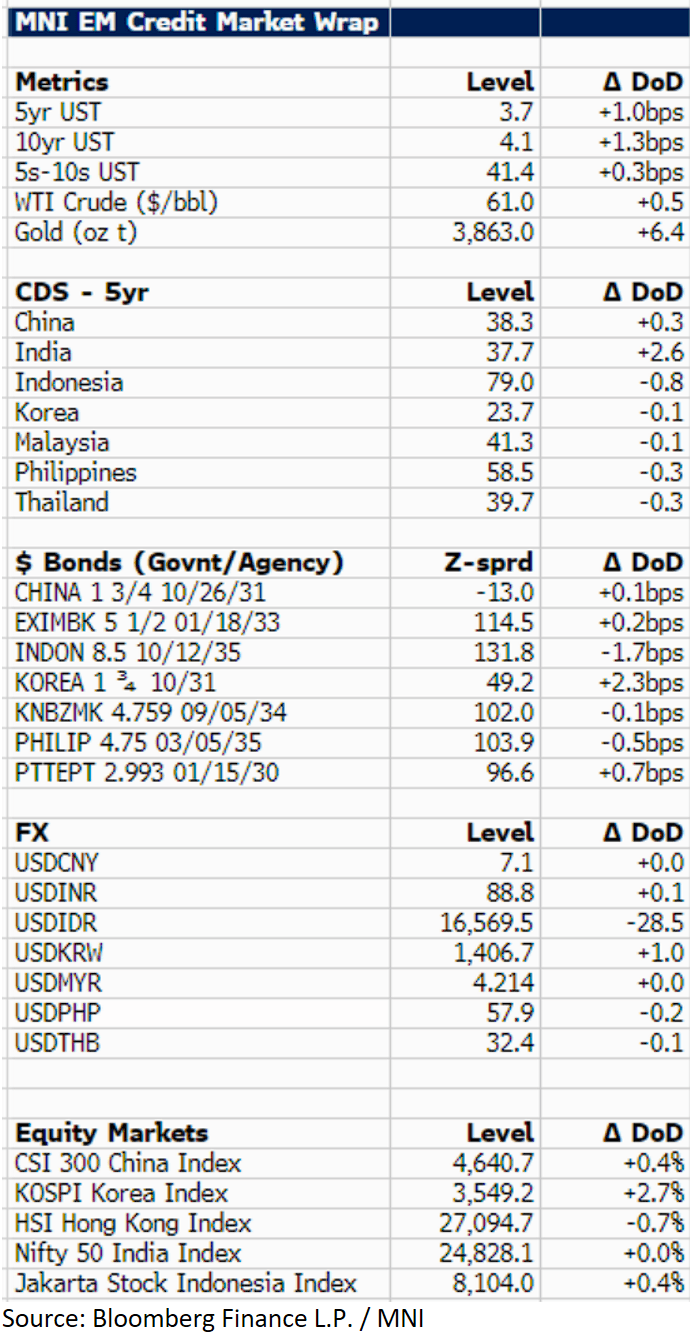

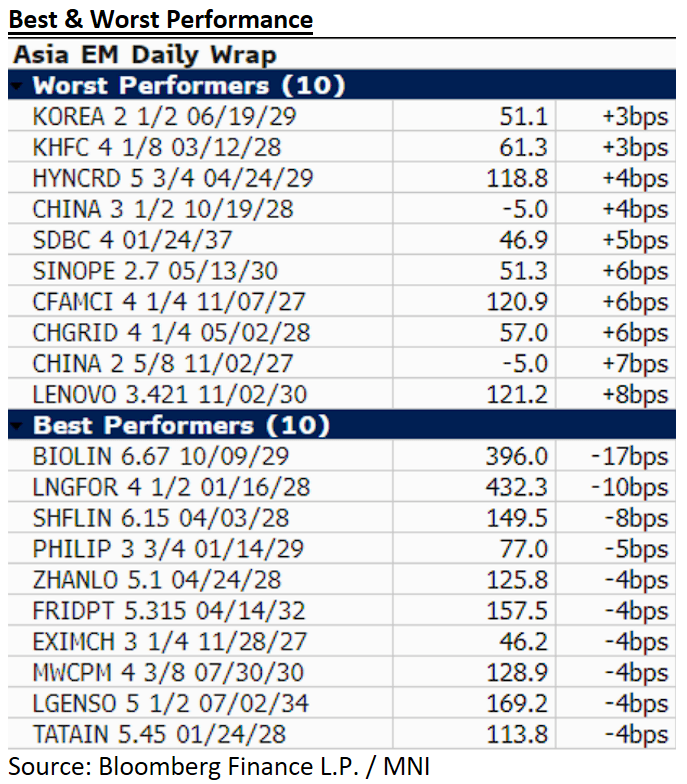

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

US Treasury yields are 1.5bp higher at 4.1% with the US government shutdown delaying the weekly jobless claims report. In LATAM, spreads were generally stable, trading in a -2 to +2 basis point range. Argentina’s bonds gained approximately 2 points, recovering some recent losses after US Treasury Secretary Bessent reassured markets that further details on US financial support would be provided.

A relatively quiet end to the week in Asia, with China and Korea out for national holidays, and not back until next Thursday (Oct 9th) and Friday (Oct 10th) respectively.

Asia EM USD sovereign and agency spreads are more or less unchanged this morning. In terms of newsflow, LG Energy announced it was sending employees back to the US, now that visa issues are resolved, and Malaysian sovereign wealth fund, Khazanah Capital, denied reports it was in talks with China on a rare earth project. No new issuance reported today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

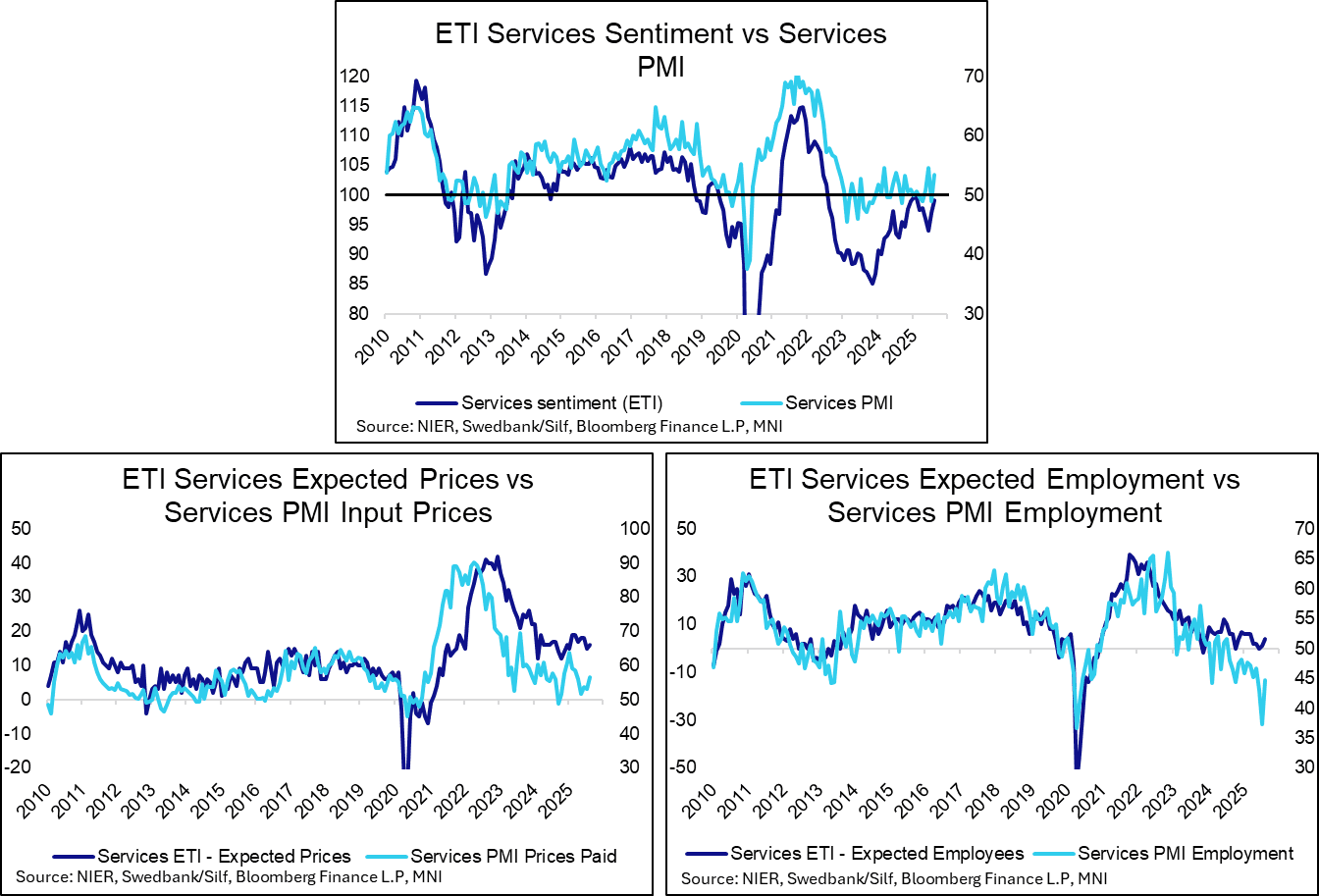

SWEDEN: Rebound In Services PMI Suggests July Was An Outlier

There was a solid rebound in the Swedish services PMI in August, rising to 53.4 after 49.0 in July and 54.6 in June. This suggests the July print was an outlier. The services reading follows an increase in the manufacturing PMI on Monday, and joins a broader set of improving Swedish activity indicators/signals from the past few weeks. That said, a Riksbank September cut remains on the cards if tomorrow’s August flash CPIF print surprises to the downside.

The employment component, which had fallen to a 5-year low of 37.8 in July, rose back to 44.6 in August (vs 43.1 in June). The index remains firmly in contractionary territory though, and continues to send a more pessimistic signal than the Economic Tendency Indicator’s services expected employment series.

RATINGS: Bank Of America Look Into Eurozone Rating Risks

Bank of America note that “even if market expectations on Eurozone member states' GDP growth and public deficit have generally deteriorated (using Bloomberg consensus for ‘26 as a discriminator), the current rating agency guidance remains relatively balanced on the likelihood of upgrades or downgrades”.

- The believe that “on the side of upgrades, Ireland, Spain, Portugal and Italy are biased for upgrades, while Austria (perhaps in 2026), Belgium and France risk downgrades”.

GILT TECHS: (Z5) Bear Cycle Intact

- RES 4: 92.06 High Aug 14

- RES 3: 91.45 High Aug 15

- RES 2: 91.24 High Aug 18 and a key near-term resistance

- RES 1: 90.16/90.84 High Sep 2 / High Aug 28 / 29

- PRICE: 89.49 @ 08:22 BST Sep 3

- SUP 1: 89.42 Intraday low

- SUP 2: 89.22 1.618 proj of the Aug 21 - 27 - 28 price swing

- SUP 3: 89.00 Round number support

- SUP 4: 88.84 2.00 proj of the Aug 21 - 27 - 28 price swing

A bear cycle in Gilt futures remains in play and a fresh cycle low again on Tuesday reinforces current conditions.The contract has started today’s session on another bearish note. The continuation of the bear leg has resulted in a break of the 90.00 handle. Clearance of this level strengthens the downtrend. Sights are on 89.34 next, a Fibonacci projection. Initial firm resistance is at 90.84, the Aug 28 and 29 high.