EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.82% +5bp

10yr UST 4.29% +6bp

5s-10s UST 47.2 +0bp

WTI Crude 64.1 +1.4

Gold 3340 -15.5

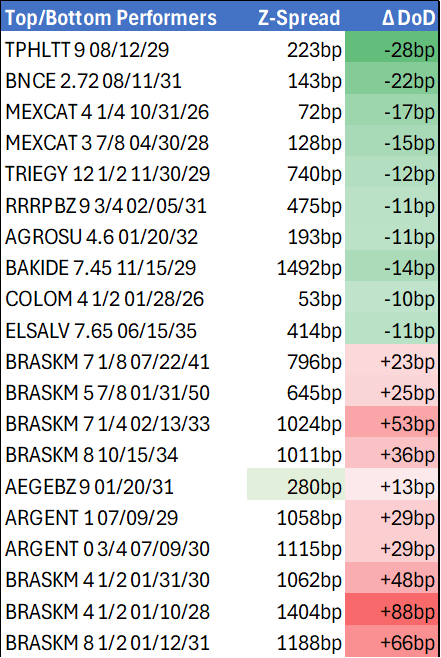

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 923bp +7bp

BRAZIL 6 1/8 03/15/34 230bp -0bp

BRAZIL 7 1/8 05/13/54 321bp -0bp

COLOM 8 11/14/35 355bp -5bp

COLOM 8 3/8 11/07/54 428bp -3bp

ELSALV 7.65 06/15/35 414bp -11bp

MEX 6 7/8 05/13/37 238bp -2bp

MEX 7 3/8 05/13/55 290bp -3bp

CHILE 5.65 01/13/37 131bp -2bp

PANAMA 6.4 02/14/35 254bp -7bp

CSNABZ 5 7/8 04/08/32 535bp -3bp

MRFGBZ 3.95 01/29/31 269bp -7bp

PEMEX 7.69 01/23/50 518bp -3bp

CDEL 6.33 01/13/35 190bp -4bp

SUZANO 3 1/8 01/15/32 163bp -5bp

FX Level Δ DoD

USDBRL 5.41 +0.02

USDCLP 966.39 +12.86

USDMXN 18.8 +0.19

USDCOP 4053.40 +24.40

USDPEN 3.57 +0.03

CDS Level Δ DoD

Mexico 97 (0)

Brazil 137 1

Colombia 190 0

Chile 51 0

CDX EM 98.03 (0.00)

CDX EM IG 101.40 (0.02)

CDX EM HY 94.61 (0.01)

Main stories recap:

· Much higher-than-expected July producer prices stirred up renewed concerns about U.S. tariff pass through inflation and led to a decline in U.S. equity indexes as well as a spike upward in bond yields.

· EM Asia secondary benchmark bond performance was mixed ahead of key US inflation data as spreads moved in a -3/+4bp range. CEEMEA and LATAM spreads tightened low single digits as relatively unchanged bond prices were unfazed by the selloff in U.S. Treasuries.

· Bonds of Brazil chemical company Braskem gave back some gains made in past days, falling 1 ½ to 2 points. Even if vulture investor Nelson Tanure decided to abandon his bid for the company thereby lowering the risk of a debt restructuring, investors would still be left with a deteriorating credit profile underscored by a weak earnings report last week and the Fitch downgrade a few days ago.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Bulls Remain In The Driver’s Seat

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6603 High Nov 11 ‘24

- RES 1: 0.6595 High Jul 11

- PRICE: 0.6515 @ 16:43 BST Jul 15

- SUP 1: 0.6509 Low Jul 15

- SUP 2: 0.6487/6373 50-day EMA / Low Jun 23 and a reversal trigger

- SUP 3: 0.6357 Low May 12

- SUP 4: 0.6275 Low Apr 14

The trend set-up in AUDUSD remains bullish and last week’s gains reinforces current conditions. Resistance at 0.6590 has been pierced. A clear break of this price point would strengthen a bullish condition and confirm a resumption of the uptrend plus maintain the price sequence of higher highs and higher lows. Scope is seen for a climb towards 0.6603 next, the Nov 11 2024 high. Initial firm support to watch is 0.6487, the 50-day EMA.

PIPELINE: Late Corporate Bond Roundup

- Date $MM Issuer (Priced *, Launch #)

- 07/15 $1.5B *Univision Communications 7NC3 9.375% (upsized from $1B)

- 07/15 $1B *Conagra $500M 5Y +102, $500M 10Y +127

- 07/15 $1B Aecom 8NC3

- Expected this week:

- 07/15 $500M Boots Group 7NC3 (includes GBP & EUR issuance)

- 07/?? $1.5B Kioxia Holdings 5NC2, 8NC3

US TSYS: Late SOFR/Treasury Option Roundup: Better Puts Post-CPI, Sites on PPI

SOFR & Treasury options saw better put volume Tuesday, outright and spd, as underlying futures rejected the initial post-CPI rally. Focus turns to Wednesday's June PPI data. Curves hold flatter profiles/well off lows, 2s10s -0.067 at 53.072, projected rate cut pricing continues to soften vs morning/pre-data (*) levels: Jul'25 steady at -0.6bp, Sep'25 at -14.1bp (-15.7bp), Oct'25 at -27.1bp (-29.4bp), Dec'25 at -43.7bp (-46.7bp).

- SOFR Options

- Block/pit, -11,500 SFRU5 95.25/95.75 put spds, 3.5 ref 95.815

- Block, 5,000 SFRU5 95.68/95.81 2x1 put spds, 4.25

- Block, -10,000 SFRZ5 96.25/96.50/96.75/97.00 call condors, 4.0 net ref 96.125

- 1,250 SFRZ5 95.75/95.87/96.25/96.37 call condors

- Block, +20,000 SFRU5 95.62 puts, cab

- -16,000 SFRH6 96.00/96.50 put spds 23.75 vs. 96.385/0.30%

- 10,250 SFRU5 95.81 puts, ref 95.84

- +2,000 SFRU5 95.87/96.00/96.06/96.18 call condors, 2.75

- 2,000 SFRU5 95.56/95.68 2x1 put spds ref 95.85

- +2,500 SFRU5 95.25/95.75 put spds, 3.5

- +5,000 SFRZ5 95.75/95.87/96.00 put trees, 2

- 4,000 SFRQ5 95.75/95.81 put spds

- Block/screen +14,100 SFRU5 95.62/95.75/95.81/95.87 broken put condors, 0.5

- +2,500 SFRU5 96.12/96.37 call spds, 1.25

- Treasury Options:

- 13,200 TYV5 108.5 puts, 32 ref 110-08

- Block, 10,000 TYV5 108/TYX5 107.5 put strip, 54 vs. 110-10/0.20%

- +10,000 TYV5 113/115 call spds 12

- Block - adds to below w/ another 18,600 USU5 108 puts, 34-35 with 13,400 at 32 on screen

- Block, total 22,500 USU5 108 puts, 28-29 vs. 112-09/0.16%

- 6,500 TYQ5/wk3 TY 110 put spds, 4

- 5,000 TYQ5 112 calls, 4

- 2,000 TUQ5 103.25/103.37/103.62/103.75 put condors ref 103-20.38

- -10,000 TYU5 109.5/112 strangles, 38

- -2,500 wk3 TY 111.25 calls, 6 vs. 110-24.5/0.25%

- -2,000 FVQ5 107.75/108 put spds, 6

- +3,500 TYQ5 109.75 puts, 5 vs. 110-25/0.08%

- 2,000 TYQ5 111.5 calls, 9 vs. 110-24.5/0.21%

- -1,000 FVU5 108 straddles, 104.5 vs. 108-04/0.10%

- +20,000 FVQ5 107.75 puts, 7.5

- +4,000 Wednesday wkly TY 111.5/111.75 call spds, 1 ref 110-23.5 to -24.5

- +10,000 TYQ5 112 calls, 4