EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.77% -5bp

10yr UST 4.24% -5bp

5s-10s UST 46.4 -0bp

WTI Crude 62.5 -0.7

Gold 3354 +6.2

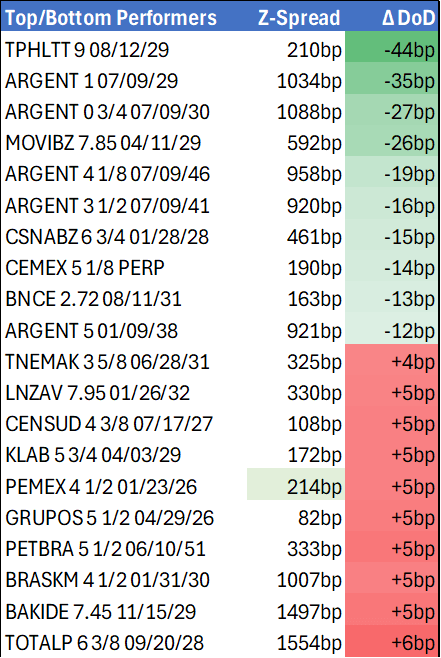

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 920bp -14bp

BRAZIL 6 1/8 03/15/34 230bp -2bp

BRAZIL 7 1/8 05/13/54 321bp -2bp

COLOM 8 11/14/35 360bp -3bp

COLOM 8 3/8 11/07/54 431bp -5bp

ELSALV 7.65 06/15/35 425bp -2bp

MEX 6 7/8 05/13/37 240bp -4bp

MEX 7 3/8 05/13/55 294bp -3bp

CHILE 5.65 01/13/37 132bp -1bp

PANAMA 6.4 02/14/35 260bp -3bp

CSNABZ 5 7/8 04/08/32 537bp -2bp

MRFGBZ 3.95 01/29/31 275bp -2bp

PEMEX 7.69 01/23/50 519bp -6bp

CDEL 6.33 01/13/35 193bp -1bp

SUZANO 3 1/8 01/15/32 167bp -1bp

FX Level Δ DoD

USDBRL 5.40 +0.01

USDCLP 953.85 -1.78

USDMXN 18.6 +0.04

USDCOP 4029.00 +9.96

USDPEN 3.54 +0.01

CDS Level Δ DoD

Mexico 97 (2)

Brazil 136 (0)

Colombia 190 (2)

Chile 51 (1)

CDX EM 98.03 0.07

CDX EM IG 101.41 (0.01)

CDX EM HY 94.62 0.14

Main stories recap:

· U.S. equity indexes inched higher and U.S. Treasury yields dropped 5bp across the curve as the cumulative effect of concerns about the labor market and yesterday’s benign inflation report led to more bullish Fed rate cut expectations.

· Asia EM benchmark bond spreads widened 2-4bps and CEEMEA spreads were mostly unchanged while LATAM spreads generally tightened 2-5bps.

· The trend in LATAM credit was positive today with a rally in U.S. Treasuries lifting prices of most benchmark bonds from high grade to high yield ½-1 ½ points.

· Earnings reports continued to stream in with no major surprises. We reported on Chile retailer Falabella, Brazil based McDonalds franchisee Arcos Dorados, Colombia financial holding company Grupo Aval and Brazil logistics and transport firm Simpar.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Breadth of Core Goods Increases Watched For Tariff Impact

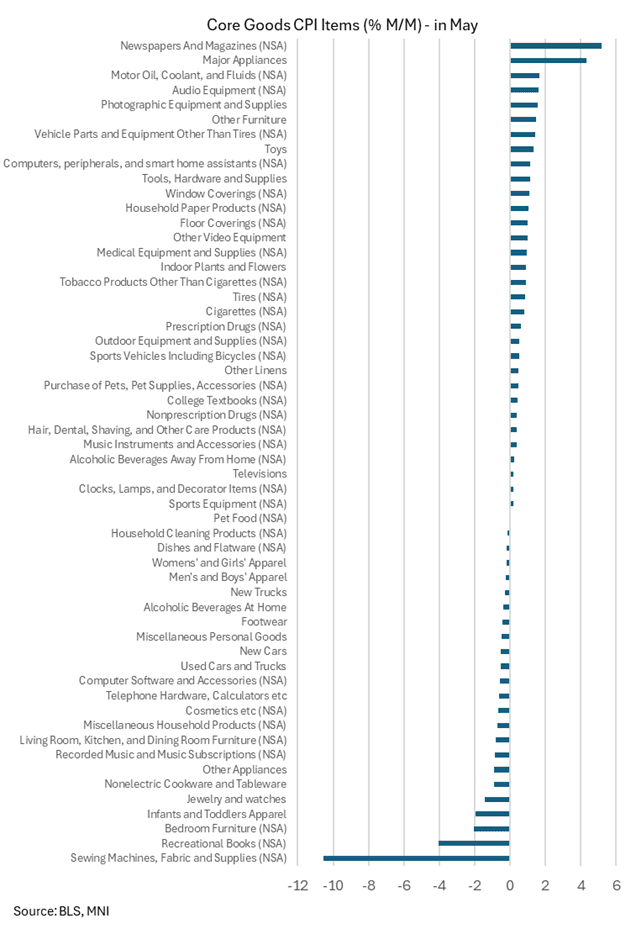

- Whilst it’s likely that upcoming months are still to see larger impacts from tariffs (see more on this in the MNI US CPI Preview, here), there were still signs of an impact within the details of last month’s May release.

- Core goods prices surprisingly fell -0.04% M/M vs analyst median expectations 0.2% M/M in May, helped by pronounced weakness in heavily weighted components such as used cars (-0.5%), new cars (-0.3%) and apparel (-0.4%).

- However, the median increase across 56 core goods items was 0.29% M/M after -0.01% M/M in April, its strongest since Sep 2022.

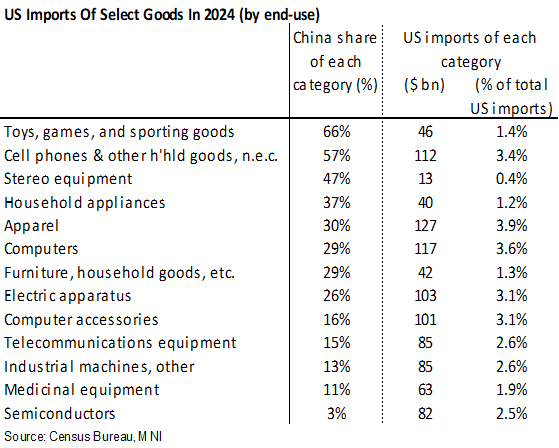

When assessing tariff impacts, we continue to expect greatest focus on those with a China-heavy affiliation, such as toys, cell phones, broad electrical/computing equipment and apparel despite the de-escalation in US-China trade policy on May 12 after Geneva talks when tariffs imposed by the US in 2025 were reduced from 145% to 30%.

AUDUSD TECHS: Trend Structure Remains Bullish

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6603 High Nov 11 ‘24

- RES 1: 0.6595 High Jul 11

- PRICE: 0.6556 @ 16:09 BST Jul 14

- SUP 1: 0.6534 20-day EMA

- SUP 2: 0.6485/6373 50-day EMA / Low Jun 23 and a reversal trigger

- SUP 3: 0.6357 Low May 12

- SUP 4: 0.6275 Low Apr 14

The trend set-up in AUDUSD is unchanged, it remains bullish and last week’s gains reinforces current conditions. Resistance at 0.6590 has been pierced. A clear break of this price point would confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Scope is seen for a climb towards 0.6603 next, the Nov 11 2024 high. Initial firm support to watch is 0.6485, the 50-day EMA.

US TSYS: Late SOFR/Treasury Option Roundup

SOFR & Treasury option trade remained mixed Monday, SOFR leaning towards low delta calls & call spds (+50k Green Mar'26 call spd for instance). Underlying futures off midday lows, curves adding to Fri's steepening (2s10s +0.744 at 52.760). Projected rate cut pricing cooled slightly vs morning (*) levels: Jul'25 at -1.2bp (-1.7bp), Sep'25 at -16.2bp (-15.9bp), Oct'25 at -30.7bp, Dec'25 at -48.9bp (-49.1bp).

- SOFR Options:

- +4,000 SFRZ5 95.62/SFRH6 95.75 put strip, 5.25 total

- 6,000 SFRU5 96.50 calls ref 95.85

- +10,000 2QZ5 97.00/97.50 call spds vs. 3QZ5 96.75/97.25 call spd, 0.0 net/steepener

- +5,000 SFRZ5 95.56/95.62/95.68 put trees, ref 96.14/0.05

- Block, +5,000 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.0 net ref 96.145

- -2,500 SFRZ5 96.50 calls, 9.0 ref 96.145

- +15,000 SFRQ5 95.81/95.93/96.00 put trees, 1.0

- Block, 5,000 2QU5 97.00/97.50 call spds vs. 3QU5 96.75/97.25 call spds. 0.5 net Gr Sep over

- Block, +50,000 2QH6 98.00/98.25 call spds, 1.0 ref 96.56

- 2,400 0QV5 96.81 straddles ref 96.785

- 4,000 0QQ5 96.87/97.00/97.12 call flys, 1.0 ref 96.735 to -.74

- 1,000 SFRU5 95.81/95.87/96.18 broken call trees, 0.75 ref 95.855

- Block/screen, +8,000 SFRU5 95.87/96.00/96.06/96.18 call condors, 2.75 ref 95.855

- Treasury Options:

- 1,500 USV5 106/108 put spds 28 ref 112-06

- 10,000 TYV5 113/115 call spds ref 110-19.5

- 5,000 TYU5 112 calls, 25

- 5,800 TYU5 109 puts, 15 ref 110-25 to -24.5

- -2,000 TYV5 110.5 straddles, 218, ref 110-22

- 2,300 wk3 FV 108.5/109 call spds, 4.5 ref 108-05.5 (exp 7/18)

- +1,000 TYQ5 109/109.75/110.5 put flys, 9 vs. 110-23/0.11%

- -2,100 TYQ5 110.75 calls, 26 ref 110-23.5/0.52%

- -1,670 TYQ5 110/111 put spds, 25 ref 110-25.5/0.57%

- 2,000 TYU5 110 puts, 31

- +2,000 Wednesday wkly TY 112 calls, 1