OPTIONS: Larger FX Option Pipeline

Jun-30 11:45

- EUR/USD: Jul03 $1.0720-30(E1.1bln), $1.0779-85(E1.3bln), $1.1070-85(E1.2bln); Jul04 $1.0750-65(E1.1bln); Jul05 $1.0900(E1.6bln)

- GBP/USD: Jul05 $1.2565-75(Gbp1.0bln)

- AUD/NZD: Jul03 N$1.0950(A$1.0bln), N$1.1000(A$1.2bln)

- USD/CNY: Jul05 Cny7.2000($1.4bln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: GoCs Outperform Ahead of GDP, RBC Recommends Long 10Y

May-31 11:44

- GoCs slightly extend the decent shift richer at the open, with 2-10Y benchmark yields all within +/-0.5bps of -5bps on the day and only the 30s lagging with -4bps.

- GoCs modestly outperform Treasuries across the curve, most notably at the front end with 2YY Tsys -2.7bps.

- RBC recommended long 10Y GoCs, with an entry 3.25%, target 2.75% and stop 3.51%, with a 2-3 month trading horizon. Rationale: "Yields (5s-30s) are near the 90th percentile of the 1yr range. It has paid to fade the extreme levels".

- "10y tenor chosen over (i) 2s to protect against BoC being re-priced higher, (ii) preferred to 5s given that tenor remains expensive on an RV basis (ie. fly very depressed), and (iii) superior to 30s as 10s30s tends to steepen when 10s move lower".

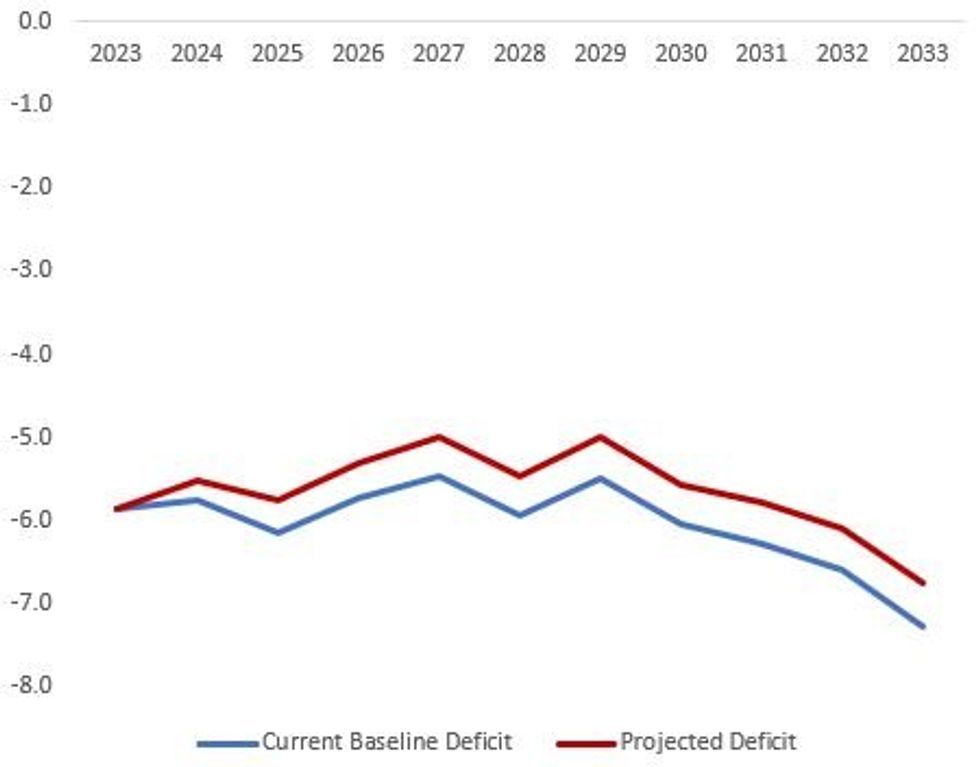

US: Macro Impact Of Debt Limit Bill Looks Modest (2/2)

May-31 11:32

Overall, the macro impact from the debt limit bill looks limited, apart from relieving uncertainty over the prospect of a near-term US debt default.

- The GDP equivalent deficit reduction in 2024 will be on the order of 0.2-0.3% of GDP lower vs baseline, growing slightly over the next decade in part due to lower implied debt servicing costs - see chart.

- To put that in context - over a decade, the cumulative deficit reduction in nominal dollars of $1.5T compares to nominal cumulative GDP projected at $332T, so about 0.45% GDP, and the 2023 deficit estimated at 5.9% of GDP.

- Another basis of comparison is the 2011 debt limit agreement which reduced deficits by $2T - that led to a projected 0.7% of GDP deficit reduction in 2012.

- They key macro impact of the deal in the short term is likely to come from the deal's cementing the end of federal student loan forbearance by Aug 30. This has no impact on the fiscal deficit projections because it had already been assumed by the CBO, and student debt relief had probably been likely to end by the fall anyway.

- But the end of forbearance will drag on consumer spending via a reduction in disposable personal income by a mostly high-spending-propensity demographic. There could be a sudden impact as well in September as debt repayments start back up (we've seen estimates of the average monthly forbearance at $250-400 per month per impacted borrower).

- For example: JPM estimates the spending reduction impact at 0.1% of GDP, though GDP could be hit at 0.25-0.5% quarterly annualized in a short period of time.

Annual Deficits As % of GDPSource: CBO, MNI

Annual Deficits As % of GDPSource: CBO, MNI

CANADA DATA: Q1 GDP Preview - 0830ET

May-31 11:27

- Q1 GDP lands at 0830ET, with consensus 2.5% and the BoC’s April forecast of 2.3% annualized after Q4’s surprisingly soft 0.0% on the back of a heavy drag from inventories.

- With the Bank estimating potential growth at 2.3% in 2023, it would mark a quarter with zero progress in demand softening to allow supply to move in better balance.

- Being the last major release before the BoC decision on Jun 7, a beat could see the 25bp hike priced later in the year start to be expected next week having been between 1/4 and 1/3 odds in recent days.

- In the separate monthly data, analysts see power outages in Quebec and the federal workers’ strike disrupting April GDP, with CIBC and RBC looking for another slight decline after the -0.1% M/M indicated by the March advance. RBC estimate the PSAC strikes shaved off 0.3pps from April GDP.

- This latest monthly momentum into Q2 could help bias market reaction to the quarterly data the BoC focuses on.