US LABOR MARKET: Large Negative Benchmark Revision Baked In For Payrolls

Feb-09 16:51

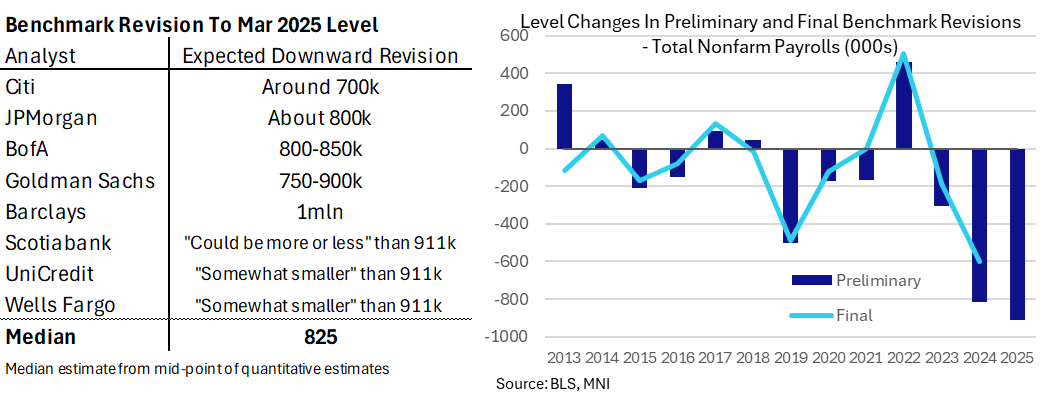

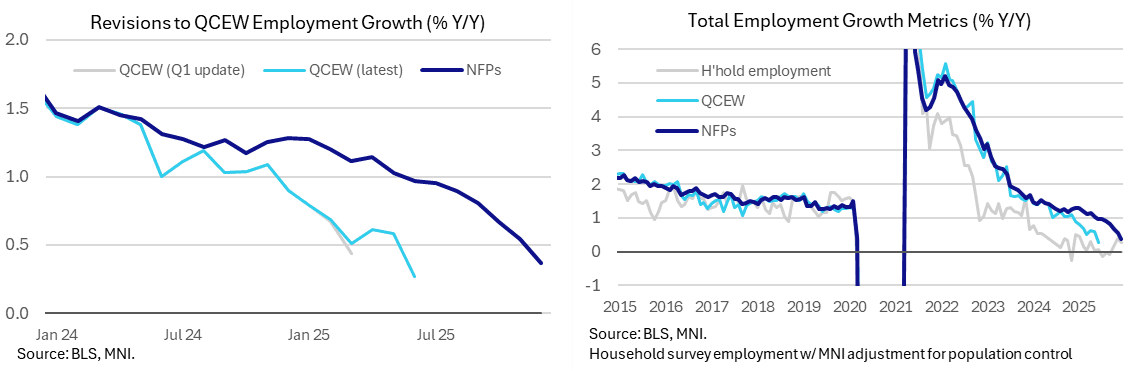

- Cumulative growth in nonfarm payrolls across April 2024 to March 2025 was likely significantly lower than first reported judging by data from the more comprehensive QCEW survey.

- We expect a 700-800k downward revision to the level of Mar 2025 payrolls in this month’s payrolls release, with some limited analyst estimates in a roughly similar range albeit a little higher with a median mid-point of 825k across five estimates.

- There’s a general consensus that we see a smaller downward revision that the 911k indicated in the preliminary benchmark revision estimate published in Aug 2025, but with Barclays a standout with that 1 million downward revision (Scotiabank also don’t rule out a larger downward revision either).

- This sort of magnitude for a downward revision has long been expected – with repeated references by senior Fed figures – and is a continuation of what was seen in the previous year’s revisions as well. Indeed, Fed Chair Powell has for a few months now touted that monthly payrolls growth in current vintages could be overstated by 60k/month (i.e. ~720k annualized) “and, you know, that could be wrong by 10 or 20 in either direction”.

- More recently, Fed Governor Waller in his dovish dissent after last month’s FOMC meeting: “Compared to the prior ten-year average of about 1.9 million jobs created per year, payrolls increased just under 600,000 for 2025. And, last year's data will be revised downward soon to likely show that there was virtually no growth in payroll employment in 2025. Zero. Zip. Nada. Let this sink in for a moment—zero job growth versus an average of almost 2 million for the 10 years prior to 2025. This does not remotely look like a healthy labor market.”

- For context, last year’s benchmark revision process saw a preliminary estimate of -818k before a final -598k in non-seasonally adjusted terms.

- We suspect it will take a benchmark revision either side of -600k and -1,000k to have an impact in isolation. What that reaction should look like is questionable though: whilst a particularly large downward revision would likely be met with a snap dovish reaction, it would also imply a lower breakeven pace for payrolls growth considering the unemployment rate will have been unaffected. Of course, that's likely only of so much comfort for the Fed, per Waller's argument.".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: MNI TEST 02, Please Ignore

Jan-09 23:36

Test Test TEST

MNI: MNI Test, Please Ignore

Jan-09 23:30

Test, ignore

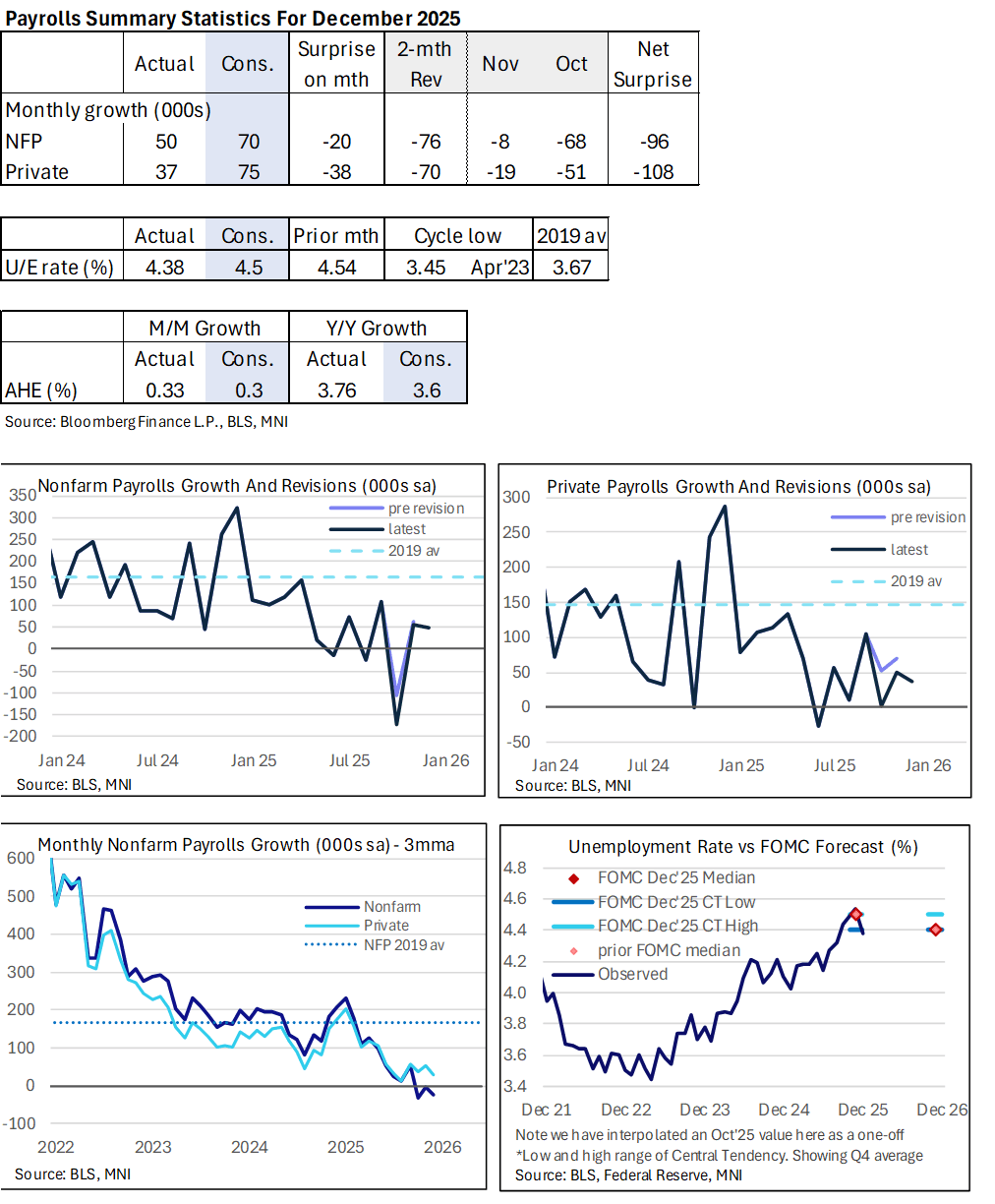

US LABOR MARKET: MNI US Employment Insight: U/E Rate Improves But Payrolls Soft

Jan-09 21:16

- We have published and e-mailed to subscribers the MNI US Employment Insight.

- Please find the full report, including detailed MNI analysis of the payrolls release plus a variety of other key labor indicators, here: https://media.marketnews.com/US_Employment_Report_Jan2026_3a3292abe9.pdf