EQUITIES: Large Estoxx block

Large block in Estoxx, suggest buyer:

VGU3 30k at 4409.00 and 5k at 4400.00.

EU1.5bn worth of Notional.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

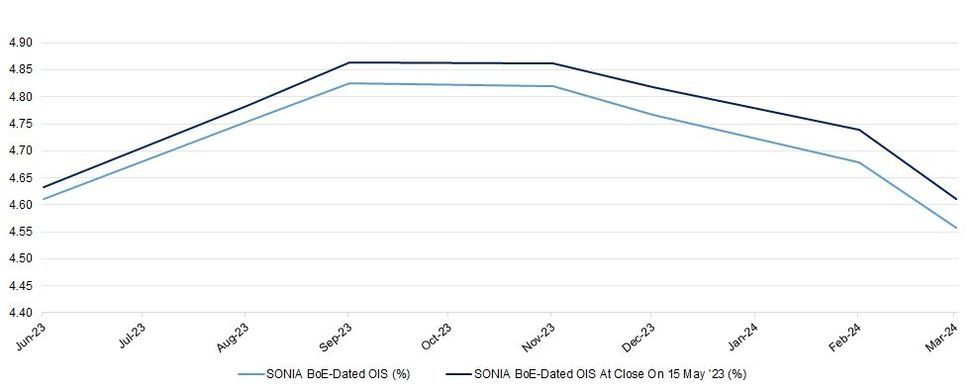

STIR: BoE Pricing A Touch Softer On The Day, Bailey Due To Speak

Global market impulses bias MPC-dated OIS pricing a touch softer today after the domestic labour market data-inspired downtick on Tuesday (although yesterday saw some counter from spill over from Fed pricing, leaving the space of dovish extremes). ~40bp of tightening is priced in before the terminal rate of the current cycle is attained, meaning terminal BoE policy pricing is in the familiar ~4.90% zone. A 25bp cut is then slightly more than fully priced come the end of the Bank’s Mar ’24 meeting.

- BoE Governor Bailey will be speaking at the British Chambers of Commerce today, with text released at 1050BST. No specific subject line for his speech just yet, but it will be the keynote address of the event.

| BoE Meeting | SONIA BoE-Dated OIS (%) | SONIA BoE-Dated OIS At Close On 15 May '23 (%) |

| Jun-23 | 4.611 | 4.633 |

| Aug-23 | 4.753 | 4.784 |

| Sep-23 | 4.825 | 4.865 |

| Nov-23 | 4.819 | 4.862 |

| Dec-23 | 4.766 | 4.818 |

| Feb-24 | 4.678 | 4.739 |

| Mar-24 | 4.559 | 4.610 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

USD: USDJPY test the 137.00 handle

- USDJPY test the Psychological 137.00 handle, and looking at the chart, there isn't much in terms of resistance until the 2023 high situated at 137.91.

Chart source: MNI/Bloomberg.

CROSS ASSET: CSI & Hang Seng Struggle, USD/CNY Tops 7.00

The CSI 300 struggled on Wednesday, shedding 0.5%, while the Hang Seng is 2.1% weaker into the close.

- This came as new home price data added to the recent run of disappointing Chinese releases, although international investors were seemingly undeterred, reverting to net purchases of mainland equities via the Hong Kong Stock Connect links (for a limited CNY1.69bn) after breaking a seven-day streak of net purchases on Tuesday.

- Nomura became the latest sell-side name to trim their Chinese GDP growth forecasts (to 5.5% for this year and 4.2% for next year).

- Alibaba & Tencent earnings present the earnings reports of note over the next 24 hours or so. Expectations ahead of those releases partially insulated the two tech giants from the wider sell off, leaving them flat on the day late on.

- USD/CNH shows back above the CNH7.00 mark for the first time since December, with USD/CNY following suit in recent dealing. This came after a neutral USD/CNY mid-point fixing gave the greenlight for such moves to develop. Still USD/CNH & USD/CNY are far less “priced” for a meaningful Chinese economic slowdown then say 5-Year IRS or 10-Year CGB yields, purely based on an eye test vs. late ZCS-era levels. 1-month risk reversals in USD/CNH are still shy of YtD highs after a relatively sharp pull away from YtD lows MtD. Meanwhile, YtD highs in that metric sit comfortably off ’22 peaks.