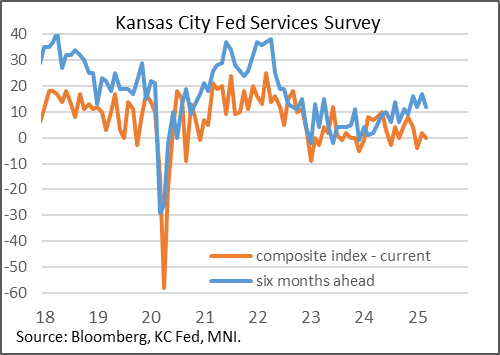

US DATA: KC Fed Services Activity Declines Only Slightly, Defying Broader Trend

The Kansas City Fed's services sector survey showed a small pullback in the composite index to 0 in March from 2 prior, suggesting flat activity on the month - though this was still better than the 13-month low -4 in January.

- The moderate decline contrasts with other regional Fed services surveys (NY, Philly) that saw much sharper drops in March amid tariff-related uncertainty.

- The internals of the KC report were mixed: "Activity in tourism & hotels grew and declines eased in the wholesale, real estate, and professional services, and education sectors. Healthcare and retail activity fell further. The month-over-month indexes were mixed. General revenue/sales picked up from -1 to 4, while employment decreased from 3 to -5. Employee hours worked decreased to its lowest reading since May 2020 at -10. The year-over-year composite index cooled further from 6 to 2, as growth in the business sector eased and consumer activity remained flat. Revenues were steady, but employment fell from the previous year’s levels for the first time since April 2024. Capital expenditures and access to credit fell only slightly."

- Expectations pulled back to 12.0 from 17.0 prior, still positive but "with firms expecting lower sales and employment growth in the coming six months."

- And the anecdotes in the report were much more negative on balance: “Customers are feeling pinched while tariffs have elevated our input costs. The short-term economics for us look dreadful and that will have an effect on our employment and investment in the business...Many economic headwinds making growth very difficult....Our sales increased this month. The adjusted interest rates and a reduction in our input costs is having a positive effect on consumers’ confidence...Customers are cutting back....Tariffs are killing us, just the thought of tariffs and the uncertainty they cause. Our stores are in high traffic shopping areas and all are quiet...As a small business, we are finding it difficult to gain new business because we don't have the resources to compete with the bigger companies...Some re-investment will be deferred until 2026 so we can recover from 4th quarter 2024...We are expanding and adding staff. Still tough finding quality blue collar workers."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking forward to sell GBP4.25bln of the 4.375% Mar-30 Gilt (ISIN: GB00BSQNRD01) at its auction next Wednesday, March 5.

US DATA: New Home Sales Pull Back, Still Mitigating Existing Home Weakness

New home sales fell much more sharply in January than expected, but this was more than made up for by upward revisions.

- The 657k (SA annualized) of new single-family house sales were below the 680k survey - but December was revised a substantial 36k higher to 734k, meaning the actual 2-month total was 14k higher than the "expected" total.

- Sales fell in each of the 4 geographic regions in January, with the exception of the West.

- In terms of inventory, December now turns out to have had a sharp drop in months of supply (8.0, vs 8.5 pre-revision), but this rebounded sharply to 9.0 months in January.

- Median prices rose 3.7% Y/Y, the strongest since January 2024, to the 2nd-highest monthly price ever $446.3k (non-seasonally-adjusted - the record was $460k in October 2022) - the average in January was $510k.

- Bigger-picture, new home sales were down 1.1% Y/Y, so not exactly dynamic.

- But new homes continue to represent an unusually elevated proportion of supply (30%, vs half that pre-pandemic) and total sales (14-15%, vs 10% or lower pre-pandemic) as existing home sales growth stagnates amid high mortgage rates.

BUNDS: /SWAPS: Commerzbank Reiterate Shorts In Long End ASWs

Commerzbank write “although Schatz ASW spreads remain resilient, Bund ASWs are hitting new lows and even underperform against 30s as markets prepare for persistent fiscal slippage under the new German government. As the game of brinkmanship for fast-tracking new expenditures gathers pace, more volatility could be in store, but Bunds will struggle to regain their 'special' status, regardless of the eventual legislative details to free up fiscal space”.

- They suggest that “combined with converging duration free-floats across the 'pristine' global bond markets this implies further catch-up with U.S. Treasury and Gilt ASW structures”.

- Therefore, they reiterate structural shorts in (ultra-)long Bund spreads, both outright and vs. Schatz.