STIR: Just Under 75bp Of BoE Hikes Priced As Oil Edges Lower, UK Politics Eyed

A move lower in oil prices since yesterday's SONIA settlement window has filtered into a modest dovi...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Just Under 45bp Of BoE Hikes Priced, Governor Bailey Eyed

Dovish adjustments in GBP STIRs since yesterday’s SONIA settlement, with oil lower over that horizon.

- The move in oil comes alongside signs of willingness re: a fresh U.S.-Iran meeting alongside ongoing talks, the passage of 30+ vessels through the Strait of Hormuz on Monday (per comments from U.S. President Trump) and Gulf pressure on the U.S. to cease its Hormuz blockade.

- ~6bp of hikes priced for this month, 18bp through June, 29bp through July and 44bp through December. Contracts covering ’26 meetings are 0.5-2.0bp less hawkish vs. close.

- SONIA futures 0.5-6.0 firmer. SFIZ6 is 7.0 below last week’s recovery high, which protects next resistance at the March 18 closing level (96.035).

- We previously flagged the SFIM6/Z6/M7 fly as a suitable weekend hedge for a breakdown in the U.S.-Iran talks, yesterday’s move higher in that structure stalled around the 30bp mark.

- With the potential for a second round of talks now increased, some may look to deploy SONIA/Euribor December ’26 narrower plays, given the elevated beta of UK rates to energy price swings. The payoff profile of such a structure isn’t clear cut, given the ~30.0 retrace from March closing highs in the spread.

- Comments from BoE’s Bailey (17:05 London), Greene (15:00 London) & Mann (09:50 London) are due today.

- Governor Bailey's comments will likely be most pertinent for markets, after his recent Reuters interview in which he alluded to market pricing of rate hikes getting ahead of itself. Any further reference to market pricing or waiting for more information will be key here.

- A reminder that MPC member Taylor (dove) noted that the state of the economy when a shock, such as the current energy one, hits is crucial and there is no simple read across from past shocks on Monday.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Apr-26 | 3.787 | +5.7 |

Jun-26 | 3.908 | +17.8 |

Jul-26 | 4.018 | +28.8 |

Sep-26 | 4.121 | +39.1 |

Nov-26 | 4.160 | +43.1 |

Dec-26 | 4.173 | +44.3 |

Feb-27 | 4.177 | +44.8 |

Mar-27 | 4.172 | +44.3 |

Apr-27 | 4.159 | +43.0 |

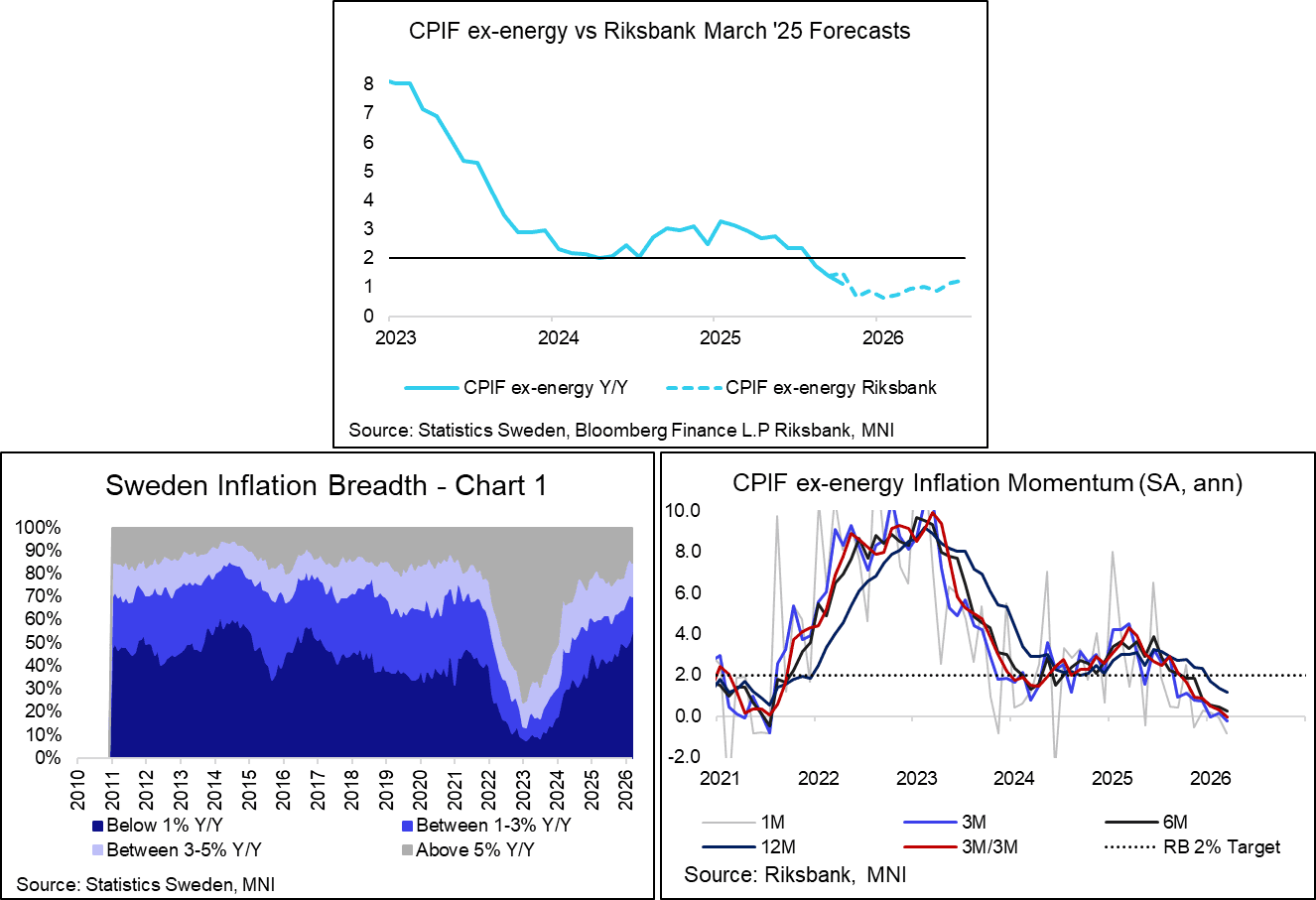

SWEDEN: Final March Report Confirms Lower Underlying Inflation Pressures

Swedish CPIF ex-energy inflation confirmed flash estimates in March, with the 1.13% Y/Y print well below the Riksbank’s 1.48% March MPR projection. We estimate seasonally adjusted underlying inflation at -0.07% M/M (vs 0.00% prior), which pulled 3m/3m momentum negative. The share of CPIF subcomponents with annual inflation rates below 1% also rose to 55% (vs 50% prior). The details confirm that underlying inflation pressures were low heading into the Iran war, which should mean any hawkish Riksbank reaction should be less aggressive than the ECB, for example. Headline inflation was 1.6% Y/Y vs 1.7% prior, with lower electricity prices offsetting higher fuel prices.

- As foreshadowed in the flash release, food inflation was soft at 0.48% Y/Y (vs 1.95% prior). A reminder that the temporary food VAT tax cut comes into effect from April, which is expected to pull this component down further.

- Services inflation was 1.94% Y/Y (vs 2.14% prior). We estimate seasonally adjusted services at 0.01% M/M (vs 0.15% prior), pulling 3m/3m momentum down to 0.24% (vs 0.71% prior), the lowest since August 2021.

- This was driven by recreational services (1.20% Y/Y vs 1.79% prior), accommodation services (-0.03% YY vs 2.59% prior) and insurance and financial services (3.36% Y/Y vs 3.48% prior). Other services, including volatiles such as package holidays and airfares, accelerated relative to February. Rent payments were broadly steady, with an uptick in actual rents offset by a decline in imputed rents.

- Goods ex-food inflation was -0.83% Y/Y (vs -1.26% prior). Seasonally adjusted goods were 0.05% M/M (vs -0.12% prior), with 3m/3m momentum still negative at -0.30% (vs -1.70% prior).

Clothing and footwear inflation was 1.61% Y/Y (vs -0.33% prior), while furnishings and household equipment was -3.55% Y/Y (vs -3.23% prior). Accelerations in vehicle inflation was seen alongside decelerations in recreational goods and personal care goods.

WTI TECHS: (K6) Monitoring Support

- RES 4: 126.49 - 1.618 proj of the Mar 10 - 23 high-low price swing

- RES 3: $123.68 - High Jun 14 ‘22 (cont) and a key resistance

- RES 2: $120.00 - Psychological round number

- RES 1: $117.63 - High Apr 7 and the bull trigger

- PRICE: $97.34 @ 07:23 BST Apr 14

- SUP 1: $91.05 - Low Apr 8

- SUP 2: $86.79 - 50-day EMA

- SUP 3: $75.64 - Low Mar 10

- SUP 4: $69.00 - Low Mar 2

Recent weakness in WTI futures is for now, considered corrective. The contract traded through the 20-day EMA, at $98.00. Attention for now is on support at the 50-day EMA, at $86.79. A clear break of the 50-day average is required to highlight a stronger short-term reversal. On the upside key resistance and the bull trigger has been defined at $117.63, the Apr 7 high. Clearance of this hurdle would confirm a resumption of the uptrend.