STIR: Just 9bp Of Fed Cuts Priced For July With U.Mich Fully Digested

May-16 16:47

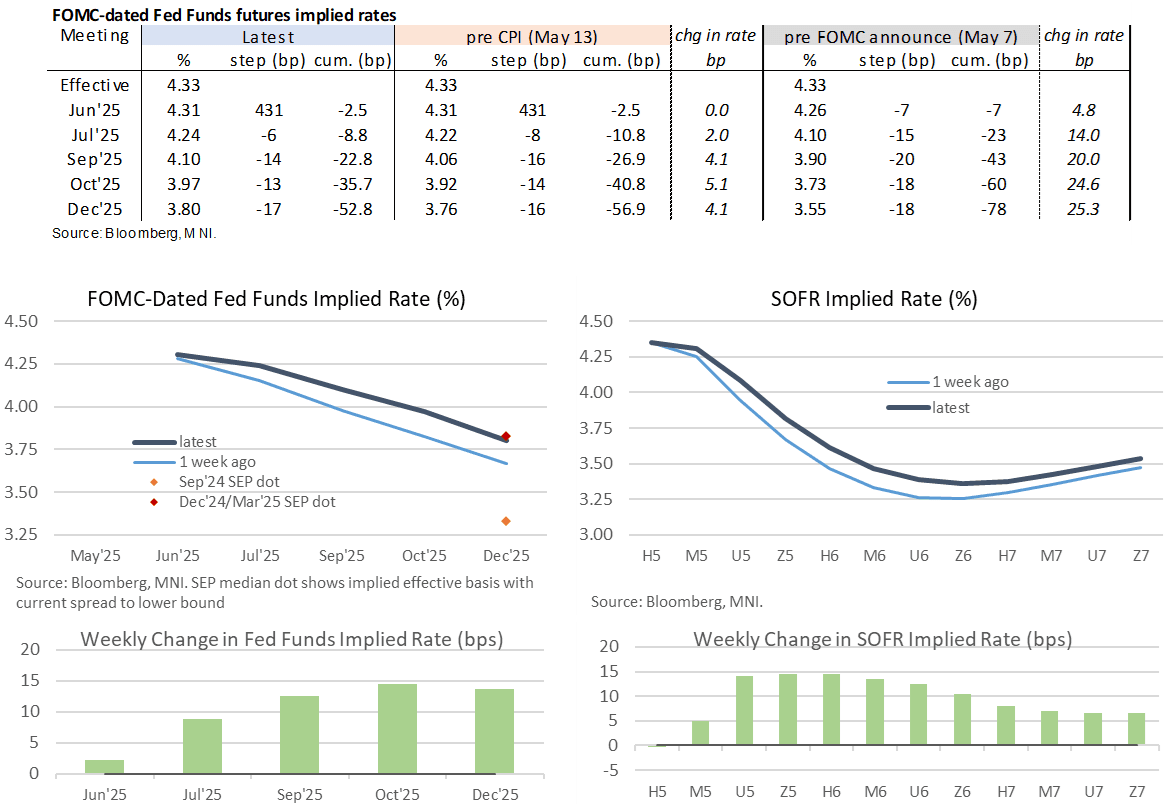

- Fed Funds implied rates are heading toward the end of the week at the higher end of their range.

- The second lowest ever reading for U.Mich consumer sentiment was caveated by the press release noting that “Many survey measures showed some signs of improvement following the temporary reduction of China tariffs” but had come at the end of the preliminary survey period and as such didn’t have much impact on the overall figure.

- Thursday’s lowering of core PCE tracking after PPI and soft core retail sales metrics in April have for now kept rates off what had been Wednesday’s hawkish extremes for the post-reciprocal tariff period.

- Cumulative cuts from 4.33% effective: 2.5bp Jun, 9bp Jul, 23bp Sep, 36bp Oct and 53bp Dec.

- The SOFR implied terminal yield of 3.36% (SFRZ6) is only 1.5bps lower on the day for 10bp higher on the week, implying broadly 100bp of cuts from current effective levels.

- The de-escalation in US-China trade policies over the weekend and Monday has seen various analyst view changes to later Fed cuts, including TD Securities next eyeing October Barclays & JPM now looking for December.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 19Y-10M BOND AUCTION: NON-COMP BIDS $116 MLN FROM $13.000 BLN TOTAL

Apr-16 16:45

- US TSY 19Y-10M BOND AUCTION: NON-COMP BIDS $116 MLN FROM $13.000 BLN TOTAL

TARIFFS: Meloni To Probe Trump For Solution To Tariff Standoff

Apr-16 16:41

On Thursday, Italian Prime Minister Giorgia Meloni will become the first European leader to sit for a face-to-face meeting with US President Donald Trump since he imposed his 'Liberation Day' tariffs. On Friday, Meloni will return to Rome to host Vice President JD Vance for a state visit.

- Politico notes: “Meloni’s personal engagement with Trump has set nerves jangling in other EU capitals. But as the bloc faces up to a potentially ruinous trade war, even her wariest counterparts are coming round to the idea that she may be the only European leader he is willing to listen to.”

- An Italian official said: “Having Trump’s ear is an asset for the entire European Union,” highlighting Meloni’s “ideological affinities with the world of American conservative right-wing politics.”

- However, as Semafor notes that Italy, “is a laggard on the key issues Trump values: Italy spends far below the European average on defense, and has a hefty trade surplus with the US.”

- Bloomberg writes: “The question for Meloni to ask is: What, if anything, does the US really want? Any hint of an answer would be of huge value to a Europe that remains stumped," noting that European Union Trade Commissioner Maros Sefcovic left a meeting with his US counterparts this week still waiting for the US to “define its position.”

Figure 1: EU Trade Balance In Goods With the United States

Source: Politico

US TSYS/SUPPLY: 20Y Preview: Another Test Of Duration Demand

Apr-16 16:33

- Treasury sells $13bn of the 20Y re-open at 1300ET (912810UJ5), in another test of duration demand although seemingly not as important as last week’s 10Y and 30Y offerings.

- Those auctions saw solid results and helped limit deleveraging pressures, including an all-time high for indirect take-up in the 10Y (assuaging fears of a slide in foreign demand) and a 2.5bp stop through for the 30Y.

- Bloomberg currently shows the WI yield at 4.8075%, off the day’s highs of 4.845% to modestly trim outright concession after the 4.632% high yield in March.

- 5s30s, an area of interest amidst deleveraging pressures of recent weeks, sits at 83bps (+3.4bp) for off last week’s high north of 95bp but holding the bulk of the steepening over the past month.

- 20Y auctions have been a mixed bag in recent months, stopping through by 1.4bp last month (largest since Jun 2024) but with a five-auction average tail of 0.6bp.

- There’s a similar story for bid-to-cover, at 2.78x in March (highest since Apr 2024) vs a five-auction average of 2.56x.

- Indirect take-up is likely again to receive attention. The 68.8% in March and a five-auction average of 66.6% weren't particularly unusual in either direction.