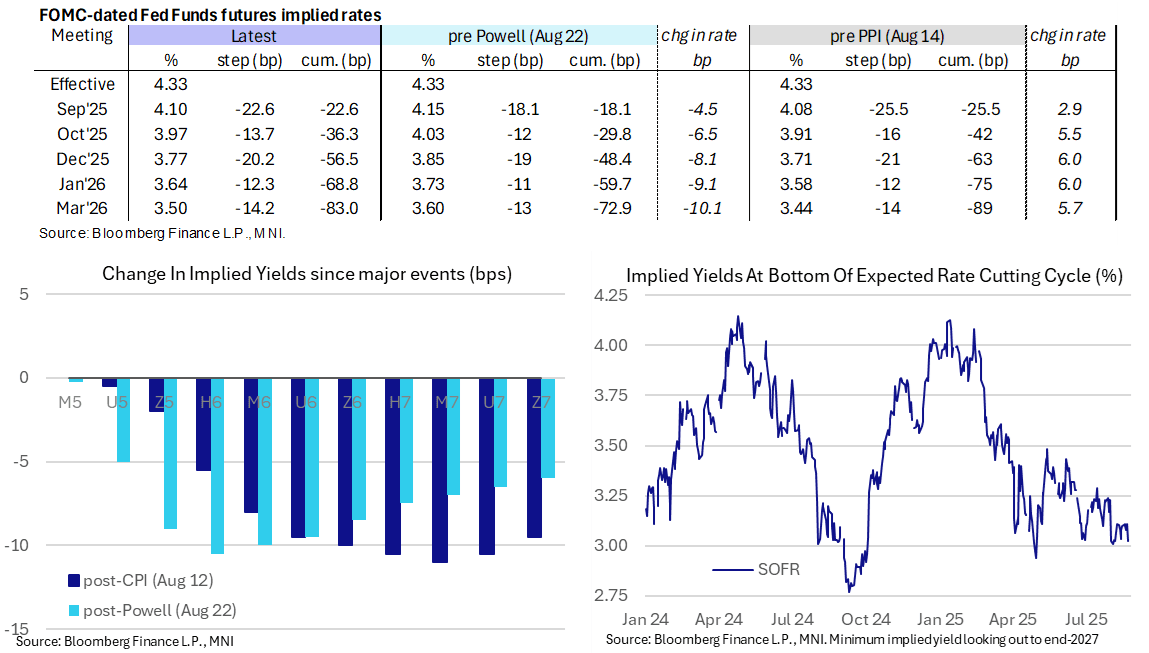

STIR: Back To Nearly Fully Pricing Fed Sept Cut, Two Cuts Seen By End-2025

Aug-22 14:27

- Fed Funds implied rates have slid 4.5bp for the Sept decision (leaving 22.5bp of cuts priced) and 8bp for the Dec decision (leaving a cumulative 56.5bp) on Fed Chair Powell’s Jackson Hole text.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 36.5bp Oct, 56.5bp Dec, 69bp Jan and 83bp Mar.

- SOFR implied yield declines are led by the H6 contract, -11bps (-10bp post-Powell).

- The terminal yield of 3.025% (H7) is -8.5bp on the day, at what would be its lowest close since Aug 1 payrolls and Aug 4.

- The dovish shift is helped by Trump since saying he’ll fire Fed Gov. Cook if she doesn’t resign. Whilst the WSJ had reported he was looking at firing her for cause, it’s still an escalation from his previous call for her to resign.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Key Inter-Meeting Fed Speak – July 2025

Jul-23 14:23

Ahead of next week's Fed decision, we've published our summary of FOMC participant communications since the June FOMC meeting, including MNI's Hawk-Dove Matrix and a recap of the latest Beige Book and June meeting minutes.

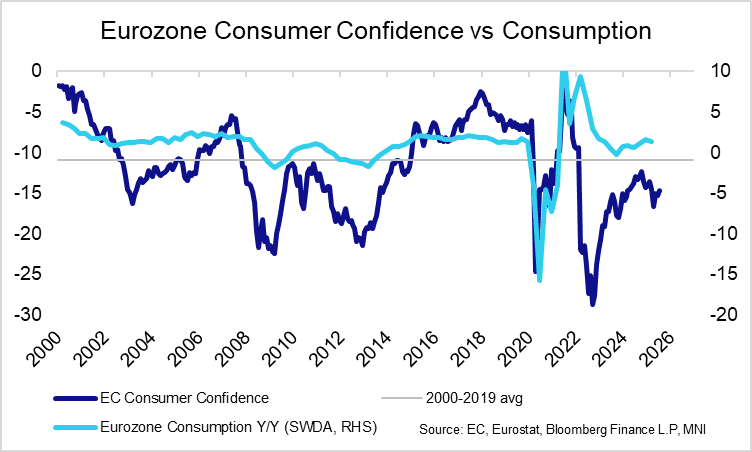

EUROZONE DATA: July Cons Confidence Slightly Better Than Exp, More Focus on PMIs

Jul-23 14:23

Eurozone flash consumer confidence was slightly stronger than expected in July, printing at -14.7 (vs -15.0 cons, -15.3 prior) for a four-month high. However, the index remains comfortably below the 2000-2019 average of -10.9.

- Markets will pay more attention to tomorrow’s July flash PMIs for a better gauge of broader economic conditions.

- A reminder that Q2 flash GDP for member states and the Eurozone as a whole are due next Tuesday and Wednesday. Bloomberg consensus currently places Eurozone GDP at -0.1% Q/Q, notably below the ECB’s +0.2% projection in the June MPR.

- For consumption, analysts pencil in a 1.5% Y/Y reading (vs 1.4% prior), with the ECB projecting a 0.2% Q/Q sequential print.

GBP: GBP/USD Edges to New Daily High, But Ranges Contained

Jul-23 14:23

GBP briefly edges to a new daily high as it benefits from the fade in the USD and US equities in the 40 minutes following the opening bell - with FX futures volumes picking up to suit the modest pick-up in price action.

- The latest price action has the USD on the backfoot, but the ranges really are contained here - the USD Index is yet to test yesterday's 97.305 lows, and a further wave of greenback sales will be needed to extend the losing streak posted off the mid-July highs.

- With today's NY cut passed, markets keep an eye on the post-ECB expiry pipeline: Even with the fade off highs in EUR/USD, the options interest remains lower for the balance of the week. Over $10bln options notional rolls off between 1.1620-65 into the Thursday, Friday NY cuts - the bulk of which expires just after the ECB press conference on Thursday - which could help contain rallies in spot over the next few days.