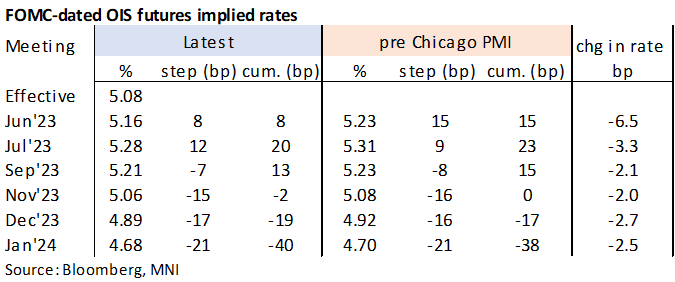

STIR: June FOMC Pricing Bears The Brunt Of Skip Rhetoric

May-31 19:37

- The combination of a sizeable downside miss for the MNI Chicago PMI, higher than expected JOLTS job openings and then Jefferson (voter) and Harker (’23 voter) supporting skipping a June hike has seen decent swings in Fed rate expectations.

- The latter weighed most heavily, especially for June OIS pricing with most of the day's 7.5bp decline coming after Jefferson/Harker, to leave just +8bp priced, whilst it no longer fully prices a hike come July with +20bp (-5.5bps on the day).

- Aside from that particularly heavy decline in June pricing, subsequent meeting expectations have seen a slightly larger retracement but are still 2-3bps lower than pre-PMI levels for down -5.5-6.5bps on the day after earlier spillover from softer European core inflation and China PMIs.

- Tomorrow sees the last day before the media blackout starts Fri midnight, currently with just a repeat appearance from Harker scheduled.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Curves Off Deeper Inversion

May-01 19:00

- Intermediate to long-end Treasury futures continue to gradually extend session lows, while yield curves bounce off deeper inversion after midday 2Y futures Block buy: 2s10s currently +1.978 at -56.670 vs. -64.490 low.

- This morning's data underscores a likely 25bp rate hike from the FOMC on Wednesday: April ISM Prices Paid climbs to 53.2, well over expected 49.0; S&P manufacturing PMI came out slightly lower than expected: 50.2 vs. 50.4 est, but gaining nonetheless vs. 49.2 in March.

- We'd caution this is a volatile series that tends to track commodity prices as much as anything - so while important, it partly reflects a bounce from the sharp drop in commodity prices last year (Prices Paid bottomed at 39.4 in Dec when the 6-month % change in raw industrials and oil prices were dropping double digits - see chart). Though clearly, we're past the lows.

- Otherwise, US markets remain generally quiet, light volumes with much of Europe out for May Day bank holiday, TYM3 just over 750k at the moment.

US STOCKS: Paring Gains in Late Trade

May-01 18:44

- Stocks have trimmed second half gains, trading mildly weaker at the moment, still holding to a narrow session range. Currently, DJIA down 20.79 points (-0.06%) at 34076.09; - S&P E-Mini Future up 0.75 points (0.02%) at 4189 and Nasdaq down 15.3 points (-0.1%) at 12211.14.

- SPX futures drifted above key resistance of 4198.25 High Apr 18 earlier to 4204.00 high before retreating. A clear break of this level would confirm a resumption of the uptrend that started Mar 13 and open 4244.00, the Feb 2 high.

- On the downside, key short-term support has been defined at 4068.75, the Apr 26 low. A break would be bearish.

- Meanwhile, quarterly earnings cycle resumes after the close, salient stocks include: Stryker Corp, Community Health Systems, Invitation Homes Inc, Vornado Realty Trust, Transocean Ltd, ZoomInfo Technologies Inc, Arista Networks Inc, Avis Budget , Group Inc, SBA Communications Corp, MGM Resorts International, Credit Acceptance Corp and Diamondback Energy Inc.

US TSYS: Late SOFR/Treasury Option Roundup, Hedging a 25Bp Hike

May-01 18:30

Light option volumes was due to most of Europe out for May-Day bank holiday Monday. Early SOFR Call structure buying ebbed in the second half while Jun'23 SOFR options saw a pick-up in limited downside put condors as a jump over 50.0 to 53.2 in April ISM Mfg PMI data, underscoring a likely 25bp rate hike this Wednesday.

- SOFR Options:

- Block, +10,000 SFRM3 94.68/94.75/94.81/94.87 put condors, 0.75 ref 94.855

- +25,000 SFRM3 94.68/94.75/94.81/94.87 put condors, 0.5 ref 94.855 to -.86

- 2,000 SFRM3 94.93/95.12 call spds ref 94.89

- Block, +10,000 SFRZ3 96.50/97.50 call spds, 13.0 vs. 95.50/0.10%

- +2,000 SFRM3 97.00/97.12/99.50/99.62 call condors

- 1,000 SFRM3 94.75/95.00/95.12 broken put flys, ref 94.915

- 2,000 SFRN3 94.50/94.93/95.00/95.18 put condors ref 95.155

- Treasury Options:

- +4,000 USM 128 puts, 54 ref 130-02

- 2,100 TYM3 112.25 puts, 8 ref 114-30 to -30.5

- 2,500 FVM3 110.5/111.25 call spds ref 109-22 to -22.5

- 2,000 FVM3 112/113 call spds, 5.5 ref 109-25.5

- 3,000 TYM3 115.75/116.5 call spds ref 115-12