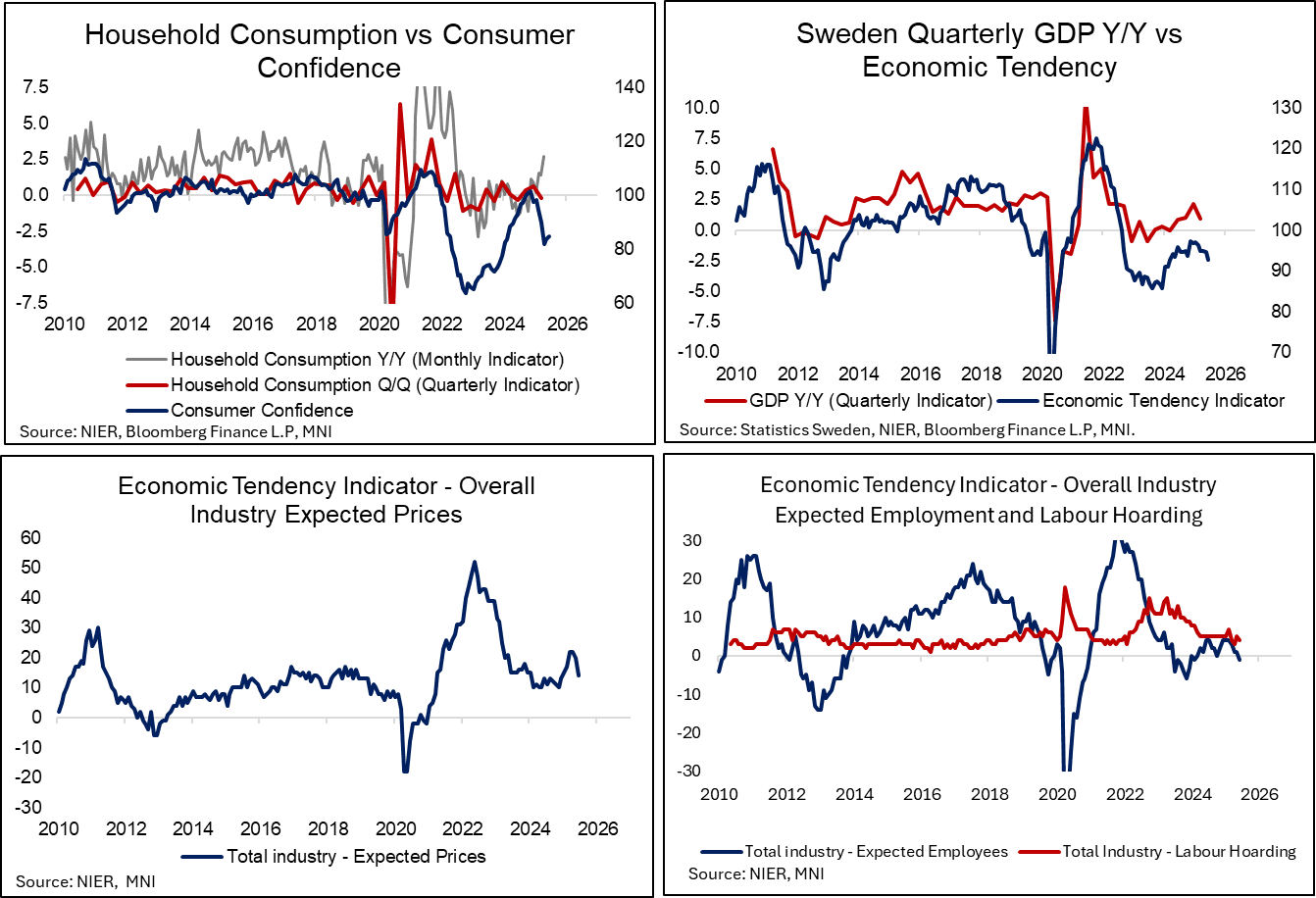

SWEDEN: June Business Sentiment Weak; Concerning To Riksbank

The June Economic Tendency Indicator (ETI) will be concerning to the Riksbank, and support market pricing for one more cut this year. The decline in business sentiment, alongside very soft (albeit slightly improving) consumer sentiment encapsulates the Riksbank’s June MPR dovish scenario, which if realised could imply a policy rate as low as 1% . This scenario assumed that “the uncertainty regarding the trade conflict and the security policy situation will gradually lead to increasingly large falls in confidence among households and companies”, weighing on growth in Q3.

- At the June press conference, Governor Thedeen said the Riksbank’s dovish scenario was a “more severe” version of what is already being observed. Today’s survey result does little push back on this assessment.

- The headline ETI eased to 92.8 (vs 94.5 prior), the joint lowest since March 2024. Business sentiment fell sharply to 94.8 (vs 98.4 prior), led by retail (98.1 vs 103.3 prior) and services (92.9 vs 95.5 prior).

- The fall in retail was the largest on record, with the largest negative contribution coming from the inventory component. Services firms are “more negative than usual, both regarding demand developments over the past three months and their expectations for future demand”. Meanwhile, “more manufacturing firms than in May reported a decrease in production volumes over the past three months due to changed tariffs or the uncertainty surrounding tariff issues”.

- This weakness saw the expected employment indicator turn negative for the first time since February.

- Total expected prices pulled back to 14 (vs 20 prior), led by manufacturing and retail. Services expected prices remain sticky at 19.

- Consumer sentiment edged up to 84.6 (vs 83.6 prior), but remains very weak. It remains somewhat inconsistent with hard consumption/retail sales data. Riksbank Deputy Governor Bunge acknowledged this discrepancy in yesterday's June minutes.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

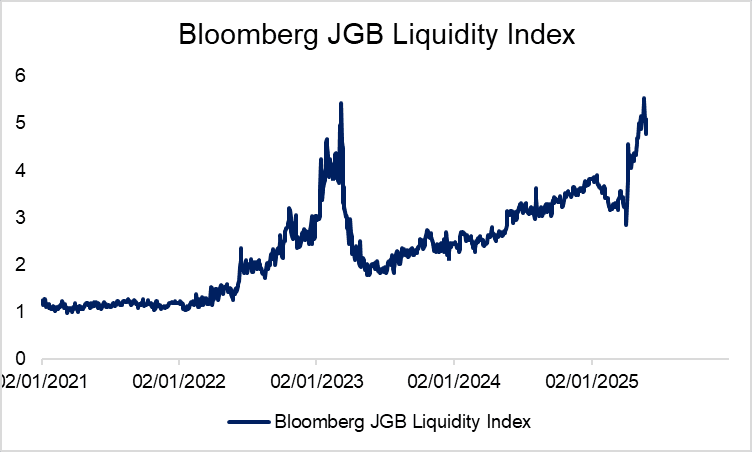

JGBS: Mid-June In Focus For MOF Selling and BOJ Buying Tweaks

- These factors have come against a backdrop of reduced liquidity in the Japanese bond market, especially at the long-end. Bloomberg’s JGB liquidity index (which isn’t a perfect measure of this given it includes all bonds with a maturity greater than one year) has fallen from last week’s highs but remains elevated, indicating worse liquidity conditions.

- Reuters notes that the MOF will make a decision on its issuance plan around mid- to-late June, after holding discussions with market participants.

- This will align closely with the BOJ’s June 17 meeting, where the bank will review its bond purchase reduction plan. The BOJ is currently reducing bond purchases by JPY400 billion per quarter through March 2026. A former BOJ official recently told MNI that the BOJ should clearly communicate the pace at which it plans to reduce its JGB holdings, including both purchases and expected redemptions, to help maintain bond market stability.

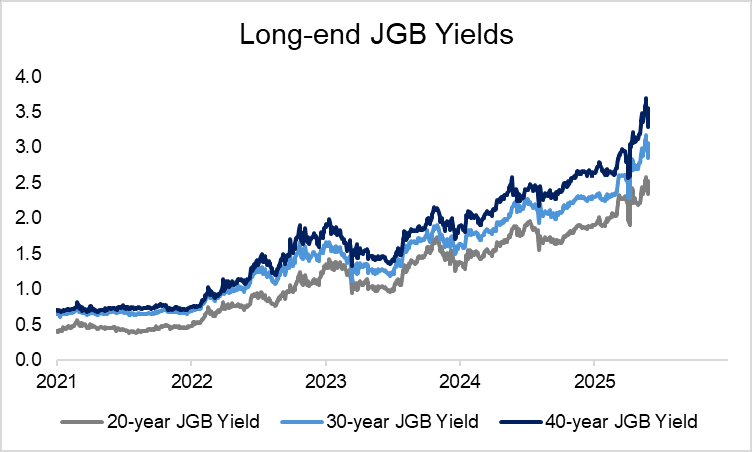

JGBS: Sharp Reprieve For Long-end JGBs On MOF Sources; Focus On Auction Demand

40-year JGB yields are down 24.5bps to 3.312% today, with the curve sharply bull flatter, after Reuters sources suggested the MOF will consider skewing the composition of its current issuance programme away from super-long-end instruments. That’s the largest one-day decline in 40-year yields since Bloomberg began tracking the data in February 2008 (and the 2nd largest absolute change in yields). 40-year yields are now almost 40bps below last Friday’s 3.697% high, with short-positioning likely exacerbating the last few days’ relief rally. However, focus remains intently on tomorrow’s 40-year auction.

- There have been several factors contributing to the sharp sell-off in (particularly long-end) JGBs over the last two months.

- (i) Signs of waning structural demand from domestic counterparties, such as the life insurance sector. Weak auction results (e.g last week’s 20-year auction) may reflect such dynamics.

- (ii) Concerns around less BOJ-led support for government bonds in the coming quarters.

- (iii) Fiscal concerns, particularly with the upper house election due in July. This morning (per BBG), a government advisory panel called for enhanced domestic fiscal prudence: “We must manage finances with a heightened sense of urgency to prevent rising debt costs from crowding out essential policy spending”.

- (iv) Global curve steepening on a wider global assessment of long-dated issuance in a structurally higher inflation environment with heightened policy uncertainty. Moves in US Treasuries have embodied this dynamic, with erratic tariff policy changes and still-expansionary fiscal policy forcing investors to demand a higher term premium for long-end US debt. The UK DMO has already skewed its issuance plans away from long-end debt due to “declining strength” of demand for these instruments.

MONTH-END EXTENSIONS: Expected Extensions

- As expected The Rolls are in full action in early trade, over 50% of the front Month Volume in Gilt is spread related, while in TYM5 it is running in the circa 69%.

- Bond Traders will also be focussed on Month End, although nothing really major there.

MONTH END EXTENSION:

Bloomberg Bonds:

- US Tsys: +0.11yr (decent).

- EU Govies: +0.07yr (average).

- UK Govies: -0.01yr (non event).

MS Bonds:

- US Tsys: +0.08yr (average).

- EU Govies: +0.07yr (average).

- UK Govies: -0.03yr (non event).