FRANCE DATA: Jun Prelim Inflation Preview: Y/Y Deceleration Seen Continuing

Jun-29 15:28

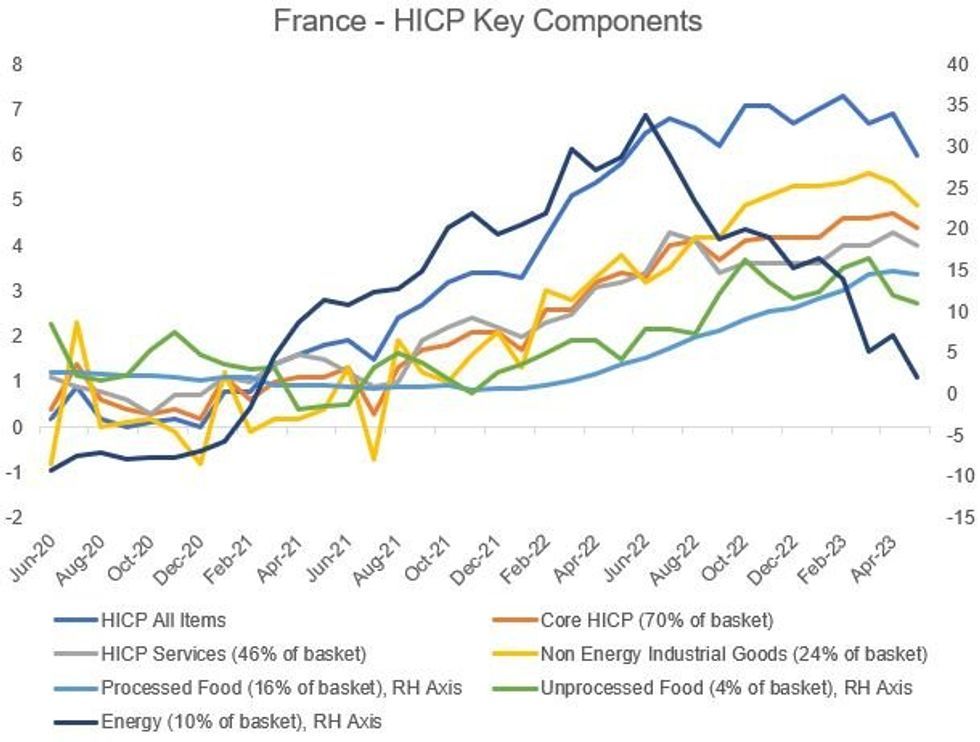

France (20% of EZ HICP) – 0745UK/0845CET Fri 30 Jun. Consensus:

- HICP: 5.4% Y/Y (6.0% prior) / 0.2% M/M (-0.1% prior)

- CPI: 4.6% Y/Y (5.1% prior) / 0.2% M/M (-0.1% prior)

- Headline Y/Y seen weaker largely on energy/base effects, though M/M pressures are set to rebound from a soft May.

- Last month's flash data surprised to the downside (HICP fell -0.1% m/m (vs +0.3% expected), whilst cooling by 0.9pp to +6.0% y/y vs +6.4% expected.

- While the flash estimate doesn't include a core reading, last month's showed a deceleration in both services and manufactured goods, which correctly flagged the softer core CPI in the final print (+5.8%, after +6.3% in April; HICP core was 4.4% after 4.7%).

- There is no analyst survey for core but the key dynamic eyed will likely be services (46% of the basket - was 4% Y/Y in HICP last time, after 4.3% in April, and in line with 4% in Mar and Feb).

Some sell-side analyst outlooks:

- JPMorgan: HICP: 5.6%. CPI 0.2% M/M, 4.6% Y/Y

- BofA: 5.6% Y/Y HICP headline (0.5% M/M), CPI 0.6% and YOY 4.9%

- Goldman Sachs: 5.4% Y/Y on -2.7% Y/Y energy driven by base effects, petrol prices. Processed food 16% Y/Y, unprocessed 8.1%. Core 4.6% Y/Y, unwinding Apr/May sequential volatility and back in line with March's pace.

- Nomura: 5.5%

- Citi: Not for this report but notes potential upside in Jul headline print as French regulated energy tariffs come to an end.

% Y/Y ChangeSource: Insee, Eurostat, MNI

% Y/Y ChangeSource: Insee, Eurostat, MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: 1Y Midcurve Euribor Call Fly

May-30 15:16

- +4,000 short Sep'23 Euribor 96.87/97.12/97.37 call flys, 3.25

US TSYS: US TSY 13W AUCTION: NON-COMP BIDS $1.739 BLN FROM $63.000 BLN TOTAL

May-30 15:15

- US TSY 13W AUCTION: NON-COMP BIDS $1.739 BLN FROM $63.000 BLN TOTAL

US TSYS: US TSY 26W AUCTION: NON-COMP BIDS $1.741 BLN FROM $56.000 BLN TOTAL

May-30 15:15

- US TSY 26W AUCTION: NON-COMP BIDS $1.741 BLN FROM $56.000 BLN TOTAL