EM ASIA CREDIT: JD.com: S&P likes what it sees

(JD, A3/A-pos/NR)

"X-S&PGRBulletin:JD Can Stomach Volatility For Stronger Business " - BBG

S&P guides EBITDA estimates lower, sees future benefits, neutral read.

S&P provided an update after close yesterday, in which it recognised that the company will likely see reduced profits as it invests in new businesses, such as food delivery, but believes this will ultimately strengthen the company's business profile.

This comes on the back of disappointing 3Q results last week, in which EBITDA dropped 84% YoY to RMB2.5bn, and materially below consensus (RMB3.4bn). The S&P comment isn't a rating action per se, but they do note that EBITDA may now fall 47% YoY in 2025 versus a previous estimate of down 28%.

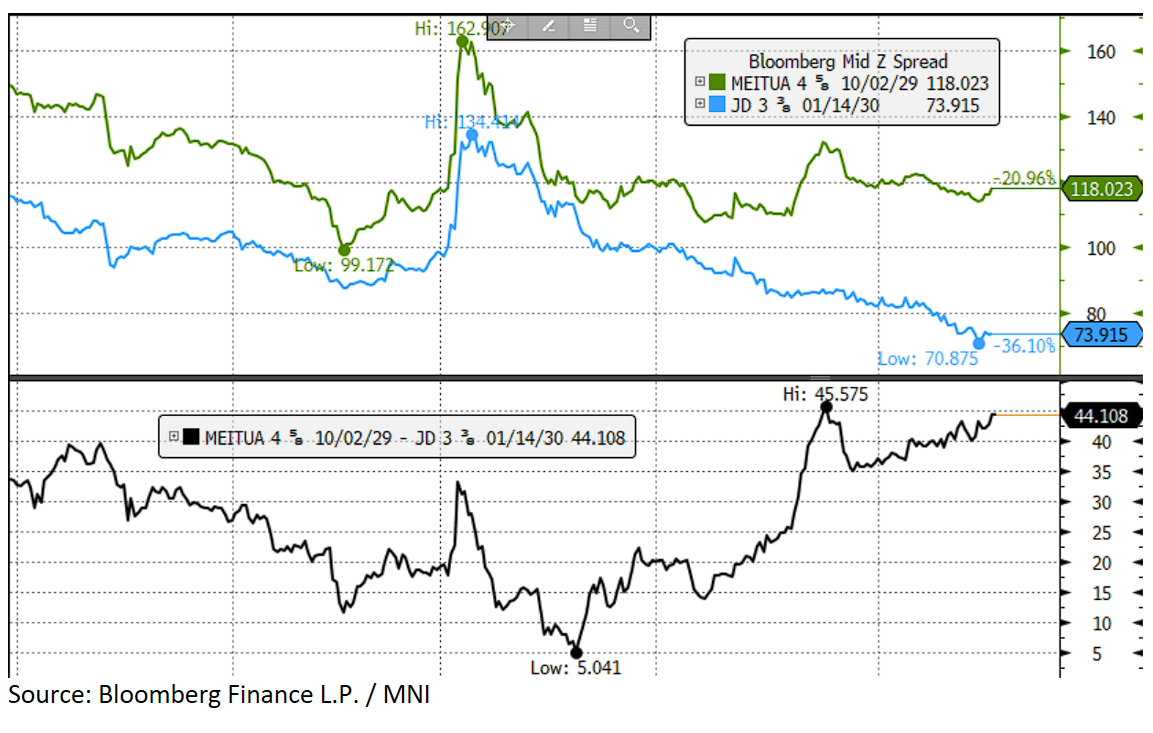

The current positive outlook does seem at risk in our view. In terms of valuations, we note that the z-spread differential between the JD.com USD 30s and the Meituan USD 29s is back to the wides and the JD 30s remain at the year-to-date tights.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: FX OPTION EXPIRY

Of note:

USDJPY ~2bn at 150.00/150.05.

EURUSD ~1bn at 1.1700 (tue).

NZDUSD 1.1bn at 0.5700 (wed).

AUDUSD 1.49bn at 0.6450 (fri).

- EURUSD: 1.1645 (665mln), 1.1650 (331mln), 1.1670 (211mln), 1.1700 (346mln), 1.1705 (206mln), 1.1715 (740mln).

- USDJPY: 150.00 (1.28bn), 150.05 (823mln), 150.25 (600mln), 150.50 (355mln), 151.00 (779mln), 151.70 (1.1bn).

- USDCAD: 1.4000 (718mln).

- AUDUSD: 0.6500 (340mln).

- AUDNZD: 1.1325 (400mln).

EURIBOR OPTIONS: Call Fly Buyer

ERU6 97.93/98.06/98.18c fly, bought for 1 in 2k.

BUNDS: Block trade

Bund Block trade, suggest seller:

- RXZ5 2.4k at 129.90.