ASIA STOCKS: Japan Effect Sees Regional Gains, NIFTY 50 Strong Uptrend Building

Feb-10 04:37

- Stocks in Japan continue to lead today following the election result and optimism over the economy. Investors are pricing in the PMs "Sanaenomics" agenda, which includes a ¥21 trillion stimulus package, potential tax relief (suspending the 8% sales tax on food), and increased defense and AI spending. The ongoing earnings season has exceeded expectations. Heavyweights like SoftBank Group saw shares spike over 10% today after upgrading full-year forecasts. Other major gainers include Furukawa Electric (+22%) and NEC, which announced a significant share buyback. This momentum is supported by structural reforms that have raised Japan's average Return on Equity expectations significantly. This sees the NKY up +2.3% today and nearly 7% in the last three trading days.

- The Japan effect lifted regional bourses with all major indexes up . China was more subdued to modest gains as markets start to wind down ahead of the upcoming holidays and the KOSPI rose by just +0.10%.

- Despite news that FTSE Russell are following the lead by MSCI, the Jakarta Composite brushed off these further concerns with a second day of gains, up +1.1% today.

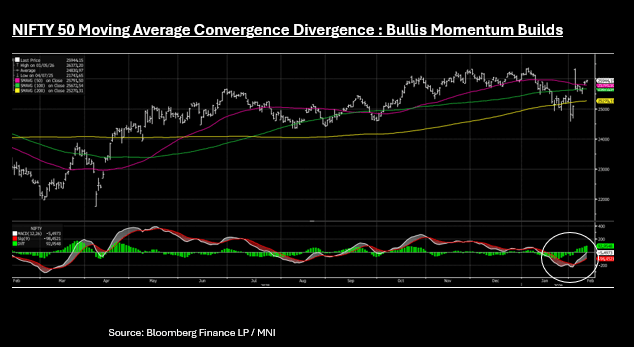

- India's NIFTY 50 is +0.30% and continues to deliver solid daily gains. Since the announcement of the US trade deal, the NIFTY 50 has gained almost 5% to be near 26,000 again. The bullish momentum is strong for the NIFTY 50 according to the MACD analysis. The short term exponential average is significantly longer than the long term suggesting a strong uptrend is building for the index.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

Jan-10 22:45

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Jan-09 23:36

Test Test TEST

MNI: MNI Test, Please Ignore

Jan-09 23:30

Test, ignore