EM CEEMEA CREDIT: Ivanhoe Mines: prod’n guidance update

Sep-18 10:47

(IVN; NR/B/B)

• Supportive read, one to watch for. Neutral for credit.

• Further to previous update last August, Co. expects to have updated ’26 and ’27 guidance as the de-watering process advances, with indication of stage progress expected for end of Nov.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - USDJPY Support Remains Exposed

Aug-19 10:47

- In FX, EURUSD continues to trade at its latest highs and a short-term bullish outlook is intact. Moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. A continuation higher would expose key resistance and the bull trigger at 1.1829, the Jul 1 high. Clearance of this level would resume the uptrend. Support to watch lies at 1.1586, the 50-day EMA.

- GBPUSD has pulled back from its latest highs but a bull cycle remains intact. Recent gains resulted in a breach of resistance at 1.3589, the Jul 24 high. Sights are on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1. A break of this retracement would strengthen the short-term bull theme. Initial firm support to watch lies at 1.3448, the 50-day EMA.

- USDJPY is in consolidation mode. A bearish threat remains present and the pair is trading closer to its recent lows. Sights are on support at 145.86, the Jul 24 low. Clearance of this level would highlight a stronger reversal and strengthen the bearish engulfing signal from Aug 1. This would open 144.63, a trendline drawn from the Apr 22 low. Initial firm resistance to watch is 148.52, the Aug 12 high. A breach of it would be viewed as a S/T bull signal.

OPTIONS: Expiries for Aug19 NY cut 1000ET (Source DTCC)

Aug-19 10:32

- EUR/USD: $1.1600(E731mln), $1.1620-25(E2.3bln), $1.1650-65(E682mln), $1.1700(E1.3bln)

- USD/JPY: Y148.30-35($709mln)

- AUD/USD: $0.6515(A$745mln)

- USD/CAD: C$1.3750-70($646mln)

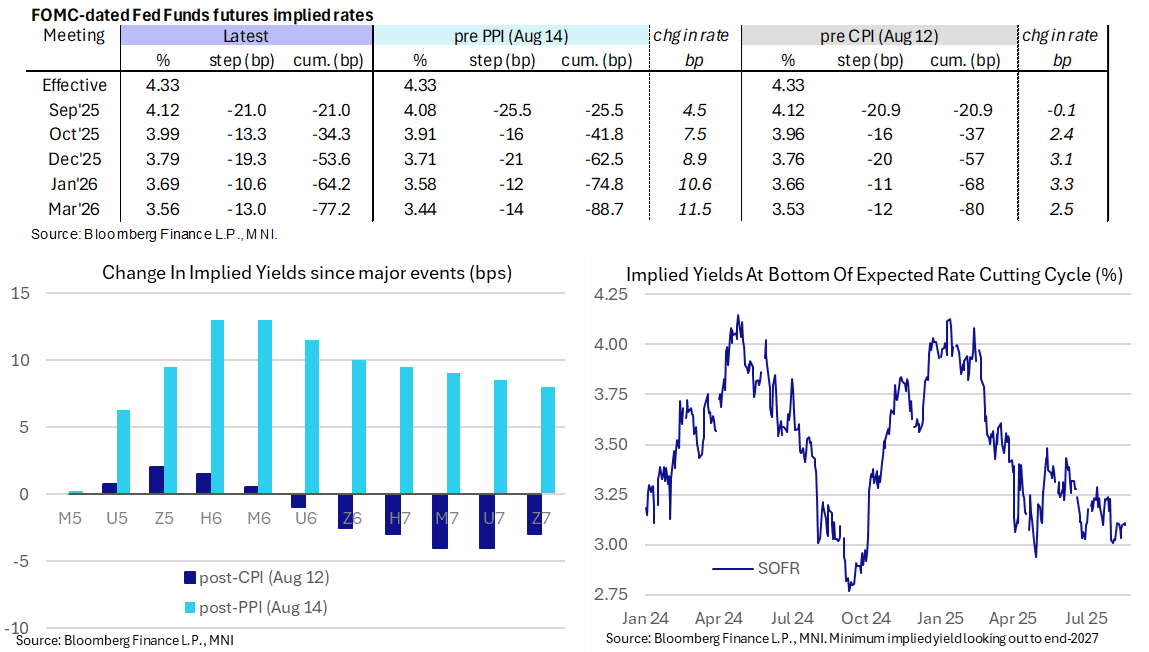

STIR: Sept Fed Cut Still No Longer Fully Locked In, A Dovish Bowman Ahead

Aug-19 10:32

- Fed Funds implied rates are unchanged on the day, with 21bp of cuts priced for next month’s FOMC meeting.

- Cumulative cuts from 4.33% effective: 21bp Sep, 34.5bp Oct, 53.5bp Dec, 64bp Jan and 77bp Mar.

- The SOFR implied terminal yield of 3.11% (SFRH7) is essentially unchanged from the past two closes, holding the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Fed VC Supervision Bowman (permanent voter, dove) speaks on Bloomberg TV at 1000ET before at a Blockchain Symposium at 1410ET (text only), with greater scope for market moving comments at the former. We suspect it might be hard to generate a dovish reaction though unless she canvasses larger cuts, something other FOMC colleagues have pushed back on.

- These will be her first remarks since last week’s mixed inflation data. She said on Aug 9 that she favors three cuts this year (unsurprising having dissented in July) and saw recent labor data as reinforcing this view.

- Tomorrow then sees the FOMC minutes before Powell’s Jackson Hole address on Friday. However, when it comes to Sept cut prospects, the August payrolls and CPI releases plus QCEW details (for preliminary payroll benchmark revision estimates) are all still to come before the next FOMC decision on Sep 17.

Trending Top

Mar-27 20:13