IRAN: Iran Has Not Reached Final Decision On An Agreement

"IRAN FOREIGN MINISTRY SPOKESPERSON SAYS QATAR AND PAKISTAN ACTIVE AS MEDIATORS BUT U.S. ACTIONS AFF...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

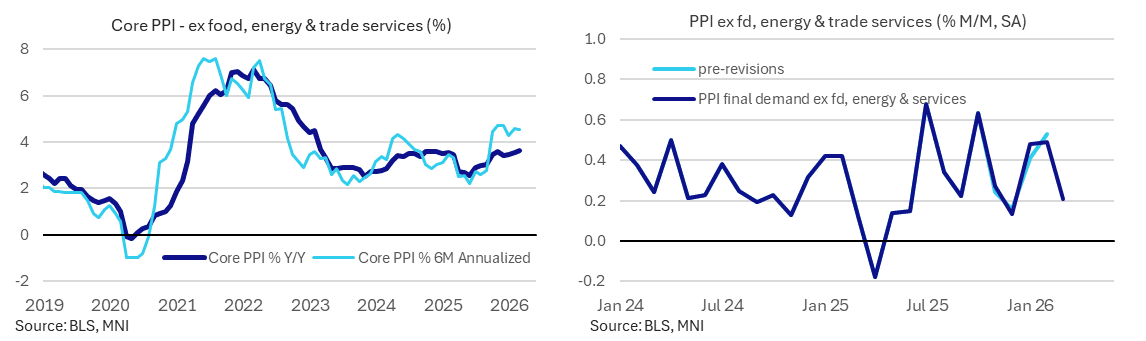

US PREVIEW: Core PPI Pipeline Pressures Seen Picking Up In April

Wednesday's PPI report for April (0830ET) will offer a latest update on pipeline price pressures refine estimates for core PCE estimates. Consensus is for a 0.5% M/M rise in overall final demand PPI, the same as March, pushing the Y/Y reading to a new cycle high 4.8% Y/Y (4.0% prior); core (ex-food/energy/trade) M/M is expected to tick up to 0.3% M/M after 0.1% in March, likewise leaving the Y/Y with a 4-handle for the first time since early 2023 (4.2%, vs 3.6% prior).

- Analyst estimates for core PCE are centered around 0.31% M/M for April albeit with still a reasonably wide range of 0.26-0.36%, but the common theme is that PCE is seen softer than CPI (0.38% M/M core) due to various measurement and weighting differences.

- Softer-than-anticipated airfares and various medical care services in CPI do not feed into PCE, so will instead be eyed in the PPI report (domestic airfares printed 2.75% M/M in March's PPI; health insurance 0.46% M/M; healthcare services 0.15% M/M), with auto insurance also potentially getting some attention (0.1% M/M in March).

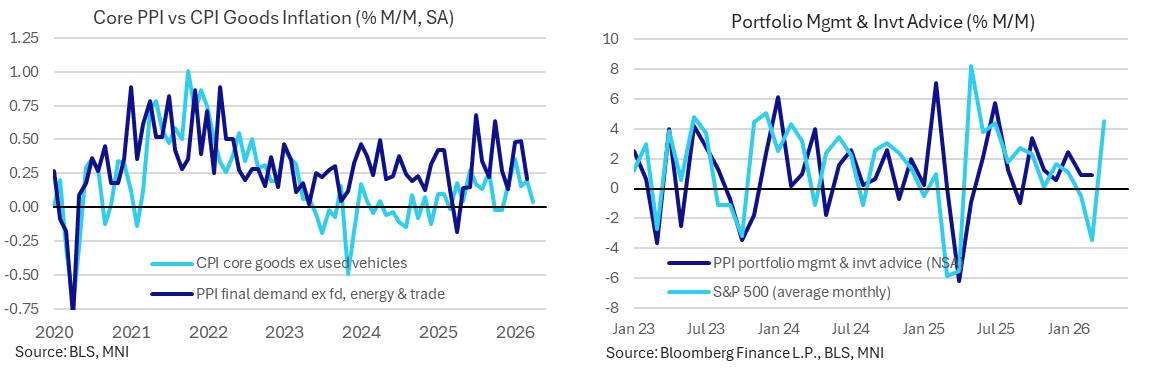

- The other key column feeding into PCE is portfolio management and investment advice PPI which after printing +0.9% M/M for 2 consecutive months should be in negative territory in April (though estimates are extremely wide, we've seen from around flat to -5% M/M) corresponding to a drop in equities in March, though of course this impact will reverse in May's PPI report.

- As for PPI itself, there will of course be significant attention on early warning signs of MidEast-related price pressures that could apply pressure on consumer inflation metrics in the coming months.

- Industry surveys, particularly ISM Manufacturing, showed significant increases to multi-year highs in Prices Paid in April.

- Final demand core goods and final demand services inflation have actually decelerated sequentially the last 2 months (March, respectively: 0.2% M/M and 0.0%), so it would be somewhat surprising not to see some basing here.

- PPI Food dropped 0.3% M/M in March (after an outsized 2.4% rise in Feb) but is likely to rebound, while energy PPI is likewise set to pick up sharply on rises in various columns including gasoline (though natgas looks to have been more muted).

US TSYS: Yields Climb Higher w/ Crude, US$, Warsh Confirmed Board of Governors

- Treasuries look to finish at/near late session lows, largely driven by crude prices rising to late session highs: June WTI trading around $102.50/bb as the market weighs the risk of escalation in the Iran war with little sign of an immediate resolution.

- The fourth consecutive tail for the 10Y note sale spurred additional selling after the $42B 10Y note auction (91282CQQ7) drew 4.468% high yield vs. 4.464% WI; 2.40x bid-to-cover vs. 2.43x prior.

- Upside in Headline and Core was driven by services, with both supercore (0.45% M/M vs 0.29% MNI Median, 0.18% prior) and primary rents (0.55%, vs 0.40% MNI median, 0.19% prior) notably higher than expected, joined by lodging (2.4% vs 0.0% MNI median, 0.24% prior) and offset by a slight downside miss in airfares, flat medical care services prices and negative communications services.

- Following the April CPI report release earlier Tuesday, Chicago Fed President Goolsbee (2027 FOMC voter) expressed concern over the recent pickup in services inflation, and has made it clear that he's no longer as worried about the labor market side of the dual mandate. He maintains his medium-term optimism that rates can come down a "fair amount", but ties that squarely into inflation progress.

- The Senate confirmed Kevin Warsh to the Federal Reserve's Board of Governors on Tuesday, a crucial step in President Donald Trump's push to make Warsh the central bank's leader after months of uncertainty due to a criminal probe of outgoing chief Jerome Powell.

- MNI LOOK AHEAD: Wednesday Data Calendar: PPI, Fed Speakers, 30Y Bond Sale

USDCAD TECHS: Tops 50-day EMA

- RES 4: 1.4015 High Dec 2 ‘25

- RES 3: 1.3985 76.4% retracement of the Nov 5 ‘25 - Jan 30 bear leg

- RES 2: 1.3878/3967 High Apr 13 / High Mar 31 and the bull trigger

- RES 1: 1.3725 50-day EMA

- PRICE: 1.3713 @ 16:38 BST May 12

- SUP 1: 1.3550/26 Low May 1 / Low Mar 9

- SUP 2: 1.3507 1.0% 10-dma envelope

- SUP 3: 1.3482 Low Jan 30 and key support

- SUP 4: 1.3420 Low Sep 25

USDCAD is building on recent gains. Despite the latest gains, the trend condition remains bearish and the latest recovery appears corrective. Resistance is seen at 1.3711, the 50-day EMA, has been pierced. A clear break of this average is required to signal a possible S/T reversal. A resumption of weakness would pave the way for a move towards 1.3526, the Mar 9 low and the next key support. A clear break of this level would open 1.3482, the Jan 30 low.