JAPAN: International Investors Bought Record Amount Of Japanese Equities Last Week

Weekly international security flow data from the Japanese MoF reveals that Japanese investors shed international bonds for a second consecutive week during the week ending 7 April, the first instance of back-to-back weeks of net sales observed since January. Still, the 4-week rolling sum of the measures remains comfortably in positive territory given the sizable rounds of net purchases deployed in the weeks prior to the current run.

- Japanese investors were also net buyers of international equities for a second consecutive week, although the net purchases were paltry.

- International investors were net buyers of Japanese bonds for the third week in four but got nowhere near challenging the record weekly net purchase levels observed in March.

- Finally, international investors deployed the largest round of net weekly purchases of Japanese equities on record last week.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -788.8 | -483.4 | 3248.8 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 28.2 | 390.3 | 494.5 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 1311.1 | 944.1 | 4674.6 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 2368.9 | 62.2 | 54.1 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M3) Pre-BoJ Short-Setting Crushed in Sharp Rally

- RES 3: 151.13 - High Mar 3

- RES 2: 149.75/150.81 - High Nov 11 / High Aug 5

- RES 1: 148.99 High Mar 13

- PRICE: 148.75 @ 15:48 GMT Mar 13

- SUP 1: 144.93 - Low Mar 9

- SUP 2: 144.15 - Low Jan 13

- SUP 3: 143.86 - 1.0% 10-dma envelope

JGBs rallied sharply into the Friday close and added to those gains throughout Monday trade. The unchanged BoJ decision and a phase of global rate re-pricing has boosted bond prices, with recent weakness wholly reversed. The Mar02 high at 147.07 has been broken, working against the over-arching downtrend. Any resumption of weakness would expose next support at the Jan 13 low on the continuation contract at 144.15 for direction.

JGBS: Futures Surge On Historic Global FI Rally

JGB futures continued to surge overnight, with the impulse derived from a historic richening in core global FI markets and exiting of shorts extending the move. The contract finished comfortably off of best levels but was still over 190 ticks firmer on the day, after hitting the highest levels seen since late November in the process. Expect this to reverberate in early Tokyo trade. This comes after 10-Year JGB yields pulled further away from the BoJ’s YCC cap on Monday. The BoJ has some more breathing room, at least for now, thanks to the SVB failure.

- Local headline flow has been light, although the latest North Korean missile tests (seemingly two short-range ballistic missiles) will generate some interest.

- 5-Year JGB supply is due today, providing the headline event of the local docket. That will leave feedthrough from Tuesday’s situation at the forefront for most of the session.

- Technically, if bulls force a breach of the overnight high in JGB futures (148.99) focus will turn to the November 11 high (149.75), with the SVB situation amplifying the pressure on short positioning and threatening a meaningful break of the technical downtrend.

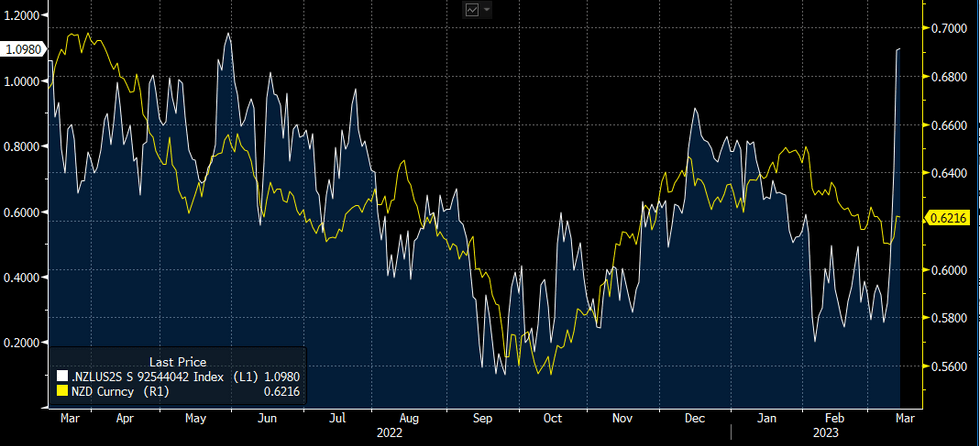

NZD: Rising Rate Differentials Underpin NZD/USD Rally

NZD/USD has risen over 2% in recent sessions. The Fed rate hike cycle repricing, in the wake of the collapse of SVB and Signature Bank, has seen the 2-Year Rate Differentials observed via swap spreads widen by ~83bps to levels last seen in late May 2022.

- NZD/USD found support below $0.61 firming as much as 3% from 2023 lows before moderating gains, this comes as rates markets re-price expectations for the Fed rate hiking cycle.

- Fed dated OIS has ~30bps of hikes priced into what is left of the hiking cycle, with ~15bps hike priced for March. The terminal rate is now seen at ~4.8% in May. There are over 90 bps of cuts priced in before the end of 2023.

- 2-Year Rate Differentials now sit at +109bps, with 2-Year Swap spread now the widest since late May 2022 when the NZD/USD was ~3 cents higher.

- Bulls look to break the 200-day EMA at $0.6265 having met resistance ahead of the level yesterday. Bears first look to break 2023 lows at $0.6085.

- Today's US CPI print presents the next macro risk event.

Fig 1: NZ US 2 year Swap Spreads v NZD/USD Daily Spot

Source: MNI/Bloomberg