INDIA: INR Swaps Continue to Price Out Rate Cuts

Nov-19 02:05

- With just over a two weeks to go before the next RBI meeting, swaps and bond signals are no longer suggesting that the last meeting for the year will see a cut.

- The swaps market had 25bps of cuts over the next month and 29bps over the next two at the beginning only a fortnight ago, whilst the MIPR function on Bloomberg has 29 cuts priced in over the next month.

- Today that it remains the 1 month forward has 6bps of cuts and the cumulative 3 months just 10bps.

- The next focus for markets in India will be November PMIs. PMIs have remained seemingly bulletproof with the Composite over 60 for the last five months, and seemingly no reason for that trend to change.

- If swaps pricing is correct, what was a relatively shallow rate cutting cycle is complete or near complete. There remains a c. 70% chance of one cut in Q2 next year priced in.

- The market pricing is somewhat at odds with the MPC who at their last meeting where rates were maintained at 5.50%, also maintained their neutral stance. The market is likely hinging on the fact that 2 of the 6 members voted for an accommodative stance.

- At the time of the last meeting on Oct 1, USDINR closed at 88.69 only to rally into the back end of October. However in recent sessions this has given back and it is back only moderately below the Oct 1 level today at 88.61. A trade deal is not yet priced into the INR yet, with local media reports suggesting tariffs to be reduced to around 25% initially, likely then back to 15% after further negotiations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: AU-US 10Y Diff Moves Away From Range’s Upper Bound

Oct-20 01:55

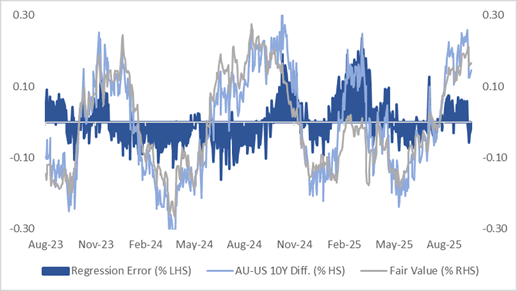

Cash ACGBs are 5-6bps cheaper on the day, but with the AU-US 10-year yield differential.

- At +14bps, the differential has narrowed from recent wides but remains in the top half of the ±30bps range that has prevailed since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is -2bps versus fair value.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has increased around 75bps since June to be around the same level as October 2024.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

CHINA: House Price Decline a Not So Gentle Reminder ahead of 4th Plenum

Oct-20 01:43

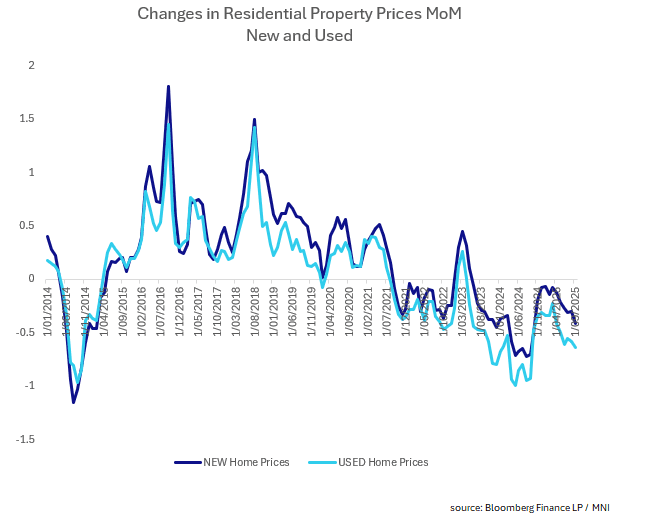

- China's New and Used Home prices declines continued in September, picking up pace from the month prior.

- New home prices declined -0.41% (from -0.30% in August) and have declined month on month since May 2023. New home prices -2.66% YoY vs -2.95% in Aug.

- September saw Shanghai and Beijing prices up +0.30% and +0.20% respectively with falls in all all other reported markets.

- The cumulative month on month decline is nearing 10% since May yet with estimations of 40-50 million unsold properties, there could be more declines to follow.

- Used home prices fell -0.64% (from -0.58% in August). The last monthly increase in Used Home prices was April 2023 with the cumulative monthly decline now over 16%. Used home prices -5.24% YoY vs -5.51% in Aug.

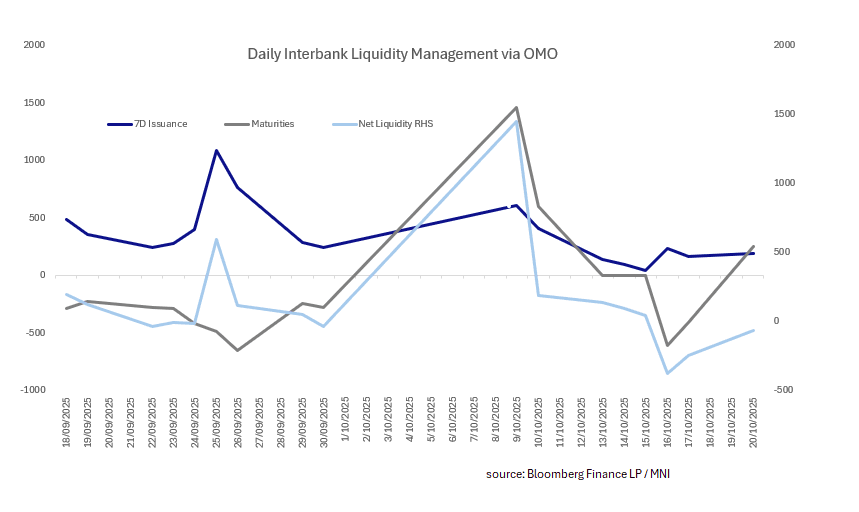

CHINA: Central Bank Withdraws CNY64.8bn via OMO

Oct-20 01:29

- The PBOC issued CNY189bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY253.8bn.

- Net liquidity withdrawal CNY64.8bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.40%.

- The China overnight interbank repo rate is at 1.30%, from the prior close of 1.35%.

- The China 7-day interbank repo rate is at 1.41%, from the prior close of 1.40%.