STIR: Initial PPI Reaction Fades A Little, PCE Readthrough Not As Hawkish

Initial hawkish adjustment in Tsys & Fed pricing starts to pare back. First glance suggests that some of the PCE readthrough is softer than the hawkish headline PPI figures would have suggested, helping explain the tempering of the initial reaction.

- ~24bp of cuts priced into FOMC-dated OIS for September, ~40bp through October and 59.5bp through year-end. That compares to 25.5bp, 42.5bp and 62.5bp ahead of the data.

- SOFR-implied terminal rate pricing 3.04% vs. 3.00% pre-data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCKs: Sep'25 2Y Buy, 10Y Ultra Sale

- Separate Blocks:

- +9,000 TUU5 103-21.38, buy through 103-20.88 post time offer at 0834:00ET, DV01 $340,000

- -4,000 UXYU5 112-22, sell through 112-23 post time bid at 0835:23ET, DV01 $345,000

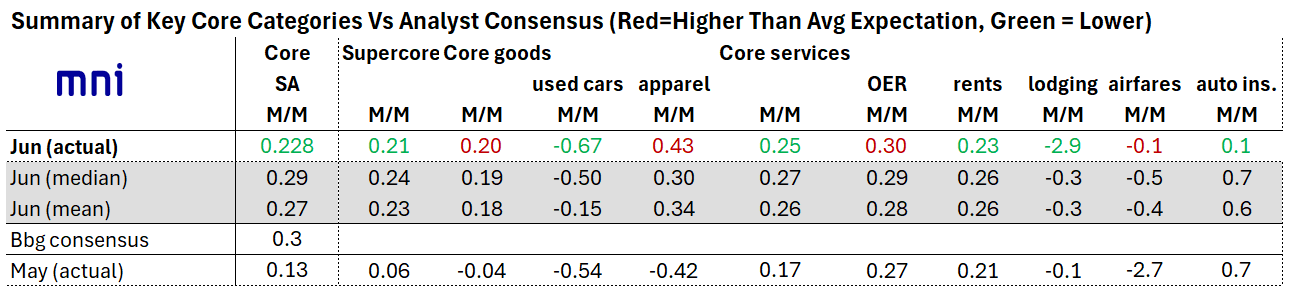

US DATA: Core Services Keep June Inflation On The Cool Side

The softer-than-expected core reading in June (0.23% M/M vs 0.29% MNI median, 0.13% prior) comes with higher core goods prices than expected (0.20% M/M vs 0.19% MNI median, -0.04% prior), but that's outweighed by core services slightly on the light side (0.25% M/M vs 0.27% MNI median, 0.17% prior).

- First on services. As noted, supercore was overall on the soft side at 0.21% (0.24% MNI median, 0.06% prior): lodging prices were significantly softer than expected (-2.9% vs -0.3% median, -0.1% prior), with auto insurance also on the soft side (0.1% vs 0.7% median, 0.7% prior). Airfares were higher than expected (-0.1% vs 0.5% median, -2.7% prior) but this isn't included in PCE; recreation services ticked up to +0.2% M/M from -0.1% (no consensus).

- OER was largely in line (0.30% vs 0.29% median, 0.27% prior), but rents picked up less than expected (0.21% vs 0.26% median).

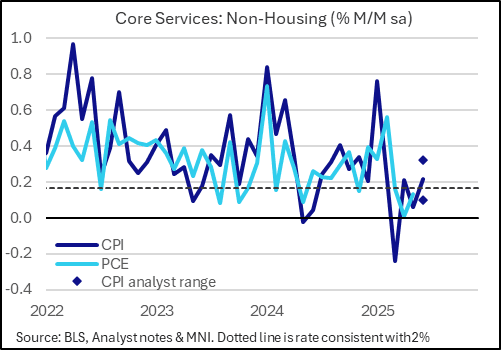

US DATA: CPI Core Services Ex-Housing ("Supercore") - June

Supercore reasonably close to average analyst estimates despite a surprisingly heavy drag from lodging away from home (-2.9% M/M). See the above table for how this lodging line stands out vs expectations.

- Core services excl OER & primary rents ('supercore'): 0.212% M/M after 0.061%. Latest 3mth av of 0.161%

- Core services excl all shelter (i.e. also stripping out lodging): 0.361% M/M after 0.056%. Latest 3mth av of 0.189%

- Limited analyst estimates for ex OER & rents had averaged 0.23% M/M, ranging from 0.10 to 0.32