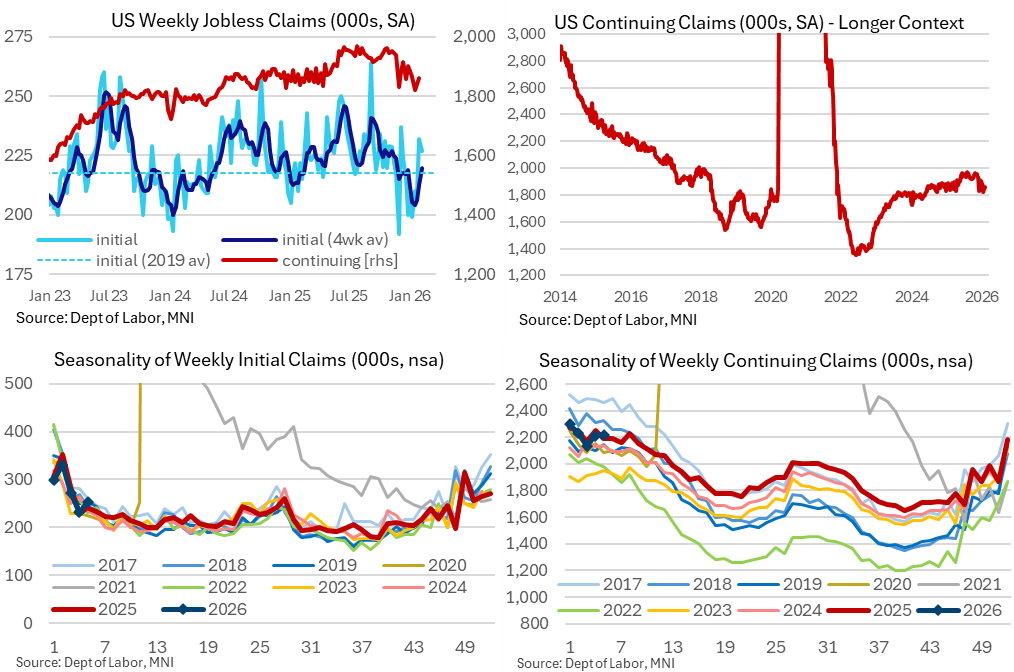

US DATA: Initial Claims Off Recent Lows, Continuing Still Lower Than 2H25

Weekly jobless claims surprised a little higher on both an initial and continuing basis. Initial claims still dipped a little after last week’s surprisingly large increase in what looks like a reversal of weather disruption, although residual seasonality more broadly looks to explain recent trends (both lower and now higher).

- Initial claims were a little higher than expected at 227k (sa, cons 223k) in the week to Feb 7 after a marginally upward revised 232k (initial 231k).

- Recall that last week’s upside surprise for initial claims looked to have been boosted by severe winter weather in the last weeks of January, and there are tentative signs that this might have faded in this latest week.

- There was some reversal of those states which saw the largest increases in the prior week: Pennsylvania saw -3.3k after +5.3k, Missouri -2.9k after +2.8k and Illinois -2.3k after +2.2k. These state-level details are in NSA terms as always, so some caution is needed, but they compared with national initial claims falling by 4.6k in NSA terms.

- There is still likely some residual seasonality at play though, having biased initial claims lower in December and January (the 4-week average hit a recent low of 204k up to Jan 17) before tilting higher again into February (220k latest 4-week average) and potentially beyond.

- Continuing claims were also a little higher than expected at 1862k (sa, cons 1850k) in the week to Jan 31 after a marginally downward revised 1841k (initial 1844k).

- Whilst it sees continuing claims extend their lift off a recent low of 1819k two weeks prior in the week to Jan 17, they are still comfortably lower than prior payrolls reference weeks including 1914k in Dec, 1944k in Nov and 1957k in Oct.

- Non-seasonally adjusted levels of continuing claims had for much of last year been tracking right at the top of ranges seen in previous years, before dropping somewhat back more into ranges so far in 2026, as indeed was the case in early 2025.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Initial Dovish Moves Following CPI Fades From Extremes, June Cut Priced

Initial dovish move on the softer-than-expected CPI data fades from extremes despite the lack of any overt hawkish caveats (volatile food and energy components provide an upward bias, with the supercore measure particularly soft vs. the limited amount of sell-side estimates we had seen). Our macro team continues to examine the details, which could be key when it comes to lasting market assessment.

- Recent data collection issues linked to the government shutdown and ongoing questions surrounding the Fed are potential factors behind the fade as market uncertainty/trust increases vs. norms.

- SOFR futures now +0.25 to +4.0 across the active contracts vs. +0.5 to -1.0 heading into the data. SFRZ6 is 3.0 off spike highs, with SOFR-implied terminal rate pricing at 3.155% vs. 3.190% heading in.

- FOMC-dated OIS prices ~1bp of easing for this month, 6.5bp through March, 12.5bp through April, 25bp through June and 55.5bp through year-end. That compares to 1bp, 6bp, 10.5bp, 23bp and 50.5bp into CPI.

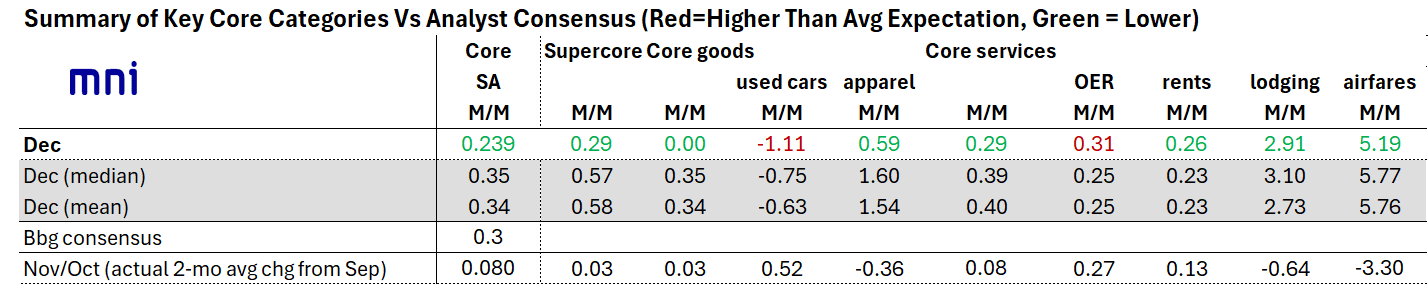

US DATA: Both Core Goods And Services Come In On Soft Side, Comms And Cars Weak

Within the core categories, the big surprise was that there was zero inflation in core goods prices despite anticipation that there would be "payback" in particular for unusually low holiday sales-related goods prices in November (along with continued expectations of tariff passthrough).

- Used cars saw a 1.1% fall (-0.8% expected) for the softest month since July 2024, with apparel rising 0.6% (1.6% expected).

- New vehicle prices were flat in a continuation of recent softness.

- Overall core goods ex-used vehicles were up 0.16% M/M which is in the pre-Oct/Nov range (averaged 0.14% between Jan and Sep).

- Core services (0.29% vs 0.39% expected) and overall supercore (0.29% vs 0.57% expected) were also on the soft side though directionally most of the major categories were in order. That includes a pickup in OER and rents that looks a little more than expected, and while travel-related services jumped as expected it wasn't quite as strong as consensus had thought.

- There was a notable pullback in communications (-1.9%, one of the biggest drops in years) prices; some medical care services looked elevated (dental +0.7%, hospital +0.9%) with overall medical care up 0.4%.

MNI EXCLUSIVE: MNI speaks to ECB sources

MNI speaks to ECB sources - On MNI Policy MainWire now, for more details please contact sales@marketnews.com