NEW ZEALAND: Inflation Stabilising, Weaker Employment But Exports Improve

ANZ business confidence for August rose to 49.7 from 47.8, the highest since March. However, the activity outlook deteriorated to 38.7 from 40.6, the weakest since May. ANZ noted that the August 20 rate cut drove some “isolated lifts in the data” but there was “no generalised confidence improvement”. The survey remains consistent with a gradual but lacklustre recovery.

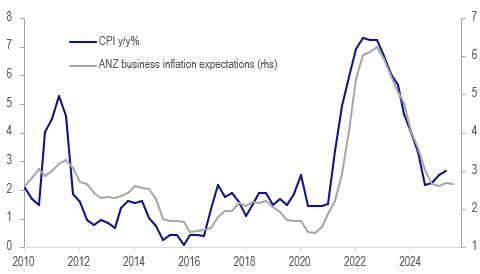

- Price/cost components improved, which is welcome given the risks that inflation will exceed the 3% top of the RBNZ’s band in the short term.

- Inflation expectations were 0.1pp lower at 2.6% in August and pricing intentions were down 1 point to 42.5, lowest since November, with 3-month ahead up 0.1pp to 1.5% driven by retail at 2.4%. Costs remained elevated but moderated 2 points to 74. Cost expectations 3-months ahead fell 0.1pp to 2.3%, while wages a year ahead moderated 0.1pp to 2.4%.

NZ CPI y/y % vs business inflation expectations

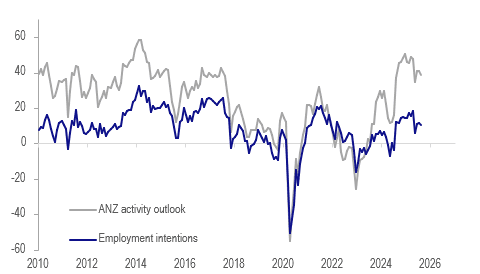

- Activity compared to a year ago deteriorated to +1.3 from +5.9 driven by continued weakness in construction but retail improved sharply in late August. The series is an indicator of GDP growth and is signalling a soft Q3.

- Employment eased 1 point to 10.5 but ANZ noted that services rose for the third straight month. July filled jobs in services rose 0.3% m/m. The Q3 average of business hiring intentions is currently slightly below Q2’s signalling that labour market conditions have remained soft.

- Investment and export intentions were bright spots. The former rose 0.5 point to 20.2, highest since December, driven by agriculture and services. Exports picked up 2 points, the highest since March before US reciprocal tariffs announced, with manufacturers strongest since February.

NZ ANZ business employment intentions vs activity outlook

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: Q2 Core Inflation Expected To Be 0.1pp Above RBA Forecast At 2.7%

Q2 CPI prints Wednesday and will be monitored closely given that the RBA relies on this series with the monthly version not yet complete (due to take place on November 26). Headline inflation continues to be distorted by federal & state government electricity rebates and so attention will remain on the underlying trimmed mean. Bloomberg consensus expects it to rise 0.7% q/q and for the annual rate to ease to 2.7% y/y from Q1’s 2.9%. The RBA’s May forecast was for 2.6% y/y and so a print close to this would likely result in an August cut but steady around Q1 may add doubt.

- Most analysts reporting to Bloomberg are around consensus at 2.6-2.7% y/y but forecasts range from 2.5-2.8% and the quarterly rate 0.5-0.8%. In terms of the major local banks, NAB and Westpac are in line with consensus, CBA expects 0.7% q/q but the annual rate to rise to 2.8%, while CBA has a slightly lower quarterly increase of 0.6% but annual inflation still 2.7%.

- Services inflation will continue to be watched as a measure of domestically-generated pressures. After being sticky through 2024, core services moderated to 3.3% y/y in Q1 from 4.2%.

- Q2 headline CPI is forecast to rise 0.8% q/q and 2.2% y/y after 0.9% q/q and 2.4% y/y in Q1. The RBA projected 2.1% y/y in May. CBA and NAB are in line with consensus, ANZ is forecasting 0.8% q/q & 2.1% y/y but Westpac is higher with 0.9% q/q & 2.3% y/y.

- Monthly June data are also released Wednesday and headline inflation is expected to be steady at 2.1% with forecasts ranging from 2.1% to 2.5%. ANZ and CBA are in line with expectations, NAB is lower at 2% and Westpac higher at 2.3%.

USD: US-EU Trade Deal Adds Fuel To The Paring Back Of Extreme Shorts

The BBDXY range overnight was 1198.76 - 1208.24, Asia is currently trading around 1208. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. Yesterday's US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. There is lots of event risk coming up this week and we are heading into month-end so some caution is warranted, this could potentially see some more paring back of USD shorts. Today is corporate month-end and this could also add to some short-term USD demand putting further pressure on the shorts.

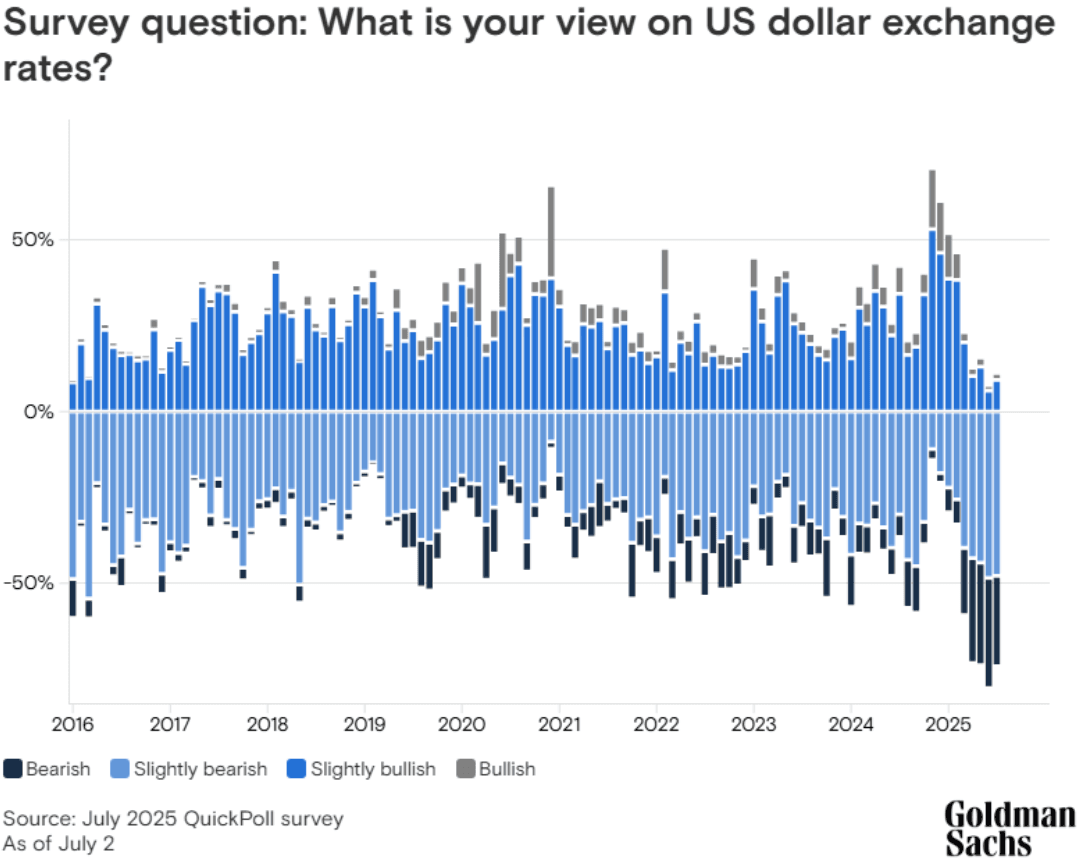

- Daily Chartbook on X: “In "a survey of 800 institutional investors ... The proportion of respondents expecting the dollar to weaken amid growing US fiscal concerns is near an all-time high -Goldman Sachs.” See Graph below.

- Arnaud Bertrand on X: “If Europeans were paying attention (or being told the truth), they should be beyond appalled by this "deal. It's nothing more than one of the most expensive imperial tributes in history. Just a massive one-way transfer of wealth with no reciprocal benefits.”

- Robin Brooks on X: “Today's rise in the Dollar is very unusual. Usually, such increases in the Dollar (vertical) map into a favorable move in the 2y2y forward rate differential (horizontal), but that isn't the case today. That could be a sign that Dollar short positioning is extremely stretched...”

- “The Dollar is seeing a big rise. Several drivers: (i) EU - US trade deal is reminder that - having dropped the ball on Ukraine - EU is supplicant, not master; (ii) tariffs are Dollar-positive, the fact that they drove the Dollar down was always an anomaly. The Dollar has based...”

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows. This consensus will also result in some decent short squeezes as a lot of the market is positioned the same way.

- Data/Events : Advanced Goods Trade Balance, FHFA House Price Index, S&P Corelogic, JOLTS, Conf. Board Consumer Confidence, Dallas Fed Services Activity.

Fig 1: Goldman Survey On USD View

Source: MNI/@dailychartbook/Goldman Sachs

AUSSIE BONDS: Solid Absorption of May-28 Supply But With Less Demand Present

The latest round of ACGB May-28 supply sees the weighted average yield print 0.61bps through prevailing mids (per Yieldbroker), extending the recent trend of firm pricing at ACGB auctions.

- However, the cover ratio dropped to 3.3300x from 3.9550x at the previous outing.

- As highlighted in the preview, the outright yield was 10-15bps higher than the previous auction but remained around 80bps lower than the cycle peak in early November last year.

- Today’s bid was likely supported by market expectations for RBA easing in 2025. A 25bp rate cut in August is given a 90% probability, with a cumulative 59bps of easing priced by year-end.

- Also on the positive side, it's important to note that the May-28 bond was included in the YM basket.

- However, sentiment towards global bonds has deteriorated over July.

- There has been no notable movement in the cash line in post-supply dealings.