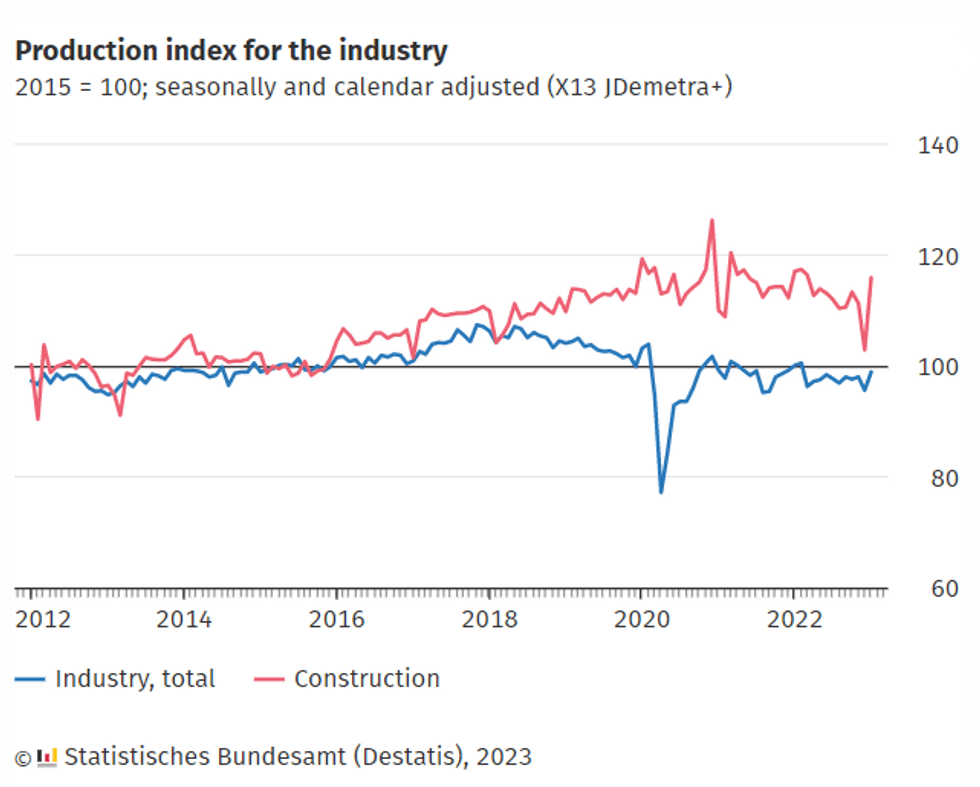

GERMAN DATA: Industrial Production Signals More Robust Start to 2023

Mar-08 07:20

GERMANY JAN INDUSTRIAL PROD +3.5% M/M (FCST +1.4%); DEC -2.4%r M/M

GERMANY JAN INDUSTRIAL PROD -1.6% Y/Y (FCST -3.7%); DEC -3.3%r Y/Y

- German industrial production jumped +3.5% m/m in January, outpacing forecasts of a softer +1.4% m/m rebound. Production remained -1.6% y/y below January 2022 levels.

- Sector-wise, January industrial production was volatile. Strong growth in electronics and chemicals boosted the headline m/m print, whilst substantial contractions were recorded across auto and pharma industries.

- Energy-intensive branches saw a marked +6.8% m/m expansion, assisted by falling energy prices and the introduction of price caps.

- Looking forward, despite the German manufacturing PMI slowing in February, output edged up for the first time in nine months due to positive developments in supply chains, new orders and employment.

- Furthermore, the IFO business survey outlooks improved in February as China’s recent reopening measures are seen as boosting exports.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: What to watch (2/2)

Feb-06 07:20

- In the UK, we will hear from Mann and Pill today; Ramsden, Pill and Cunliffe tomorrow, and the testimony ahead of the TSC from Bailey, Pill, Tenreyro and Haskel on Thursday. In addition, we will receive December activity data and the first print of Q4 GDP on Friday. Although this data is of much less importance than inflation or labour market data at present, it will still be an important datapoint for the MPC.

- In the US focus will remain on digesting the impact of Friday's labour market and ISM services data in the early part of the week, as well as the ramifications from the shooting down of the Chinese balloon and any implications that may have on the politics side. The highlight of the week in data terms will be Michigan inflation expectations data on Friday.

OUTLOOK: What to watch (1/2)

Feb-06 07:17

We have already received German factory order this morning which came in stronger than expected. Core FI markets have moved lower again in Asian trading, as market participants continue to react to Friday's much stronger than expected US labour market data.

- The RBA rate decision is due overnight tonight with a 25bp hike widely expected. The focus is likely to be on any change in tone of the statement and indications of how the RBA's forecasts have changed. For the full MNI RBA Preview click here.

- German inflation will be the focus for Eurozone markets this week. There is a large spread in expectations for the number in the Bloomberg survey. The median estimate is 10.0%Y/Y with the average estimate of 9.8% with four analysts looking for a sub-9.0% number. We noted last week that the Eurozone flash HICP print implied a reading of 7.9%Y/Y to 8.6%Y/Y. So we will need a decent downside surprise to this week's German number for EZ HICP not to be revised downwards in the final reading. See the full analysis piece here.

MNI: GERMANY DEC FACTORY ORDERS +3.2% M/M (FCST +2.0%); NOV -4.4%r M/M

Feb-06 07:01

- MNI: GERMANY DEC FACTORY ORDERS +3.2% M/M (FCST +2.0%); NOV -4.4%r M/M

- GERMANY DEC FACTORY ORDERS -10.1% Y/Y (FCST -11.6%); NOV -10.2%r Y/Y