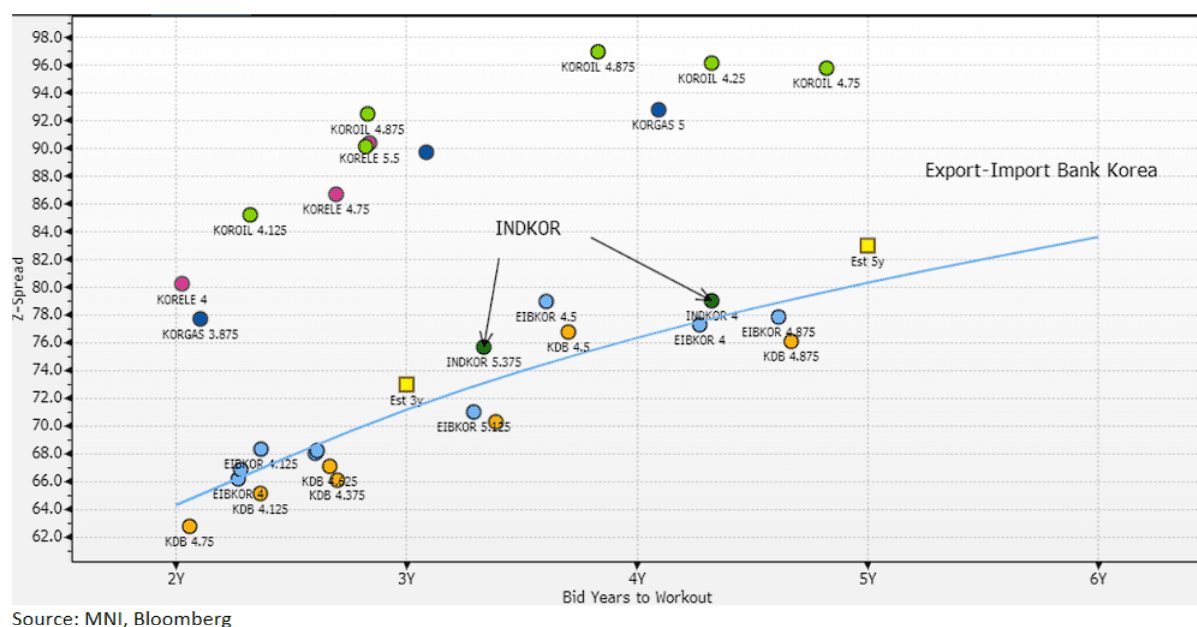

EM ASIA CREDIT: Industrial Bank of Korea (INDKOR; Aa2/AA-/AA-) - FV Estimate

"*MANDATE: INDUSTRIAL BANK OF KOREA USD 3Y/5Y FXD/FRN SOCIAL BOND" - BBG

Industrial Bank of Korea (INDKOR), majority owned by the Korean government, has mandated banks for a possible $ 3y/5y fixed/frn deal. We take a look at where fair value is for a possible 3y or 5y fixed deal.

Comparable bonds issued in the last 3 years, include those from INDKOR, as well as State backed Export-Import Bank Korea (EIBKOR), which we use for a guide on the curve. We believe that they will trade closely together, with INDKOR perhaps a few bp wide to the EIBKOR curve as is the case with the existing bonds.

We therefore see fair value for a 3y at z+ 73 and a 5y at z+83bp, the 2y extension being worth around 10bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUDUSD Continues Trending Higher On US$ Weakness, AUDNZD Lower

AUDUSD is off its intraday low of 0.6432 to be up 0.5% to 0.6468 following Friday’s outperformance. It reached a high of 0.6481 earlier helped by US President Trump suggesting today that some trade deals could be announced this week. With the US dollar continuing to weaken (USD BBDXY index -0.4%), the G10 is broadly stronger against the greenback.

- AUDJPY is lower in the softer risk environment. The pair is down 0.2% to 93.25 after a high of 93.59.

- AUDNZD has trended down through the session and is now -0.2% to 1.0816 after a low of 1.0814.

- AUDEUR is little changed at 0.5703 off the intraday trough of 0.5686. AUDGBP is 0.2% higher at 0.4865.

- Many Asian markets are shut today but equities are generally weaker with ASX down 0.8% and TAIEX -2.1%. The S&P e-mini is down 0.7%. Oil prices are sharply weaker with WTI -3.9% to $56.01/bbl. Copper is up 0.6% and iron ore is steady around $97/t.

- Later US services ISM/PMI data are released. The UK is closed.

ASIA STOCKS: Strong Inflows Continue Resume for Taiwan

Taiwan has experienced very strong inflows as signs of a thawing in the trade war resonate with investors.

- South Korea: Recorded outflows of -$65m as of Friday, bringing the 5-day total to +$722m. 2025 to date flows are -$12,329m. The 5-day average is +$144m, the 20-day average is -$254m and the 100-day average of -$144m.

- Taiwan: Had inflows of +$1,244m as of Friday, with total inflows of +$2,144m over the past 5 days. YTD flows are negative at -$17,215. The 5-day average is +$429m, the 20-day average of +$53m and the 100-day average of -$173m.

- India: Had inflows of +$20m as of the 30th, with total inflows of +$1,814m over the past 5 days. YTD flows are negative -$12,266m. The 5-day average is +$363m, the 20-day average of +$74m and the 100-day average of -$111m.

- Indonesia: Had inflows of +$8m as of Friday, with total inflows of +$18m over the prior five days. YTD flows are negative -$3,055m. The 5-day average is +$4m, the 20-day average -$51m and the 100-day average -$37m

- Thailand: Recorded outflows of -$41m as of Friday, outflows totaling -$12m over the past 5 days. YTD flows are negative at -$1,645m. The 5-day average is -$2m, the 20-day average of -$24m the 100-day average of -$19m.

- Malaysia: Recorded inflows of +$80m as of Friday, totaling +$227m over the past 5 days. YTD flows are negative at -$2,579m. The 5-day average is +$45m, the 20-day average of -$16m and the 100-day average of -$32m.

- Philippines: Saw inflows of +$12m as of Friday, with net inflows of +$45m over the past 5 days. YTD flows are negative at -$252m. The 5-day average is +$9m, the 20-day average of -$2m the 100-day average of -$4m.

INDONESIA: VIEW: Goldman Sachs Expects 100bp Easing By End-2025

The impact on headline inflation of the government’s electricity discount continued to unwind in April with the CPI rising 1.95% y/y from 1.0% y/y in March and -0.1% in February. Core remained at 2.5% y/y for the third consecutive month but well within Bank Indonesia’s (BI) 1.5-3.5% target corridor. Goldman Sachs continues to forecast BI will ease by a further 100bp by end-2025 if the rupiah will allow it. It sees a risk that rate cuts could continue to be delayed if the “IDR continues to underperform peer currencies”.

- GS said “Indonesia's headline CPI inflation increased to 2.0% yoy in April, returning to the central bank's inflation target band of 1.5-3.5% (vs. 1.0% yoy in March). Today's reading was above our and Bloomberg consensus expectations. On a seasonally adjusted, sequential basis, headline CPI slowed to 1.1% mom s.a. in April from 1.6% mom s.a. in the previous month.”

- “Housing and utilities inflation rebounded to 1.6% yoy in April (vs. -4.7% yoy in March) mainly from a normalization of electricity tariffs. This contributed 26bp towards the headline inflation in April, compared to -77bp the previous month.”

- “Core inflation, which excludes food and administered goods, was unchanged at 2.5% yoy in April as faster personal care inflation driven by high gold prices being offset by generally slower domestic goods and services inflation.”