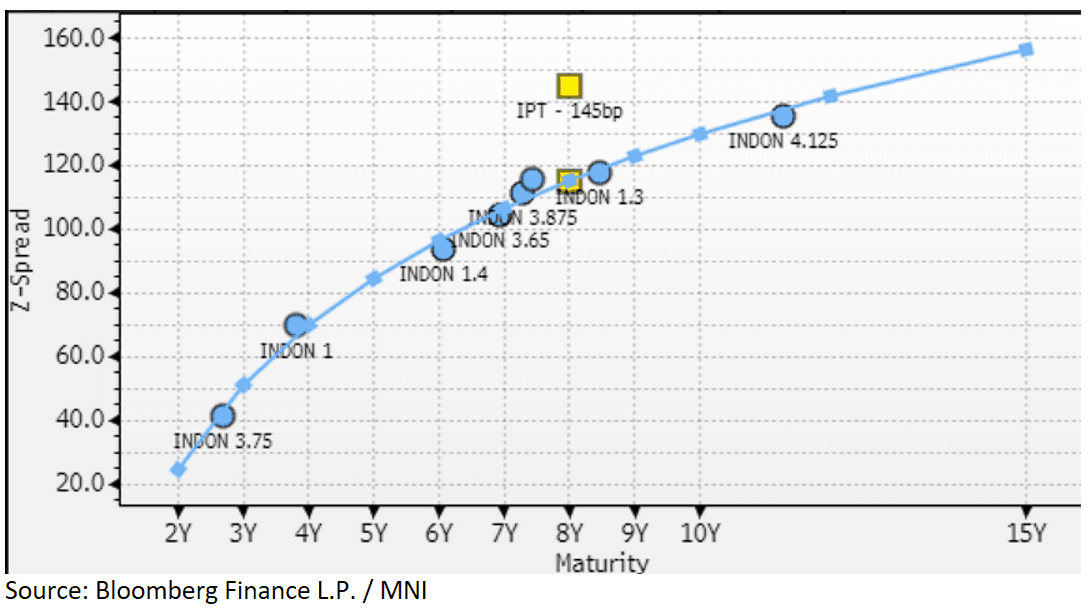

EM CREDIT SUPPLY: Indonesia: New EUR deal FV

(INDON, Baa2/BBB/BBB)

"*GUIDANCE: INDONESIA €BENCHMARK 8Y SDG MS+145 AREA" - BBG

New Issue: EUR benchmark 8Y

IPT: ms+145bp area

FV: ms+115 bp area.

Indonesia is coming to the market with a new EUR 8Y sustainability note. The Indonesia government EURO curve is relatively large, with the most liquid bonds according to Bloomberg data being the 28s, 32s and 37s. In terms of fair value, we see it more or less in line with the curve, with the new 8Y note at around ms+115bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Steady Start For Futures; 5s30s Testing Trendline Support

Uneventful start to the week for Gilt futures, currently +7 ticks at 91.30 with volumes running below recent averages for this time of day. Last week’s rally has highlighted a stronger technical corrective cycle, with the move higher also allowing an oversold trend condition to unwind. Friday’s high was pierced at the open, exposing 91.45 as the next upside target (Aug 15 high).

- The UK curve has lightly bull flattened, with 2/5-year yields little changed and 30-year yields around 0.5bps lower.

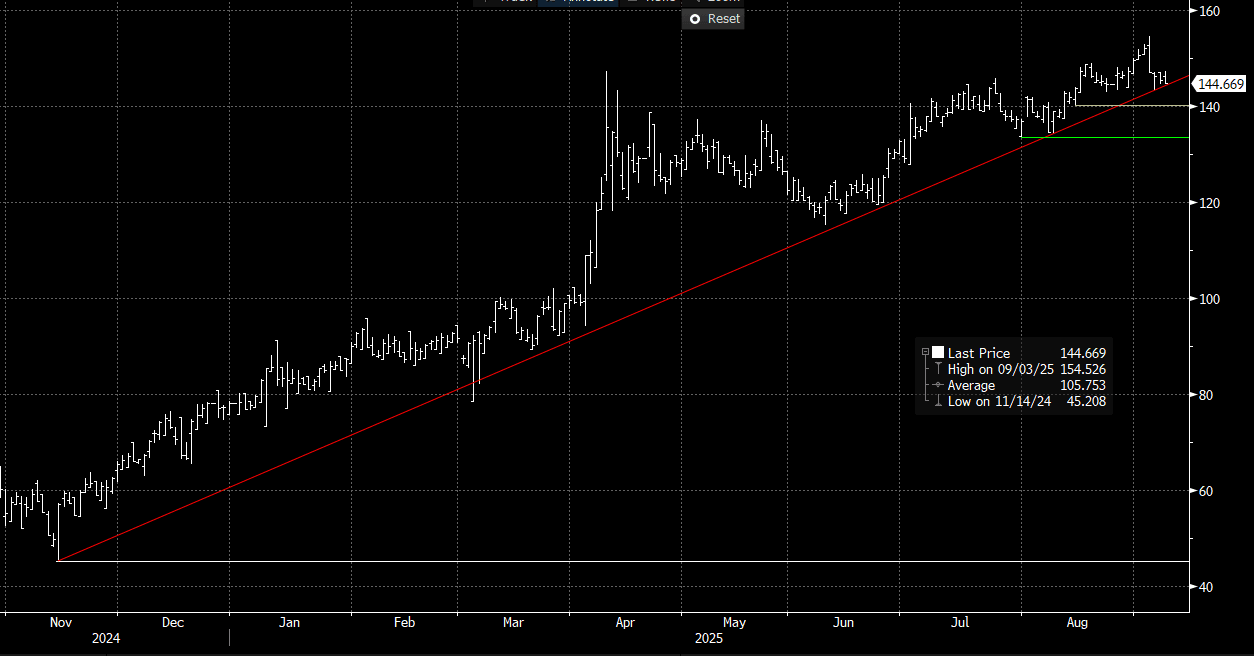

- 5s30s is 0.7bps lower at 144.7bps, extending the run of relief flattening that began last Wednesday. The spread is currently hovering around trendline support drawn from the November 2024 low. A clear breach of this support would leave scope for a retracement back towards ~140bps (Aug 14 low).

- 10-year yields are little changed at 4.643%, now 20bps below last Wednesday’s 4.845% high.

- A reminder that the KPMG-REC jobs report released overnight was weak, but had little market impact. The BRC shop sales monitor is released overnight, with monthly activity data for July due on Friday. Most data interest remains on next week’s labour market and inflation data.

- This week, Gilts will likely take cues from global core FI moves, with some focus reserved for political headline flow following Starmer’s reshuffle last Friday.

Figure 1: UK 5s30s Curve (Source: Bloomberg Finance L.P)

BONDS: Bunds Testing Friday's Highs; Core FI Curve Flatten With Exception of JP

Bund futures are testing Friday's 129.20 high (currently +8 ticks at 129.17), clearance of which would expose the August 6 high at 129.31.

- Headline flow has been relatively light this morning, while there was little impact from the stronger-than-expected German industrial production reading earlier.

In cash markets, the German curve leans bull flatter, with yields flat to 1.5bps lower.

- 5s30s is 1.1bps lower at 106.5bps, after marking a fresh multi-year high of 111bps on Wednesday.

- Global core FI curves have seen modest relief flattening over the past few sessions, but the technical trend remains for a steeper curve across the US, UK and Germany.

As noted earlier, the JGB curve twist steepened overnight following the resignation of LDP leader Ishiba on Sunday.

- Thatcherite MP Sanae Takaichi is a front-runner among many opinion polls - and also ran against Ishiba in the last leadership race. While politically conservative, she's made clear her preference for easy monetary policy and a bigger role for fiscal spending - reminiscent of the Abenomics policy set from 2012 - 2020.

- These dynamics clearly lean in favour of lower short-end, but higher long-end yields.

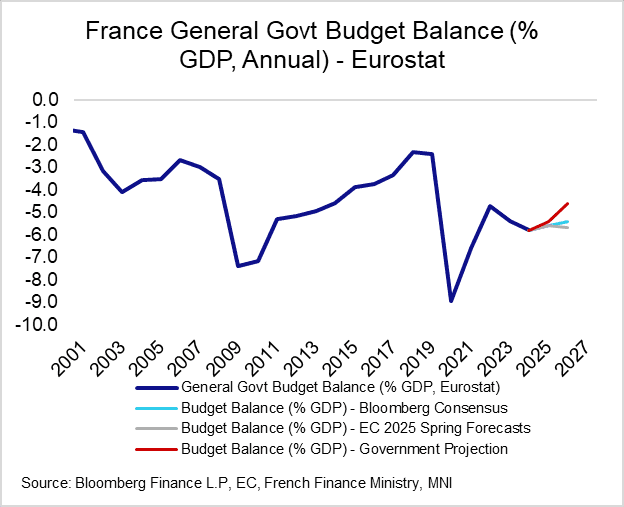

FRANCE: Markets May Already Price French Budget Concessions [2/2]

Focus for markets isn’t really on the vote itself, but its fallout. Parties on the right and left of the political spectrum have expressed a lack of confidence in Bayrou's fragile administration, exacerbated by his contractionary 2026 budget plans presented before the summer recess. Sources suggest President Macron wants to avoid calling another snap legislative (not Presidential) election, suggesting the only path forward for French politics is for a new PM to find support for a watered down set of 2026 budget proposals.

- The Socialist Party have proposed a budget that includes E22bln of fiscal consolidation measures, half of the E44bln planned by Bayrou.

- While a less fiscally tight budget would be more likely to gain support in the National Assembly (hence reduce political risk premium), it would have a negative impact on France’s already weak fiscal trajectory.

- However, the current analyst consensus and the EC’s Spring forecasts for the budget deficit/GDP ratio are notably less optimistic than the French Government’s (see chart). That suggests market prices may already incorporate an expectation for a new administration to make budget concessions. This may limit the scope for further OAT/Bund spread widening following the no-confidence vote.

- The 10-year OAT/Bund spread is 0.5bps narrower at ~78bps today. While off this year’s closing high of 81.5bps on Aug 27, it still incorporates around ~12.5bps more political risk premium than compared to mid-August levels.

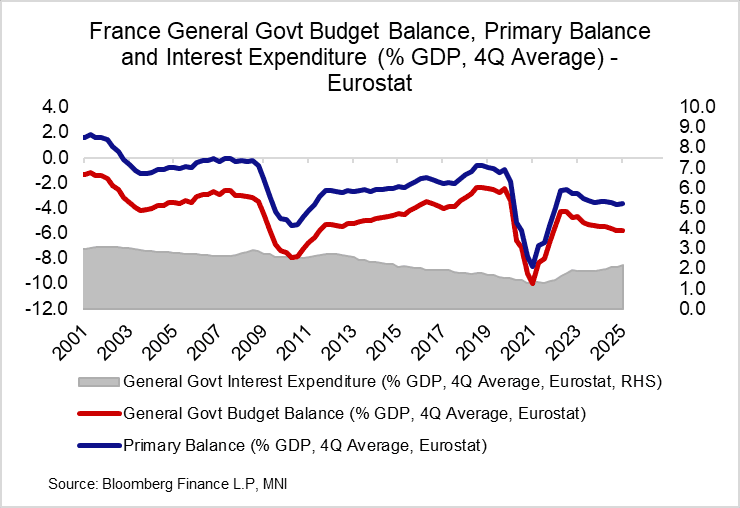

- Outright 10-year yields have pulled back alongside global FI peers in recent sessions, currently at 3.435%. While off year-to-date highs of 3.631%, 10-year yields remain up almost 25bps this year. This will place upward pressure on French interest expenditure for its extremely large debt burden.