IRAN: i24 Suggests Khamenei Has Not Approved MOU

May-28 14:51

i24 reporter Stein posts "Source familiar with the details tells i24NEWS: Mojtaba Khamenei did not a...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

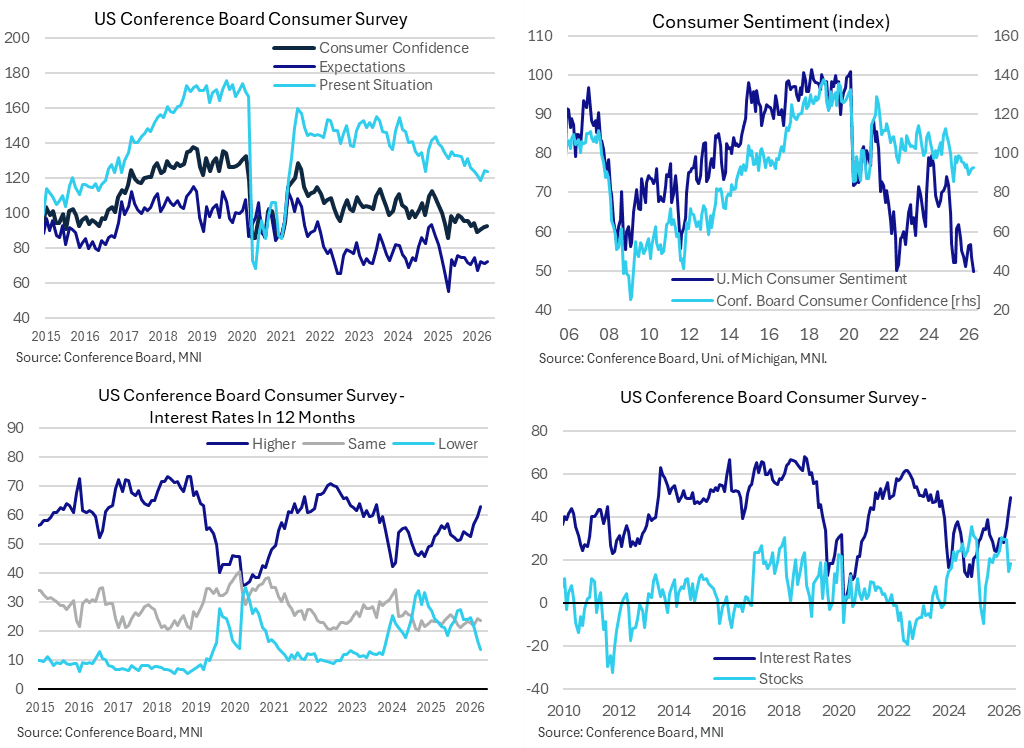

US DATA: Conference Board Consumer Confidence Sees Surprise Improvement

Apr-28 14:49

Conference Board consumer confidence surprisingly increased in April as perceptions of the present situation held up much better than expected and expectations surprisingly improved. Whilst still on the low side compared to recent years, it still paints a less pessimistic picture than U.Mich sentiment which hit a series low in April.

- Consumer confidence: 92.8 (cons 89.0) in April after upward revision to 92.2 (initial 91.8) in March

- Present situation: 123.8 (cons 120.1) in April after upward revision to 124.1 (initial 123.3) in March

- Expectations: 72.2 (cons 69.2) in April after fractionally upward revised 71.0 (initial 70.9) in March

- It marks a third consecutive monthly improvement in the main confidence index after the 89.0 in January was its lowest since 85.7 in Apr 2025 after tariff announcements.

- For recent context, it compares with the 95.8 averaged in 2H25, 96.4 in 1H25, 104.5 in 2024 and 105.4 in 2023 whilst it hit 85.7 in the depths of the pandemic to match the initial tariff hit.

- It therefore continues a rough trend decline in confidence, but the deterioration under the Trump administration has been less severe than its U.Mich counterpart where sentiment recorded a series low in April. It’s generally assumed that the U.Mich survey tends to be more susceptible to personal finance and inflation developments whereas as the Conference Board survey is more sensitive to the labor market.

- Within the details, the share expecting higher interest rates over the next year increased further from 59.3% to 62.8% for its highest since Aug 23.

- The share expecting higher stock prices over the next twelve months also improved on the month from 47.4 to 49.2% but it remains below the 53.7 averaged in Dec-Feb at what had been its highest since Jan 2025.

- “The survey period for this month’s preliminary results was April 1–22, a period that included the temporary two-week ceasefire in the Middle East conflict beginning April 8 and the subsequent rebound in US equities.”

PIPELINE: Corporate Bond Update: $1.25B Serbia Launched, Dual FX

Apr-28 14:46

- Date $MM Issuer (Priced *, Launch #)

- 04/28 $1.25B #Serbia 10Y +145, includes EUR1B 5Y & Eur900M 12Y legs

- 04/28 $750M #Emirates NBD Perp NC6 6.25%

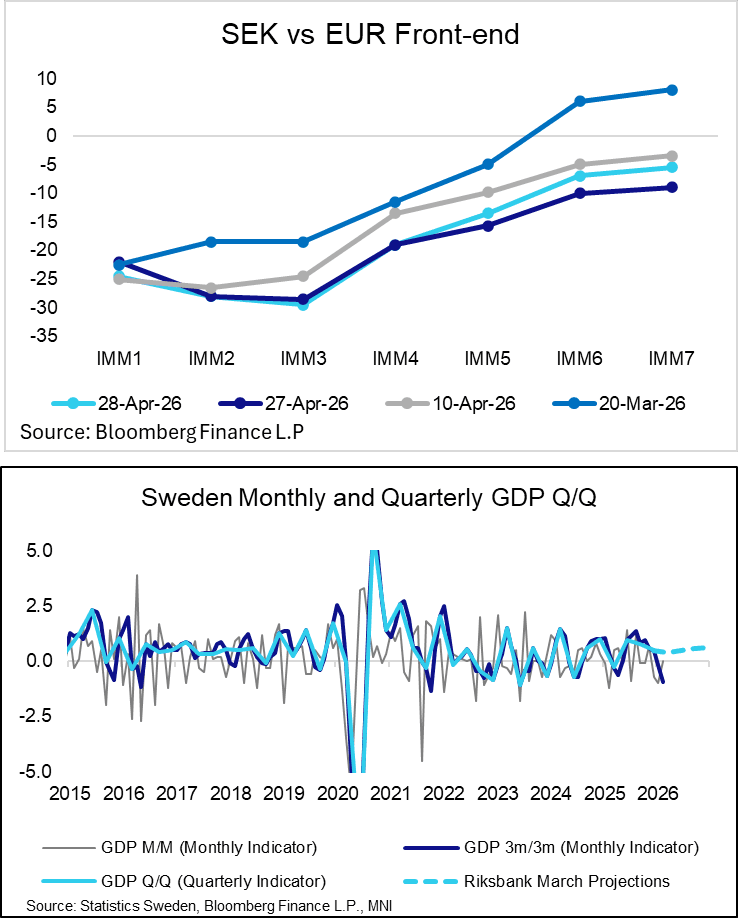

SWEDEN: Risk Sentiment Weighing On SEK FX, FRAs Reprice Hawkishly

Apr-28 14:46

- SEK sits towards the bottom of the G10 leaderboard today, with USDSEK up 0.7% and EURSEK up 0.45%. Fading optimism around an Iran war ceasefire deal – despite US President Trump’s latest Truth Social posts - have weighed on risk sentiment through the session. Zooming out, a number of SEK crosses remain in consolidation mode, with no clear near-term technical trend.

- We wrote last week that the krona will remain sensitive to developments in the Middle East, and would benefit from any material de-escalatory developments. However, low carry in the context of softening domestic growth momentum could limit upside in such a scenario.

- In rates markets, SEK FRAs have repriced hawkishly alongside EUR peers today. FRA implied rates are up to 10bps higher and now up to 60bps above 3M STIBOR. The SEK-EUR curve has twist steepened on the session.

- We continue to believe that any Riksbank policy reaction to the Iran war should be less aggressive than the ECB.

- Tomorrow’s Swedish macro calendar is heavy. We think the April Economic Tendency Indicator is most important. Alongside usual questions on sentiment and expected price plans, tomorrow’s survey is a quarterly version that also includes business inflation expectations and capacity utilisation measures.

- Flash Q1 GDP is expected at 0.2% Q/Q, below the Riksbank’s 0.4% March MPR projection. Given the weak development of the monthly GDP indicator in January and February, we think consensus may be too optimistic. However, the flash reading should always be taken with a pinch of salt, as it is volatile and revision prone.

- March retail sales and lending data area also released tomorrow, alongside February wages.