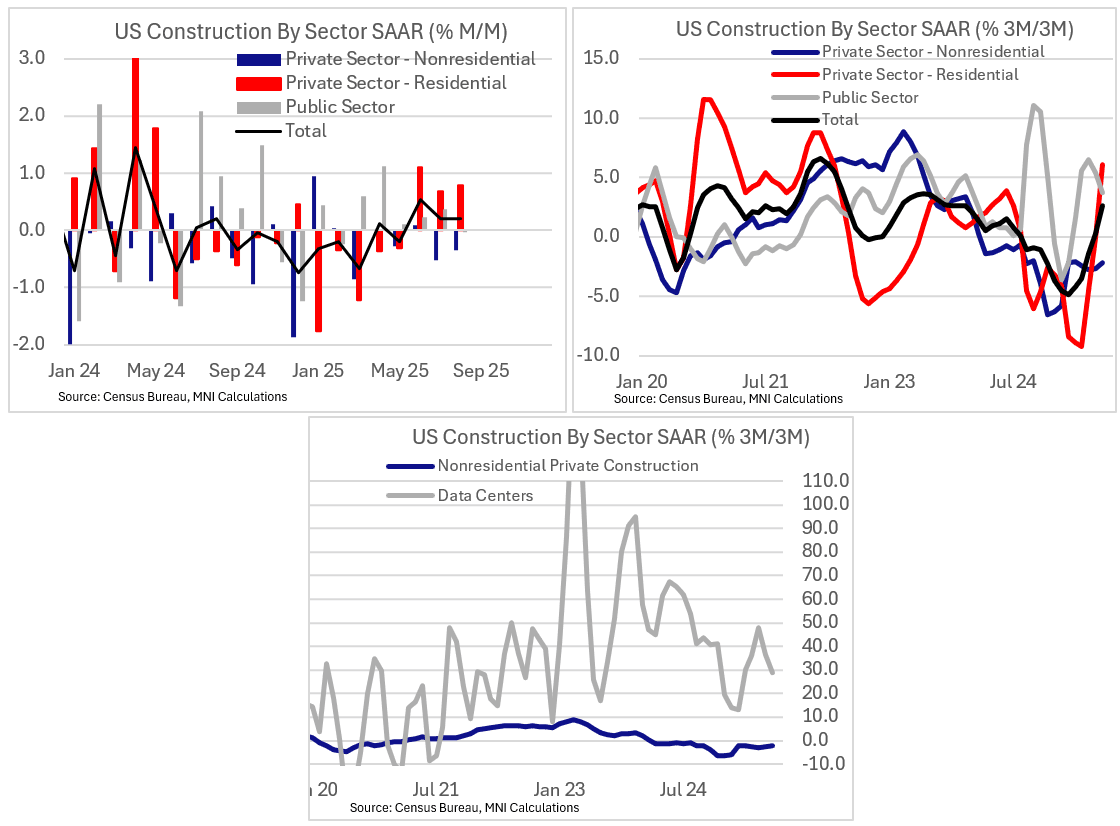

US DATA: Housing Is Starting To Lead Construction Growth As Data Centers Slow

August construction data - whose Oct. 1 release was delayed 6 weeks due to the federal government shutdown - showed a 0.2% M/M rise in spending (-0.1% expected, 0.2% prior rev from -0.1%). Overall construction looks to be stronger on the residential side than it did earlier in the year, boding positively for that side of the GDP equation, with public sector construction also looking solid enough. However, non-residential construction growth has stalled amid policy uncertainty, with even the vaunted data center boom showing signs of moderating over the summer.

- This was the 3rd consecutive rise in construction (which is expressed in seasonally-adjusted annual rate and nominal terms), the longest expansion since 2023. And the recent pickup is being driven by private sector construction: it rose 0.3% for a 3rd consecutive gain and is now rising 2.3% on a 3M/3M annualized basis following 11 consecutive declines.

- Somewhat surprisingly given the travails of the housing market, the pickup is being driven by residential construction - a 0.8% rise saw the 3M/3M rate jump to 6.1% for the first positive reading since August 2024 and the highest overall since April 2022 (the level is now at the highest of the year).

- Conversely nonresidential construction has contracted 2 months in a row, including manufacturing, both of which are at the lowest levels since 2023.

- One trend worth noting is an apparent slowdown in data center construction. It's still growing at an extremely elevated pace overall, 29% 3M/3M annualized in August, but this is down from nearly 100% at peaks in 2023/24.

- Public sector spending has been consistently positive for the last 6 months, making October's flat reading the weakest since February, but this is still an overall contributor to construction spending. There was virtually no growth in data center construction by value between June and August. That being said, this series has increased 4-fold since the end of 2021 and is worth about 5.5% of total non-residential private construction, up from 2% in that span.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: US Week Ahead Headlined By Delayed CPI Report On Friday

- The September US CPI report will be released on Friday, delayed amidst the government shutdown but with the BLS making a special exception on social security payment considerations.

- Bloomberg consensus looks for headline CPI inflation at a rounded 0.4% M/M after 0.38% back in August and for Y/Y inflation to firm two tenths to 3.1% for what would be its highest since May 2024.

- Core inflation is seen at a rounded 0.3% M/M after 0.35% in August (exceeding the median unrounded estimate of 0.31%) and 0.32% in July. It’s expected to see core CPI inflation hold at 3.1% Y/Y having in August increased to its highest since February.

- Core details should see focus on both goods and services angles: underlying goods inflation has clearly firmed in recent months on tariff pressures although the median increase has currently seen a peak back in June, whilst services will be watched for any spillover after some strong recent non-housing readings.

- The report will come within the FOMC blackout period ahead of the Oct 28-29 decision, with a 25bp cut fully priced and likely needing a large surprise to alter this.

- As for broader inflation details, Fed Chair Powell this week confusingly suggested that we will have the September PPI report but the BLS had previously said “No other releases will be rescheduled or produced until the resumption of regular government services”.

US DATA: Latest Jobless Claims Estimates During The Shutdown

As noted earlier, MNI estimates initial jobless claims at a seasonally adjusted 218k in the week to Oct 11 and continuing claims at a seasonally adjusted 1929k in the week to Oct 4.

- To give a better idea of sensitivity around these estimates, which rely on estimates for some missing states, we note the below analyst estimates:

- Goldman Sachs have a central estimate of 217k for initial claims in a range of 211-225k, whilst they see continuing claims at 1917k in a range of 1885-1930k.

- JPMorgan meanwhile also see 217k for initial claims whilst they see continuing claims as having held constant at 1927k.

NATGAS: Venture Global in Talks with Ukraine for more LNG Deliveries, Reuters

Ukraine is seeking more cargoes from Venture’s Plaquemines facility as the embattled nation approaches the winter heating season, according to Reuters sources

- Venture is in talks with Ukraine’s DTEK to procure more LNG cargoes after a year of gas infrastructure attacks by the Russians.

- Venture Global CEO Michael Sabel met with President Volodymyr Zelenskiy on Thursday October 16.

- DTEK signed an agreement in 2024 for an undisclosed amount of LNG from the facility, as well as 2 mtpa from Calcasieu Pass Phase 2 currently under construction.

- Plaquemines currently has spare capacity to deliver more cargoes to Ukraine on the spot market, per Reuters.

- Plaquemines now sends out the second highest LNG volume in the US, with feedgas demand averaging 3.45 bcf/d according to MNI figures.