TURKEY: Home Sales Rose 19.8% Y/Y in December

- Turkey's home sales rose 19.8% Y/Y in December versus -7.8% in November, according to the Turkish Statistical Institute. Home sales rose 14.3% in 2025 as a whole to 1.69m units - 254.8k sales were made in December.

- Ekonomi run a piece in which they note that the new year began with news that two companies were unable to make payments on their bonds. Experts cited by the newspaper point out that more companies may follow, reflecting the difficulties that financially distressed companies are facing amid high interest rates and limited access to financing.

- Looking ahead, the CBRT rate decision on Thursday provides the key highlight of the week, with the central bank expected to reduce the one-week repo rate by 150bps to 36.50% after the December CPI inflation data came in slightly below expectations. Our full preview, with analyst views, will be published later today.

- Note too that Fitch Ratings and Moody’s both may publish their credit rating assessments for Turkey after the market close on Friday. Turkey’s credit rating at Fitch is BB- while its credit rating at Moody’s is Ba3, with stable outlooks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (H6) Marked Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.160 @ 15:32 GMT Dec 19

- SUP 1: 95.120 - Low Dec 10

- SUP 2: 95.087 - 2.0% Lower Bollinger Band

- SUP 3: 94.276 - 1.0% 10-dma envelope

Aussie 10-yr futures remain well toward the bottom of the recent range, having taken out all major support levels in the process. With 95.275 cleared, prices are pushing to new contract lows, opening vol-band support through 95.087 and into 94.276. Any recoveries need to break back above 95.900 to signal near-term bullish traction.

AUDUSD TECHS: Corrective Phase Still In Play

- RES 4: 0.6759 High Oct 11 ‘24

- RES 3: 0.6723 High Oct 21 ‘24

- RES 2: 0.6707 High Sep 17 and a key resistance

- RES 1: 0.6661/86 High Dec 16 / 10

- PRICE: 0.6608 @ 15:56 GMT Dec 19

- SUP 1: 0.6593 Low Dec 18

- SUP 2: 0.6566 50-day EMA

- SUP 3: 0.6517 Low Nov 27

- SUP 4: 0.6466/21 Low Nov 26 / 21

The trend condition in AUDUSD remains bullish and the latest pullback appears corrective. The move down is allowing a recent overbought condition to unwind. Support at the 20-day EMA, at 0.6598, has been pierced. The 50-day average is at 0.6566. The area between the two averages represents a key short-term support zone. A resumption of gains would refocus attention on key resistance at 0.6707, the Sep 17 high and bull trigger.

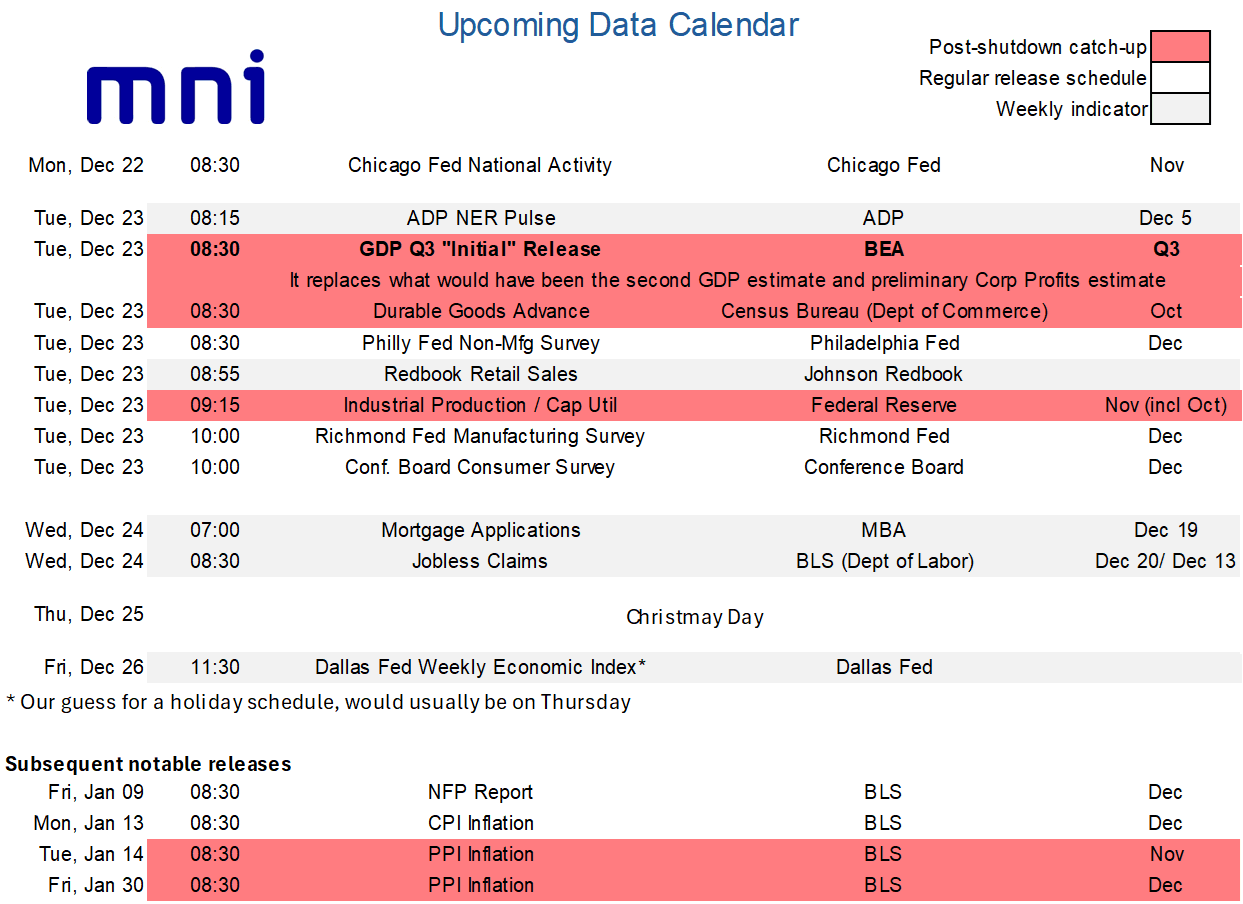

LOOK AHEAD: US Macro Week Ahead: Long-Awaited Q3 GDP Plus Labor Updates

- The week ahead sees a slimmed down data schedule after a particularly busy few weeks, including distorted NFP and CPI reports in the week just gone. There are still some important releases though, with the highlight being the long-awaited “initial” Q3 GDP release on Tuesday.

- This report will replace what would have been the second GDP and the preliminary corporate profits estimates, with the extended tracking window of the Atlanta Fed’s GDPNow pointing to strong real GDP growth of 3.5% annualized after an average 1.6% in 1H25 (-0.65% in Q1 before 3.84% in Q2).

- Expect continued close attention on private demand, best seen by Powell’s preferred PDFP category, which is currently tracking at ~2.4% annualized for similar to the 2.4% averaged in 1H25 (1.9% Q1 before 2.9% in Q2).

- Tuesday also sees updates for the weekly ADP tracker in the four weeks up to Dec 5, getting closer to the reference period for the monthly report, after last week’s further improvement. It’s followed by useful updates for Q4 GDP tracking with durable goods for October and industrial production for both October and November, before the Conference Board consumer survey for December with its closely watched labor differential having stalled at subdued levels but not deteriorated further since September.

- Note as well that Wednesday then sees weekly jobless claims a day early ahead of Christmas Day, with continuing claims capturing the December payrolls reference period. There is currently minimal Fedspeak scheduled and we suspect this will remain the case ahead of Christmas, likely confined to media appearances if any.