OIL: Hold Thursday Losses, Flat On Week, US Military Build Up Continues

Oil benchmarks are holding a little weaker in the first part of Friday dealings, after sharp losses on Thursday, as the threat of near term strikes from the US on Iran appear to have receded. WTI was last near $59.10/bbl, while Brent was close to $63.60/bbl (both benchmarks fell by more than 4% on Thursday). We are now back to little changed for the week for both oil benchmarks.

- Still, market sentiment is likely to remain skittish, as Fox News reported that the US continues to push military assets into the region: via BBG: "Washington is boosting its military presence in the Middle East. At least one aircraft carrier is moving into the region and other military assets are expected to be shifted there in the coming days and weeks, Fox News reported, citing military sources."

- For WTI futures, a bull cycle remains intact for now and the move lower from Wednesday’s high appears corrective. Price has traded through a key short-term resistance at $61.25, the Oct 25 high, this week. This strengthens the bull phase and highlights a stronger reversal of the recent downtrend. Sights are on $62.59 next, a Fibonacci retracement. Initial firm support lies at $58.64, the 50-day EMA.

- More broadly, focus will remain on surplus risks in the oil space, with this the clear desire from a US administration standpoint as Trump seeks to lower (or keep low) gasoline/fuel prices onshore in the US.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

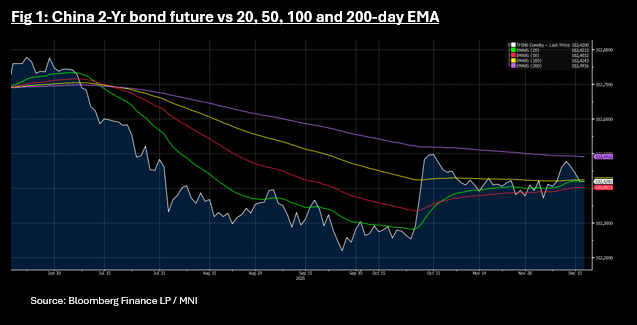

CHINA: Bond Futures Steady as Equities Rebound

- As equities rebound after two days of losses, bond futures are steady this morning moving only marginally higher.

- The China 10-Yr future is up +0.06 at 107.96 as it nears the 20-day EMA of 107.99.

- The 2-Yr future is up +0.01 at 102.42, atop the 20-day EMA of 102.42. Were it to break below, downside resistance is via the 50-day EMA of 102.40.

- Cash is steady with the 10-Yr at 1.84%, down -0.5bps this morning and the 2-Yr at 1.39%

JGBS: Futures Holding Weaker At Lunchtime Break, JGB Yields Steady

At the lunchtime break, JGB futures are holding negative, 133.29, -.14 versus settlement levels. Recent lows at 133.18 remain intact, while upticks continue to be faded, with a negative technical bias in play. US bond futures have failed to kick on from the overnight lead in and are down modestly during the morning session in Asia, which may be spilling over to JGBs at the margin.

- JGB yields are little changed in the first part of Thursday dealings. The 10yr was last near 1.97%, up a touch but short of recent cycle highs (close to 1.98%). The 2yr is around 1.07%, as Friday's BoJ meeting outcome comes into focus.

- The market is fully priced for a hike. Beyond December, attention will focus on guidance around the neutral rate, which Ueda has described as "1-2.5%," signalling that policy normalisation is likely to continue gradually rather than end at 1%. See our preview here:

- Earlier data was firmer on the export side and core machine orders, but isn't likely to shift BoJ thinking around the economic backdrop.

CHINA: More of the Same for Policy in 2026

- An article in the China Securities Journal assess policy in 2025 describing it as 'supportive' suggesting that since the beginning of the year various policy tools have worked together to guide financial institutions to increase their support for the real economy, whilst 'anchoring the goal of stable financial markets.

- Looking at the potential for policy in 2026, the article points to more of the same with the continuation of the current 'moderately loose' monetary policy, adhere to precise policy implementation whilst using flexible tools like RRR cuts and interest rate cuts to promote overall social financing costs.

- On social financing costs, the article points to overall social financing costs being at historical lows with lower loan interest rates thanks to cuts in the 7-day reverse repo rate, whilst lower housing provident fund loan rates are lower also. The weighted average interest rates for new corporate loans was 30bps lower than a year ago.

- The recent Central Economic Work Conference clearly stated that various policy tools, such as reserve requirement ratio (RRR) cuts and interest rate cuts, will be used flexibly and efficiently in what appears to leave room for further RRR and interest rate cuts in 2026.

- The focus on financing costs and banks willingness to lend will support the government's goal of improving domestic demand and target innovative industries viewed as important to the future development of the economy.

- It appears from this article that there is no imminent change to come, rather more of the same as the economy remains on track to achieve the 5% GDP growth target.

- Instead, it appears now that the already 'supportive' policy provides a backstop and could be altered if needed.

- Going forward we continue to monitor social financing costs and lending data as a key insight for future direction of policy.