NEW ZEALAND: Higher Inflation Expectations Risk To Underlying Inflation

There was a significant pickup in RBNZ measured household inflation expectations in Q2 across time p...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: 10-Yr Grinds Lower Ahead of Strong Issuance Schedule

- Ahead of what is set to be a reasonably big week of issuance, the PBOC again has matched maturities in this morning's OMO - indicating that the interbank market remains flushed with liquidity.

- Whilst the 10-Yr CGB grinds lower again to 1.76%, the 10-Yr bond future is flat, whilst the 2-yr is down just -.01 at 102.556.

- In a light week for economic data releases, the PBOC kept 1-Yr and 5-Yr Loan Prime rates on hold today as solid growth and uncertainty for the path of US interest rates sees limited likelihood of policy intervention in 1H of 2026.

- The liquidity position is supportive of the issuance schedule ahead, with some sizable, longer duration issuance in the calendar.

- China to Sell 90 Bn Yuan 1.75% 2036 Bonds on April 22

- China to Sell 5 Bn Yuan 1.38% 2028 Bonds on April 22

- China to Sell 5 Bn Yuan 1.4% 2029 Bonds on April 22

- China to Sell 4.5 Bn Yuan 1.57% 2031 Bonds on April 22

- China to Sell 170 Bn Yuan 2027 Bonds on April 24

- China to Sell 85 Bn Yuan 2056 Bonds on April 24

- China to Sell 34 Bn Yuan 2046 Bonds on April 24

EUR: EUR/USD - Pulls Back From Top Of Range Above 1.1800

The EUR/USD range Friday night was 1.1765-1.1849, Asia is currently trading around 1.1755. The pair failed again to hold above the 1.1800 resistance as momentum stalls, we gapped lower on the open but have since filled most of that in. The market wants to sell USD’s but perhaps it needs to hold off for now as the market works through paring back some of last week's overzealous enthusiasm to pile back into risk. We are now pulling back from the top-end of the range toward the 1.1850 area and I suspect we should continue to find it tough going up here in the short-term, or until we get any real agreement reached. First support on the day is toward 1.1700 and then the 1.1600-1.1650 area, where USD bears will be looking for buyers to reemerge to have another crack at the 1.1850 area at some point.

- MacroEdge: “The Dutch cabinet will activate the first phase of the national emergency oil crisis plan on Monday.”

- EndGame Macro on X: “What This Really Means. This is the Dutch state admitting they may not absorb a Hormuz shock cleanly if the disruption lasts. Phase 1 is the point where an oil story becomes a state capacity story. The public message is no immediate shortage. The internal message is to prepare for one. And if the disruption drags on, the hardest economic damage will likely come with a lag. Inflation and transport costs hit first. Margins and output come next. Labor pain usually comes later, once firms stop treating the shock as temporary.”

- “There is no neat formula that turns lost barrels of oil into lost jobs one for one, but the broader pattern is clear. When oil prices stay high long enough, oil importing economies usually see weaker hiring, softer employment, and rising unemployment over the following quarters as higher energy costs squeeze margins, slow production, and hit demand. That is why the Dutch move should be read as a signal that policymakers think this may be moving beyond a temporary price shock and toward a serious supply shortage.” https://x.com/onechancefreedm/status/2046016980730421481?s=20

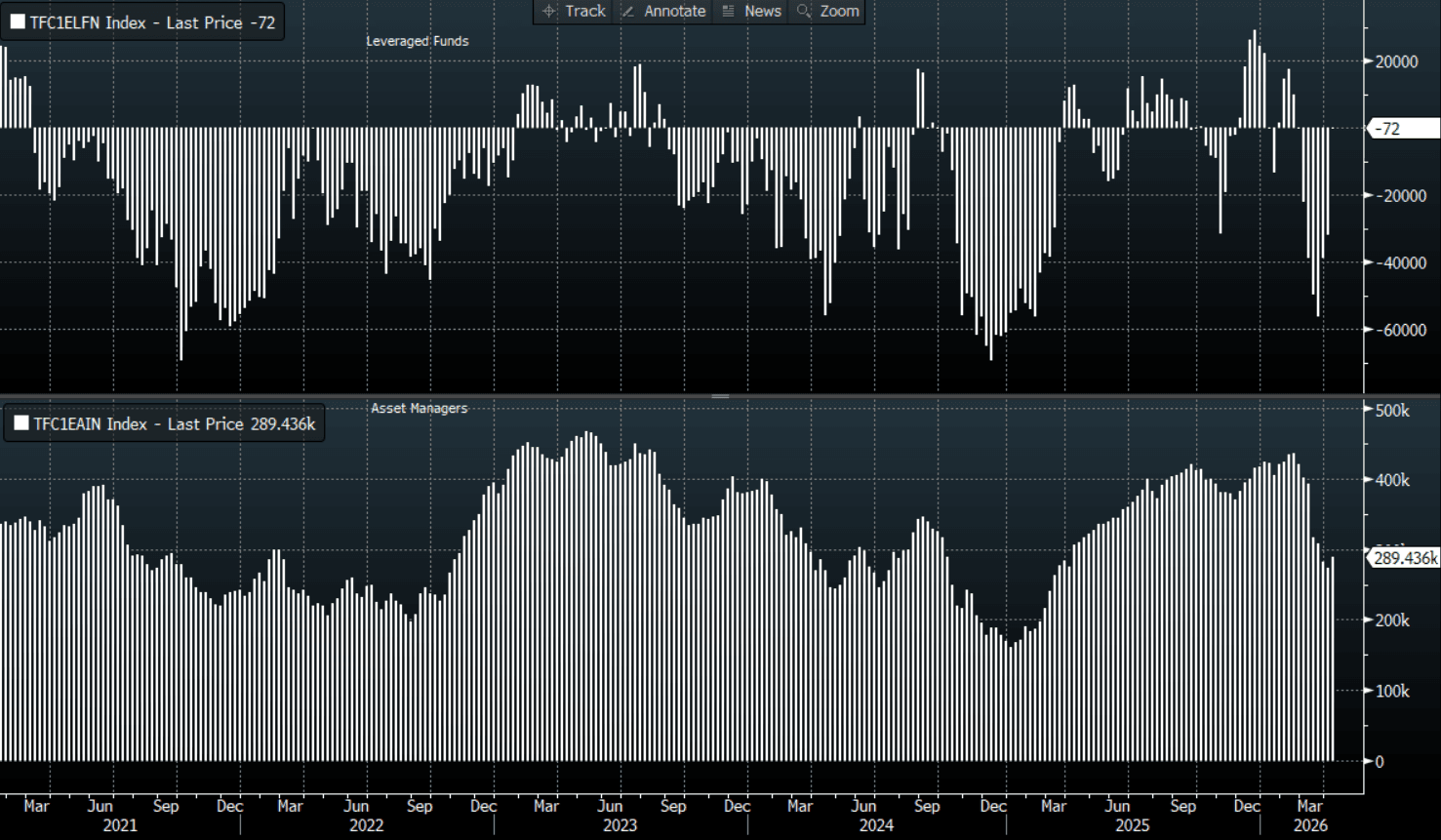

- CFTC Data up to 14/04/26 shows the Leveraged community aggressively to reducing their recently acquired short EUR exposure back to flat, -72(Last -31777). Asset managers started adding back their recently reduced core longs, +289 436(Last +273 833).

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.1600(EU1.52b), 1.1700(EU691m), 1.1750(EU1.76b). Upcoming Close Strikes : 1.1650(EU3.98b April 23), 1.1825(EU3.69b April 23), 1.1850(EU2.46b April 22) - BBG

- The EUR/USD Average True Range for the last 10 Trading days: 67 Points

Fig 1 : EUR CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

STIR: Will Market Fade Front End Pricing: RBNZ Vs RBA

While the next move by the RBA and RBNZ is most likely tightening, potential divergent timelines in our opinion have created a relative value opportunity in the OIS market.

- The RBA is expected to front-load tightening, driven by its view that demand has been too strong and is behind the recent inflation rise. It appears less data-dependent in the near term and inclined to reverse prior easing.

- The RBNZ, in contrast, has been signalling patience and gradualism, with future moves heavily dependent on incoming data. RBNZ Governor Breman was very clear that the MPC is focused on the medium-term and that the OCR path will depend on how growth and expectations develop and impact medium-term inflation.

- While markets broadly align with expectations of rates returning to around 3%, they appear to pricing hikes too aggressively and too early, with a full hike by July versus a more RBNZ-consistent September timeframe.

- This mismatch creates a potential opportunity: NZ front-end rates look too hawkish relative to the RBNZ’s guidance, especially versus Australia.

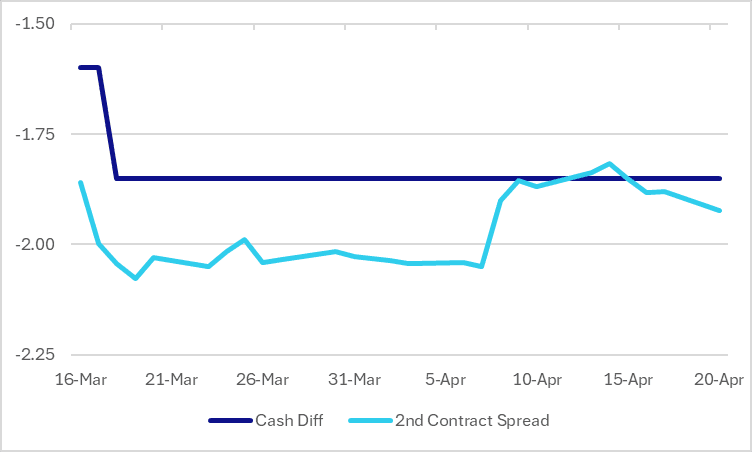

- One possible expression that could be considered is to fade front-end RBNZ pricing versus the RBA by way of the 2nd meeting date contract spread. A paid viewpoint of the Jun-26 RBA versus Jul-26 RBNZ OIS spread around current levels (-192bps), with scope to gravitate towards -210bps possible if the above macro views unfold.

Figure 1: NZ-AU – Cash Differential Vs. 2nd Meeting Date Contract Spread

Source: Bloomberg Finance LP / MNI